This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

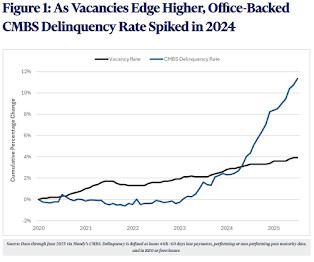

Consequently, this has temporarily masked the underlying CMBS distress, which has recently become more apparent through rising loan delinquencies and declining property valuations. In other words, 2024’s full-year delinquency spike even outpaced levels seen during the Global Financial Crisis (GFC).

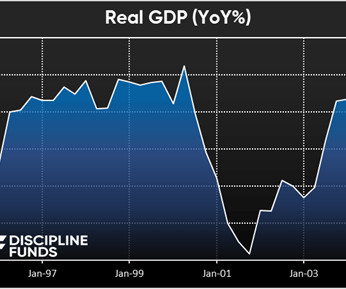

The previous high mark over this period, around the height of the dot-com era in early 2000, appears small in comparison. This means that the expansion of valuation multiples, like price-to-earnings (P/E), has played a big role.2 Data for Panel A and Panel B from 1/1/2000 12/31/2024. Pay attention to valuations.

This means valuations could actually move even higher and owning capital is going to become increasingly important for financial well-being. We lost almost 3MM jobs and the rate of GDP growth slowed, but from 2000 until 2003 RGDP actually averaged 2.25%. The age of abundance is coming. Everything will become a technology firm.

Equity markets corrected by more than 50% in 2000-01 and more than 60% in 2007-08 which lasted for 1.5-3 Like the circle of life, good times are followed by bad times, and bad times are followed by good times, stock markets also go through cycles of excessive greed/optimism to excessive fear/pessimism.

The Russell 2000, an index of 2,000 small-cap companies widely used as a benchmark for U.S. Fixed income investments are subject to various risks including changes in interest rates, credit quality, inflation risk, market valuations, prepayments, corporate events, tax ramifications and other factors. small-cap stocks, rose 4.50

In this post, we break down the most important differences between SPY and QQQ across key dimensions: performance, volatility, valuation, sector exposure, factor makeup, and fees. Using Portfolio Visualizer data from 2000 to May 2025, QQQ outperformed SPY slightly with a 7.77% annualized return vs. 7.52%. Standard Deviation 15.3%

So of course, what the Fed will do impacts markets, impacts valuations, impacts interest rates. 00:46:16 [Speaker Changed] I mean, if you look at the, the valuations, if you look at the fundamentals, it is, it’s surprising, right? So there’s still a pretty big valuation gap. So of course we follow it.

Equity markets corrected by more than 50% in 2000-01 and more than 60% in 2007-08 which lasted for 1.5-3 Like the circle of life, good times are followed by bad times, and bad times are followed by good times, stock markets also go through cycles of excessive greed/optimism to excessive fear/pessimism.

Small caps were the big winner on the day, though, as the Russell 2000 gained nearly 6% for its best day since November 2022. How the economy is doing, Fed policy, inflation, valuations and overall market trends potentially matter much more. Data Source: Carson Investment Research, FactSet 11/01/24 So What Really Matters?

crore, highlighting strong business performance relative to valuation. crore, highlighting strong business performance relative to valuation. crore, highlighting strong business performance relative to valuation. crore, highlighting strong business performance relative to valuation. 44,993 crore in FY25, which is over 2.02

This composite approach looks across profitability, valuation, growth, quality, and more to identify companies with durable fundamentals – not just high share prices or momentum. In 2000, the biggest companies were Cisco, GE, and Intel – none of which crack the top 20 today. RJF Raymond James $148.03 $29,866 14.3

For example, if the house brings in $2000 per month ($24,000 each year) and the sale price is $240,000, the next investor is buying a business with a price-to-earnings ratio of 10, because 240k/24k=10. But if you manage to convince someone to hand over $480,000 for that same house, youve sold at a P/E of 20.

You, you wrote at the journal through the.com implosion as well as the whole runup to 2000 September 11th, the great financial Crisis. I did it in 2000, 2002. So, so the 20 years you spent at the Journal really is a fascinating couple of decades. What era of finance did you find the most intriguing as a journalist?

Valuations Are a Poor Short-Term Timing Indicator Do you like buying things when they are pricey? There is virtually no proof that high (or low) valuations can predict what stocks might do the following year. Rather than making investing decisions based on valuations, you are better off investing in days that end in y if you ask me.

Dissecting Stock Performance & Valuations A lot of pundits are pointing to an overheated market, but on a 3-year basis, returns are looking more normalized (+8.2% Time will tell. per year) because of the -20% hit on stocks during 2022. Source: Yardeni.com As always, the future is uncertain, and risks abound for next year.

