This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

As a result, financial advisors should start honing the services Gen X members will likely benefit from the most, including retirement planning, estate and tax planning and mortgage refinancing. Between 2007 and 2010, they lost 38% of their median net worth, or $24,000, more than any other age cohort. trillion annually.

Let’s first look at the data: From 1959 through 2007, housing starts for single family homes in the U.S. These factors combine to make for an interesting setup for all sorts of housing-related construction and services as the housing market works to find an equilibrium. averaged more than 1.1 million per year.

His work covering the advisor tech space began in 2007 when he joined InvestmentNews as the advisor industry’s first dedicated technology reporter. Prior to his six years with WM , Janowski worked for Forrester Research as an analyst covering Digital Wealth Management. now Pontera).

When you get it wrong, it crushes your retirement plans. My own track record at making big calls is pretty damned good, but none of our clients wants me slinging around their retirement monies based on my gut instinct. The dotcom top, the double bottom in Oct 02-March 03; the highs in 2007, the lows 2009.

His work covering the advisor tech space began in 2007 when he joined InvestmentNews as the advisor industry’s first dedicated technology reporter. Prior to his six years with WM , Janowski worked for Forrester Research as an analyst covering Digital Wealth Management. now Pontera).

The services they offer are great differentiators and help make advisors a go-to resource for navigating the intricacies of retirement income planning (which is very complex), healthcare-cost planning (a too often overlooked major expense), and as an end-of-life services guide (in the case of bQuest). now Pontera).

He is the host of the Infinite Loops podcast and the author of How to Retire Rich , Invest Like the Best , and Predicting the Markets of Tomorrow. He was the director of systematic investing at Bear Stearns, leaving in 2007 to launch O’Shaughnessy Asset Management, now a part of Franklin Templeton.

By then, we began to have meaningful assets in our savings/retirement accounts and the bear markets had a bigger economic impact on those finances. 2000-13 : Secular bear market did not make new highs until March 2013 2018 : ~20% pullback as the economy slowed, FOMC hiked.

Actually, the lost decade up until the end of 2007 was pretty good for this concept using 25% into ULPIX instead of SSO. All three are from late 2007 and talk about me calling it a bear market and defensive action I was starting to take. The second backtest also cuts out the lost decade of the 2000's.

As a Retirement Income Certified Professional and a Life and Annuities Certified Professional, John advises clients on retirement planning, investment planning, and risk management. His primary focus is to help people align their financial decisions with their values and truths to live enriching lives.

It was 101% at the end of 2019, and 137% just before the financial crisis in 2007. That’s up from 183% at the end of 2019, and close to the 219% we had back in 2007, except now it’s happened without households taking on as much leverage. That’s up from 210% at the end of 2019, and 160% in 2007.

You hear the word recession and might be reminded of the Great Recession from late 2007 to mid-2009. Also, do not forget that liquidating your investments early may come with penalties or tax consequences, especially if you are pulling from retirement accounts, such as the Individual Retirement Account (IRA) or the 401(k).

In 2007, Kathleen began her career in the financial services industry with New England Financial. After serving for eight years as an active duty officer in the Army Corps of Engineers, she retired — but continued to commit herself to selfless service. Kathleen graduated from the United States Military Academy at West Point in 2000.

The Bloomberg article included a couple of quotes about dialing down the equity exposure in retirement which has been the default approach but that chart shows why dialing down is a bad idea. The simplest example would be the person to retired at the end of 2007 and then 12 months later, the stock market was 39% lower.

If you’re depending on income to fund your retirement, 5% rates are a blessing. 2007-09 Great Financial Crisis 7. ( A Wealth of Common Sense ) see also The Great and Awful Thing About These Interest Rates : The era of low interest rates is over. In the blink of an eye, the Fed went from punishing savers to punishing borrowers.

If you put 3% into Ariba Networks into a diversified portfolio in 2000 or bought a house you could comfortably afford in 2007 then you had a setback but weren't blown up. I posted the above joke on Bluesky a few days ago. This person will get blown up if anything bad ever happens, absolutely destroyed.

