This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

But that is incomparable to the 2008-09 era, where every financial institution had consumed CDOs, where toxic sub-prime loans were securitized into ticking time bombs. Therein lay a massive difference between 2008 and 2023. ~~~ Market turmoil to is often chalked up to fear and emotion, and with good reason.

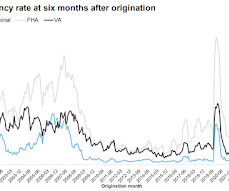

of 2024 vintage originations have been delinquent six months after origination, the highest share for any vintage since 2008 – outside of pandemic-era payment shocks Note that national mortgage performance is being impacted by the hurricanes. There is much more in the newsletter.

From December 2006, until she passed away from ovarian cancer on Nov 30, 2008, Tanta was my co-blogger. I will return on Thursday, Sept 5th (If I don't get lost!) In December 2006, my friend Doris "Tanta" Dungey started writing for Calculated Risk.

Also, contrary to popular belief that investment management has become commoditized, there was more demand for those services in 2022, while interest in financial planning dropped, according to a new study by the IAA and COMPLY.

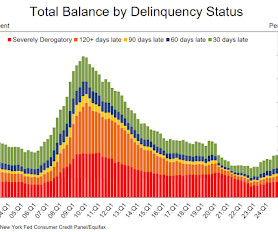

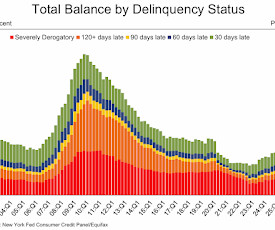

Household debt previously peaked in 2008 and bottomed in Q3 2013. About 126,000 consumers had a bankruptcy notation added to their credit reports this quarter, a small decline from the previous quarter. emphasis added Click on graph for larger image. Here are three graphs from the report : The first graph shows household debt increased in Q3.

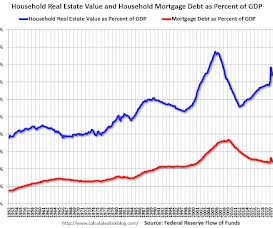

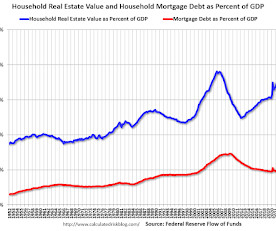

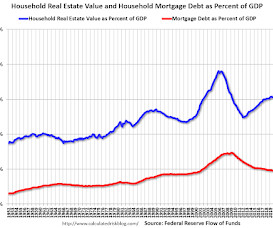

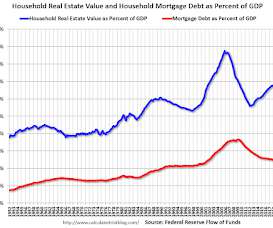

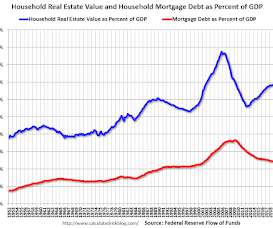

Household percent equity (as measured by the Fed) collapsed when house prices fell sharply in 2007 and 2008. Note that this does NOT include public debt obligations. The second graph shows homeowner percent equity since 1952. In Q1 2025, household percent equity (of household real estate) was at 72.0% - down from 72.2%

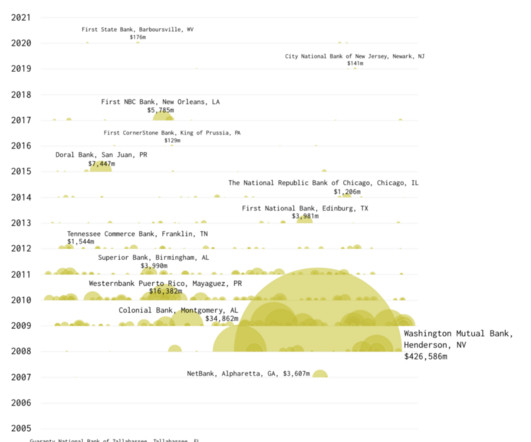

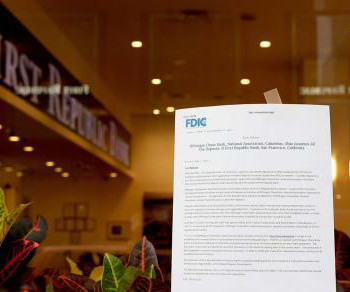

The graphic above, via Flowing Data , puts recent events into perspective: At $209 billion in assets, the Silicon Valley Bank failure since Washington Mutual crashed in 2008 (JPM Chase took them over from the FDIC). Bank failures since 2001, scaled by amount of assets in 2023 dollars. The post U.S.