Barry Ritholtz : Well, that was sweet of them to do it that way… You know, I have a vivid recollection from the people I, we, we were talking about Josh Frankel and Dave Rosenberg, and I know a lot of Rich Bernstein, all these people I know from the 2000 Era Merrill Lynch. But we think that that valuations are there.

For instance, if you had bought Nasdaq, or even the S and PETF in March of 2000 for sure. And then number three is gonna be sentiment and valuation. Now, sometimes people say sentiment and valuation, why are they together? So, so valuation is going to reflect sentiment. The third is sentiment and valuation.

He began with a single restaurant, a single cookie store, and eventually parlayed that into a series of acquisitions, mergers, expansions, ultimately leading to the Panera Bread concept, which now has 2000 locations and does about six and a half billion dollars. He sold the company in 2017 or so for about seven and a half billion dollars.

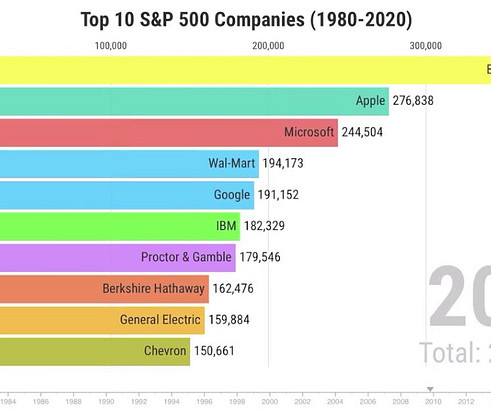

Four of 1990’s top ten were still there in 2000. IBM topped the list in 1980 and 1990, but was off it entirely by 2000. Also off the list for 2000: Philip Morris (still profitable due to international markets, but tobacco was more and more a social pariah in the U.S.), Only Microsoft remained from the 2000 list.

We can go deeper on small, you go 00:21:27 [Speaker Changed] Micro cap and 00:21:28 [Speaker Changed] Deeper to a degree, our benchmark is still the Russell 2000 value index. I mean, and I immediately got the 80 20 rule. 00:04:40 [Speaker Changed] So you’ve previously discussed the epiphany you had at Harvard Business School.

Small-cap stocks continued their month-to-date surge as the Russell 2000 Index rose to an all-time high. Fixed income investments are subject to various risks including changes in interest rates, credit quality, inflation risk, market valuations, prepayments, corporate events, tax ramifications and other factors.

Valuations tended to crash and burn very, very cheap valuations tended to do well. In 1999, 2000. Right, right. Did the research found very compelling evidence that what its PE is really matters to your returns going forward. Very, very high. But of course, you know, Barry, I was 16, 17 much more interested in girls.

Sidebar, if you were in markets in the late 90's into the early 2000's, that last line might remind you of Alberto Vilar saying that Yahoo was going to be the next Yahoo. The valuation of CRCL might be a little bit stretched, it's also more than 20x revenue. Its stablecoin is USDC which is the second largest after Tether.

Valuations Matter, but Maybe Not as Much as You Think We absolutely pay attention to valuations, and the high valuations on technology is one of the reasons we didnt come into 2025 overweight in this group like so many others. The bottom line is that since 2000, the average year has gained 9.8%. But that drops to -12.5%

Financial Times ) A high P/E is not a stock market sell signal : Valuation is a terrible stock market timing tool. He is manager of the firms Technology Opportunities Fund (BGSAX), which has trounced the Nasdaq 100 and the MSCI World Net benchmarks since its inception in June 2000; his new AI-focused fund, the iShares A.I.

I hope we won’t go into a Hal 2000 type situation. The valuation of risk versus 00:46:33 [Speaker Changed] Reward 00:46:34 [Speaker Changed] Is something that I think a machine cannot do in the same way that human can. We do that, as I said, through understanding uncertainty, events catalysts and change.

npr.org) Health Measles cases are at their highest since 2000. defector.com) Why MLB team valuations are lagging other pro leagues. (theconversation.com) Why doctor groups are suing Health Secretary Robert F. Kennedy Jr. over vaccine recommendations. thehill.com) We continue to make progress on cardiac disease.

Dividends come from earnings, and so those are sort of anchors to valuation. It’s where tech bubble in 2000 is the classic example. Barry Ritholtz : He had a very famous Wall Street Journal piece In, like, late night fourteenth 2000. Present value of future cash flows, any asset is present value of future cash flows.