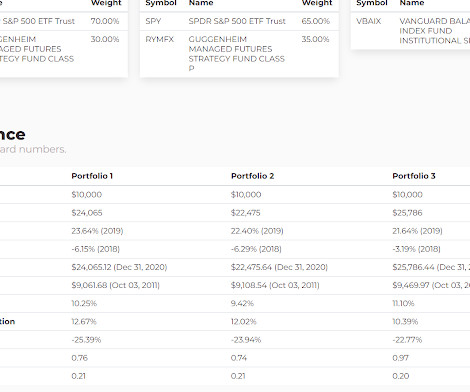

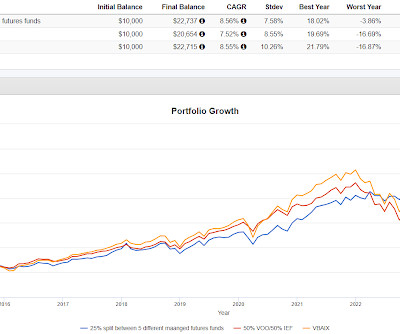

To my knowledge, RYMFX was the first managed futures mutual fund and it had the space to itself for several years after in launched in 2007. It has been challenging as we've talked about in other posts recently but I believe the 2010's were even worse. Check out the following. The backtest runs from the start of 2011 to the end of 2020.

For a little context, from the S&P 500's peak in October 2007 to the low in March 2009 when the index dropped 55%, VBAIX was down 37%. The 4% rule is of course the most basic, most elementary rule of thumb for sustainable withdrawals in retirement. this year versus down 24.8% for the S&P 500. The 4% rule was based on this too.

It’s been Walmart’s slogan since 2007 , and it’s a useful motto that can apply to your own life too. Improve your life by investing for retirement. We couldn’t talk about saving money without discussing the big “R”: retirement. A higher savings rate can help you retire sooner. Use a high-yield savings account.

The tendency toward negative correlation has certainly held up more often than not in my time with managed futures going back to 2007 when RYMFX first started trading as Rydex Managed Futures. Maybe, that wouldn't have been so bad. This gets us to the title of the post and Robinson's comments around how much to allocate to managed futures.

Then at some age beyond the typical range of middle-age, and advisor should be able to swing retiring financially speaking. Additionally it is my preference to not retire as I've mentioned many times so having a normal allocation to equities is not ideal in my case. I have about 20-25% in equity exposure.

The S&P 500 hit 1500 in March 2000, then again in the fall of 2007 and then the third and final time in January, 2013. The returns are not unprecedented, the 1990's were similar as one example but then when it ends, the "backside of the mountain" as Meb put it can be pretty rough.

Automatic enrollment has tripled since 2007. Outside of a retirement account, I see nothing wrong with holding six months of living expenses or something like this. Inside a retirement account, I can't think of a good reason why 9% of your portfolio should be earning next to nothing. This is a beautiful chart.

Yahoo comes to mind which I sold in the pre-market when the news was announced, this was maybe 2006 or 2007 and Kinder Morgan Partners when KMI was going to absorb it back in. I took the comment to mean put it into SCHD and live in retirement off the dividends (and Social Security too).

When I first was using a managed futures fund for clients, so talking 2007 or so, I stumbled into the idea that part of the past success came from interest earned on T-bills. Managed futures goes long and short some number of futures contracts that are collateralized by cash and cash equivalents like very short term T-bills.

Kathy Bostjancic: Given the severity of the last two recessions (the Great Recession in 2007-08 and the COVID recession in 2020), it’s likely not surprising that many investors think the next downturn could be just as severe. To add implications for consumers’ financial futures, many are concerned about their retirement plans.

One of the first reforms he put in place was setting a retirement age. According to this policy, the retirement age for directors was set at 70 and senior executives at 65. Mody was sacked after a messy scrap, Seth and Kerkar retired over the years as they crossed the age limits and Palkhivala quit citing ill health.