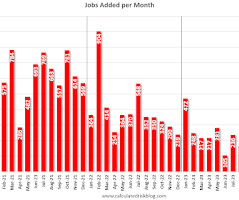

This graph really shows the collapse in retail hiring in 2008. Earlier: October Employment Report: 12 thousand Jobs, 4.1% Unemployment Rate Seasonal Retail Hiring Typically, retail companies start hiring for the holiday season in October, and really increase hiring in November.

He was also a Pulitzer finalist for his work covering the 2008 financial crisis. He has since reported from over 36 countries, holds two Gerald Loeb awards and eight prizes from the Society of American Business Editors and Writers.

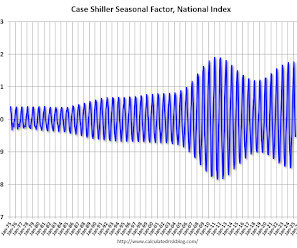

The peak MoM increase in NSA prices this year was the smallest since 2008! The seasonal swings declined following the bust, however the pandemic price surge changed the month-over-month pattern. The second graph shows the seasonal factors for the Case-Shiller National index since 1987.

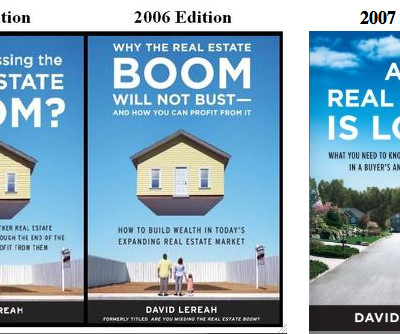

November 3, 2006) Tracking NAR Spin (April 23rd, 2008) Realtors Get Real (March 2007) Pending Home Sales Index, NAR Housing Market “Bottoms” (January 2008) How Counter-Productive is Realtor Association Spin?

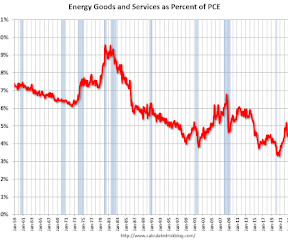

As is the increase in energy prices during the 2001 through 2008 period. In general, energy expenditures as a percent of PCE has been trending down for decades. The huge spikes in energy prices during the oil crisis of 1973 and 1979 are obvious. In April 2025, energy expenditures were at 3.6% of PCE, down from 3.8% in June 2022.

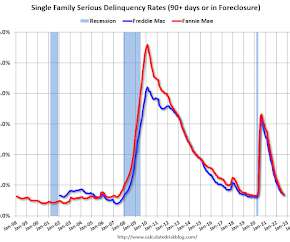

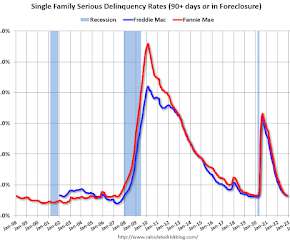

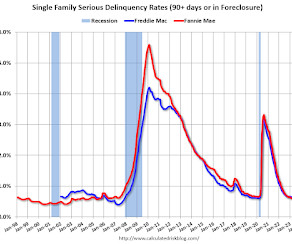

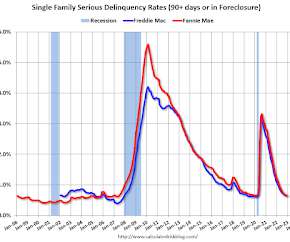

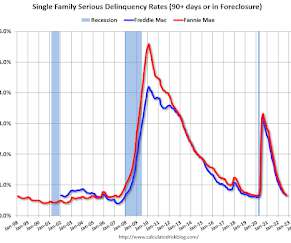

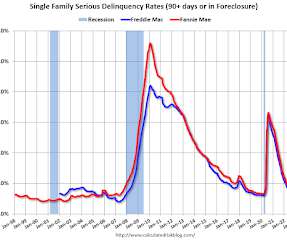

For loans made in 2005 through 2008 (1% of portfolio), 3.83% are seriously delinquent (down from 3.95%), For recent loans, originated in 2009 through 2021 (98% of portfolio), 0.55% are seriously delinquent (down from 0.57%).