Nvidia is not the first giant tech company to trade at a rich valuation. Irrelevant Investor ) see also “No matter how you cut it, you’ve got to own Cisco” (2000) 23 years ago, Fortune magazine’s cover story about networking gear maker Cisco was published. We can’t compare things to the future, so we look to the past.

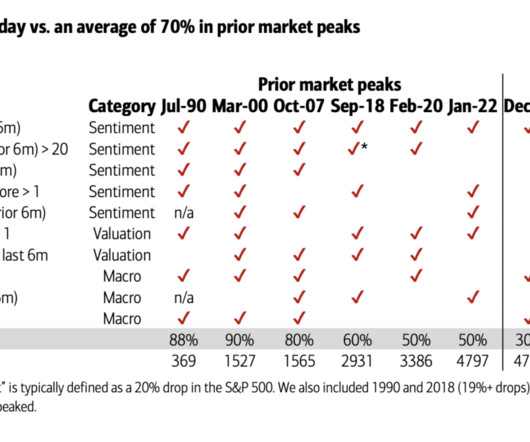

She observes it is less about the things investors tend to focus on — “technical analysis, geopolitics, behavioral finance and even skirt hemline trends” — and more about specific measures she tracks in sentiment, valuation, macro-economic areas. The table above shows the major market peaks going back to 1990.

This has made finding fundamentally sound stocks trading at reasonable valuations much easier in the small-cap space than in the S&P 500. Here are the current top 10 Russell 2000 stocks.

but the giveback off the highs was substantial: S&P 500 was down ~23%, Russell 2000 was off 27%, and the Nasdaq 100 came down 32%. But we won’t know how big a losing trade it might be until early 2024, when we see the updated valuations. Blame whatever you want – Too far, too fast? End of ZIRP? Too rapid rate increases? –

After lagging the S&P 500 for much of 2024, the Russell 2000 small cap index has staged an impressive rally in recent weeks. As smaller companies catch up to their large cap counterparts, investors may be wondering which Russell 2000 stocks look most attractive. over 10 years Manageable debt levels Projected 10-year return of 16.8%

from the most speculative level of valuations in U.S. history – exceeding even the 1929 and 2000 extremes, based on the valuation measures we find best-correlated with actual subsequent market returns in cycles across history. As of Friday, December 16, the S&P 500 Index is down -19.7%

No matter what metric you looked at, the peak valuations for growth stocks in mid-2021 were extreme. This is a chart of the valuation of the most expensive decile of our investable universe using the Price/Sales ratio. But even after that decline, the overall valuation remains about 30% above its average for the full period.

With our most reliable valuation measures more extreme than both the 1929 and 2000 market peaks, we continue to believe that the stock market is tracing out the extended peak of the third great speculative bubble in U.S.

Even with bear markets like 2000-2002 and 2008-2009, the portfolio had strong returns for a very long period. While some of that outperformance was due to improving fundamentals and earnings, most of it the returns came from the valuation investors assigned to these stocks. Source: [link].

The economy, inflation, interest rates and market valuations drive the key questions facing advisors. Does the tech stock landscape mirror the boom of 1996 or the bust of 2000? What will be the impact of Meta's inaugural dividend payment? Is now the time to increase allocations to international Markets?

By Justin Carbonneau ( Twitter | LinkedIn | YouTube ) — Over the past few weeks, I’ve seen a number of charts highlighting the opportunity in small-cap stocks given their absolute and relative valuations. The chart below, also from our market valuation tool, compares small cap value to large cap growth stocks. Only 12.4%

On December 6, the S&P 500 set the most extreme level of valuations on record, exceeding both the 1929 and 2000 market peaks on measures that we find best-correlated with actual, subsequent 10-12 year S&P 500 total returns across a century of market cycles.

The Russell 2000® Index (which tracks small-cap stock performance) was up only 0.44%. Are the Russell 2000’s weak returns a sign of slowing economic growth, or is the recent underperformance of small caps reflecting investor sentiment about current market opportunities? times earnings over the same period.

The Russell 2000 has declined 32% from its November 2021 high through June 2022—worse than the S&P 500’s 24% drop. And the Russell 2000 is now up 14.3% With the Fed swiftly raising rates and the slowing of economic growth, small-cap stocks have gotten pummeled. But that could be about to change, portends an article in Barron’s.

A client said – I understand market valuations are expensive but it doesn’t seem that it will correct much. The fundamental driver of market peaks and exorbitant valuations is the perception that there is nothing to worry about – there is no investment risk. There is nothing to worry about.

Investors may find opportunities at more reasonable valuations when comparing different asset classes across the market. For example, small caps have lagged the NASDAQ 100 this year, with the Russell 2000® Index of small-cap stocks down nearly 10% year.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content