The S&P 500 fell an eventual 57% from its October 2007 peak before bottoming on March 9, 2009, and finally ending the global financial crisis (GFC) bear market. Retirement funds had been demolished and there was very little hope. For anyone who remembers that time, it was truly a frightening period in history.

Starting back in 2007 or 2008 I wrote about his barbell portfolio idea that goes very high risk with 10% of the portfolio in search of asymmetric returns and then very conservative with the other 90%. It's an interesting idea and if CAOS turns out to not be the answer, maybe something else in the future will be.

Here's a MarketWatch article quoting me in 2007 about managed futures. Try to figure out the simple and obvious questions and risks, make sure you're not over exposed to those risks and then diversify your diversifiers.

I wrote about it a couple of times for TheStreet.com, most recently on May 22, 2007. A funny note about PSP. The title of that article was Buyout Bust? Steer Clear of Private Equity ETF. Ok, I didn't like then, it's been a stinker and I would still avoid it.

A recent survey from the Nationwide Retirement Institute® uncovered topics business owners are looking to discuss including economic pressures and business-specific challenges such as access to capital, the tight labor market, employee benefits, and supply chain disruptions. Many are actively seeking the guidance of a financial professional.

Back in 2006 and 2007 there were far fewer funds available to help offset large stock market declines. There is a secondary, more subtle point that relates to portfolio construction and portfolio theory as we discuss here and as I have implemented into client accounts.

At Citi, in 2007, fantastic timing, you take over as Head of Structured Solutions. And so, 2007, I came over to Citi. And when you think about market timing was 2007 the best time to — to make a move, but it ended up being a perfect time actually long-term for — for my career. BITTERLY MICHELL: Always risk.

Read the article but substitute ETF anytime it uses the word alternatives or any synonyms because this article read like one of the countless late to the part articles about ETFs from 2007 to maybe 2010.

Retired or Limited Hermes Constance bag sizes. While the fashion Maison is still manufacturing all the above Hermes Constance sizes, various limited editions have been retired or are created in limited quantities/editions. The Hermes Constance 23 is a retired model introduced in 2007 and discontinued in 2009.

Even Mr. Money Mustache, as a person who retired 17 years ago, is still in this boat for the simple reason that my retirement income from dividends and hobby businesses is still greater than my annual living expenses (which still hover around $20,000 per year). (It’s the current blowup) -20% so far What’s your guess?

from September to October, the highest increase since February 2007.* The key to early retirement is making your Grape Nuts at home **I'm definitely less confident in this assertion than I was a couple of months ago The post How Much Does Inflation Cost? It's not just milk and gas. The question now is, where do we go from here?

Or you could look at the 2007 high which was within a few points of the 2000 high and say it took 12 years to double. From the high in 1968, it took 18 years to double which is a very long time of course. In the decade of the 90's it went up 4x which is very short for that sort of gain. From the high in 2000 it took until 2019 to double.

Years ago, maybe 2007, I said no to being a partner at my firm. I've talked a lot about the need to figure ourselves out to make sure we are targeting the outcomes we actually want. The work episode helped me better understand how much value I place on simplicity. The reasoning was very simple.

The fund has been around since 2007. The old school way to build this yourself would be to use the PIMCO Stocks PLUS Long Duration (PSLDX). It is leveraged up such that it offers 100% equity exposure and 100% long bond exposure.

Here's an article at theStreet.com from 2007 where I bagged on PSP. I would want to divide that sleeve up more if this was any sort of real portfolio I was going to implement. The standard deviation of the version with PSP is quite a bit higher. Average returns with high volatility. Then I looked at Dartmouth.

We like to look at the “prime-age” (25-54 years) employment-population ratio, since it gets around definitional issues that crop up with the unemployment rate (someone is counted as being “unemployed” only if they’re “actively looking for a job”) or demographics (an aging population with more people retiring and leaving the labor force every day).

It's total return CAGR going back to 2007 was +5.29% and price-only was -3.50%. The Cohen and Steers Closed End Opportunity Fund (FOF) was the one closed end fund of CEFs that I found, I'm sure there are others though. It currently yields 10.55%. The last five years though tell a much different story.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content