For loans made in 2005 through 2008 (1% of portfolio), 3.49% are seriously delinquent (down from 3.71%), For recent loans, originated in 2009 through 2021 (98% of portfolio), 0.52% are seriously delinquent (down from 0.53%).

For loans made in 2005 through 2008 (1% of portfolio), 3.11% are seriously delinquent (down from 3.31%), For recent loans, originated in 2009 through 2021 (98% of portfolio), 0.48% are seriously delinquent (down from 0.51%).

For loans made in 2005 through 2008 (1% of portfolio), 3.49% are seriously delinquent (unchanged from 3.49%), For recent loans, originated in 2009 through 2021 (98% of portfolio), 0.53% are seriously delinquent (up from 0.52%).

For loans made in 2005 through 2008 (1% of portfolio), 3.71% are seriously delinquent (down from 3.83%), For recent loans, originated in 2009 through 2021 (98% of portfolio), 0.53% are seriously delinquent (down from 0.55%).

Household percent equity (as measured by the Fed) collapsed when house prices fell sharply in 2007 and 2008. Note that this does NOT include public debt obligations. The second graph shows homeowner percent equity since 1952. In Q4 2024, household percent equity (of household real estate) was at 74.4% - down from 74.7% in Q3, 2024.

The tool includes the option to run plans through real-life historical scenarios including the Great Depression, the post-war period, 1970s stagflation, the dot-com bubble and the 2008 financial crisis.

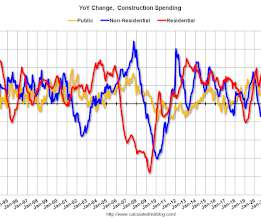

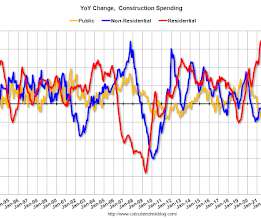

Non-residential (blue) spending is 19% above the bubble era peak in January 2008 (nominal dollars). Residential (red) spending is 36% above the bubble peak (in nominal terms - not adjusted for inflation). Public construction spending is 6% above the peak in March 2009. The second graph shows the year-over-year change in construction spending.

Credit Suisse is among lenders that have been defending themselves against claims over the sale of mortgage securities that plummeted in value during the 2008 crisis. It paid $600 million last year to settle a lawsuit with MBIA Insurance Corp over mortgage securities.

Non-residential (blue) spending is 24% above the bubble era peak in January 2008 (nominal dollars). Residential (red) spending is 35% above the bubble peak (in nominal terms - not adjusted for inflation). Public construction spending is 9% above the peak in March 2009. The second graph shows the year-over-year change in construction spending.

Household debt previously peaked in 2008 and bottomed in Q3 2013. Transition into serious delinquency, defined as 90 or more days past due, edged up for auto loans, credit cards, and HELOC balances but remained stable for mortgages. emphasis added Click on graph for larger image. rise from 2024Q3.

First Republic’s private wealth-management platform will become part of JPMorgan Advisors, which JPMorgan inherited from Bear Stearns when it bought that firm in 2008.

For loans made in 2005 through 2008 (1% of portfolio), 4.11% are seriously delinquent (down from 4.45%), For recent loans, originated in 2009 through 2021 (98% of portfolio), 0.60% are seriously delinquent (down from 0.63%).

Household percent equity (as measured by the Fed) collapsed when house prices fell sharply in 2007 and 2008. Note that this does NOT include public debt obligations. The second graph shows homeowner percent equity since 1952. In Q2 2024, household percent equity (of household real estate) was at 74.9% - up from 74.2% in Q1, 2024.

Household percent equity (as measured by the Fed) collapsed when house prices fell sharply in 2007 and 2008. Note that this does NOT include public debt obligations. The second graph shows homeowner percent equity since 1952. In Q2 2022, household percent equity (of household real estate) was at 70.5% - up from 70.1% in Q1, 2022.

2008 0.1% -2.5% Note: This table includes both annual change and Q4 over the previous Q4 (two slightly different measures). For 2024, I used a 2.6% growth rate Q4 over Q4. this gives 2.8% real annual growth). Real GDP Growth Year Annual GDP Q4 / Q4 2005 3.5% 2009 -2.6% 2020 -2.2% -1.0% 2024 1 2.8% 1 2024 estimate based on 2.8%

Below is a table showing Federal Reserve net income the vast bulk of which reflects net interest income from 2008 to 2024 (2024 is my estimate), as well as Fed remittances to the Treasury as shown in the Feds financials (more on this later).

Household percent equity (as measured by the Fed) collapsed when house prices fell sharply in 2007 and 2008. Note that this does NOT include public debt obligations. The second graph shows homeowner percent equity since 1952. In Q3 2022, household percent equity (of household real estate) was at 70.5% - unchanged from 70.5% in Q2, 2022.

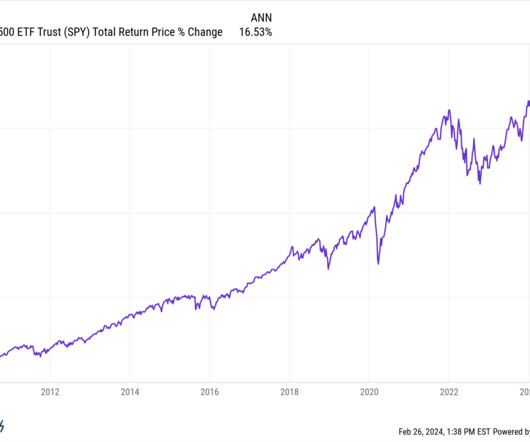

Despite 5% short-term interest rates and stickier inflation than some people would like and the Fed potentially pushing back interest rate cuts for a few months and the new True Detective seasons being a massive disappointment…the S&P 500 continues to take out new all-time highs.

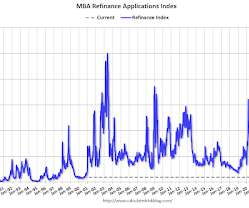

percent of all applications, which was the highest share since March 2008. The current 30-year fixed rate is now well over three percentage points higher than a year ago, and both purchase and refinance applications were down 38 percent and 86 percent over the year, respectively.” percent from 6.81 percent, with points decreasing to 0.95

Household debt previously peaked in 2008 and bottomed in Q3 2013. Transition into serious delinquency remained stable for auto loans, credit cards, and other debt. emphasis added Click on graph for larger image. Here are three graphs from the report : The first graph shows household debt increased in Q1. rise from 2024Q4.

Since 2008, the Census Bureau has included government transfers in its Supplemental Poverty Measure. ” In 2008. If this were true, it would mean we have been measuring income inequality incorrectly (perhaps wealth inequality as well). It is untrue. You may remember Phil Gramm. He’s the (thankfully) former U.S.

Job growth slowed in 2023 but was still historically strong. The second table shows the change in construction and manufacturing payrolls starting in 2006.

The other times this happened occurred in 1987, 2008 and 2020, some of the most volatile market environments we’ve ever seen. That’s a loss of more than 10% in just two days. loss was the fifth worse two-day stretch for the stock market since 1950. You can go an entire year without experiencing a 10% dra.

Coincident Index by States (May 22, 2008). The FOMC increases are having an impact. Previously : Signs of Softening (July 29, 2022). Why Recessions Matter to Investors (July 11, 2022). Soft Landing RIP (July 25, 2022). The post Coincident State Indexes (October 2022) appeared first on The Big Picture.

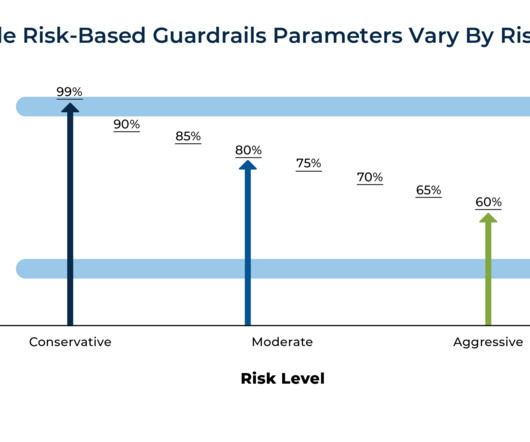

HiMaVs leverage the brain's natural preference for narrative and visual information by showing how a retirement income plan – such as a risk-based or guardrails-based strategy – would have fared during actual historical periods like the Great Depression, Stagflation of the 1970s, or the 2008 Global Financial Crisis.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content