This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

While many firms have historically relied on commission-based compensation methods – reflecting a sales-driven approach – financial advice has evolved with technological advancements and a greater focus on financial planning, with the Assets Under Management (AUM) fee emerging as the primary compensation model.

Liz is the co-owner of Pleasant Wealth, a hybrid advisory firm based in Canton, Ohio that oversees $146 million in assets under management for 522 client households.

Training programs for new financial advisors have traditionally followed a sales-focused, sink-or-swim approach that primarily paid on commission for product sales. Some programs emphasize technical expertise, while others focus on communication skills needed to engage effectively with clients. Read More.

Traditionally, investment planning has been at the forefront of how financial advisors add value for their clients. Combined with growing advisor (and consumer) interest in comprehensive financial planning services, the number of ways advisors can add value for their clients has expanded greatly.

riabiz.com) DPL Financial Partners is seeing growth in commission-free annuity sales. advisorperspectives.com) Do financial advisers recommend annuities to their clients? (morningstar.com) A list of the most popular podcasts for financial advisers. linkedin.com) The biz Vestwell just raised a new $125 billion Series D.

Enjoy the current installment of "Weekend Reading For Financial Planners" - this week's edition kicks off with the news that the Department of Labor released the final version of its Retirement Security Rule (a.k.a.

Enjoy the current installment of “Weekend Reading For Financial Planners” - this week’s edition kicks off with the news that NAPFA has announced that it will no longer exclude advisors who receive up to $2,500 in annual trailing commissions from previous product sales, if they agree to donate that money to a non-profit organization (..)

Historically, the career path for newer financial advisors has followed a commission-based model that was focused on sales and business development first and learning the technical aspects of financial planning along the way. Read More.

Historically, the career path for newer financial advisors has followed a commission-based model that was focused on sales and business development first and learning the technical aspects of financial planning along the way. Read More.

Also in industry news this week: A recent study finds that having a defined marketing strategy is a linchpin of marketing success, as advisors with a defined strategy were more likely to have seen an increase in inbound leads during the past 12 months and have more confidence in meeting their practice goals during the coming year than those without (..)

Traditionally, investment planning has been at the forefront of how financial advisors add value for their clients. Combined with growing advisor (and consumer) interest in comprehensive financial planning services, the number of ways advisors can add value for their clients has expanded greatly.

Supreme Court decision shifting authority to interpret laws passed by Congress from Federal agencies to the judicial system could have significant impacts on regulation of the financial advice industry, including the potential for additional legal challenges to regulations from the Securities and Exchange Commission (SEC), the Department of Labor (DoL), (..)

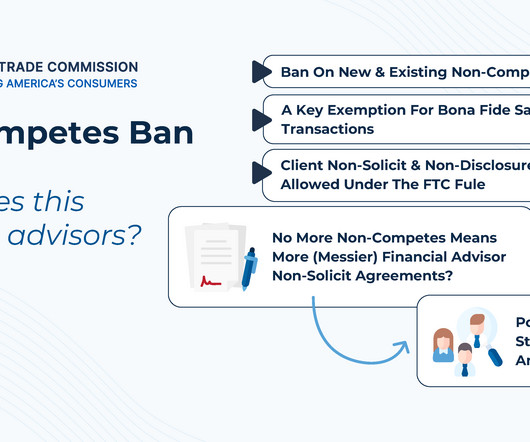

With these factors in mind, the Federal Trade Commission (FTC) in April of 2024 announced a final rule banning most non-competes nationwide that is expected to take effect (pending legal challenges) on September 4, 2024.

It is a massive Dunning Kruger : exercise in inexperienced but overly confident “ Finfluencers ” reducing complex issues involving money to a slick but misleading sales pitch. What’s dangerous here is that she’s well spoken, seems trustworthy, and comes across confident in her ability to do this for her clients.

Many times, though, they’ll tell me they’re really “bad at sales” or “bad at closing.” If it happens often, it can paralyze you from asking for the sale with confidence — and prospects notice the lack of confidence. Some advisors call this “commission breath.” When this is the case, it’s obviously a huge problem.

Michelle is a Wealth Advisor for Financially Wise Divorce, a hybrid advisory firm based in Minneapolis, Minnesota, that oversees $87 million in assets under management for 91 client households.

A fiduciary advisor is a financial professional who is legally obligated to act in the best interest of their clients. A fiduciary must always prioritize their clients’ needs above their own interests and mitigate or disclose any conflicts of interest that may arise. Not all advisors are fiduciaries.

Then any commissions earned from the sale of products, usually insurance products, are credited back to the client, offsetting and reducing the annual fee by the amount of the commission. A planner using a fee-offset model sets an annual fixed fee for their services.

Life transitions such as marriage, divorce, the birth of a child or grandchild, career changes, retirement, an inheritance, or the purchase or sale of a home can all influence your broader financial picture. These events may affect your investment approach, tax planning strategies, insurance needs, and estate planning documents.

Brad is the Co-Founder & CEO of Intellicents, an independent RIA with 12 offices across the country and headquartered in Albert Lea, Minnesota, that oversees $6 billion in assets under management for more than 3,000 client households.

Here is what makes us different: Hourly, Fee-Only Service: We operate on an hourly or, flat, fee-only basis, ensuring transparency and alignment of interests with our clients. Importantly, we do not accept salescommissions or any compensation beyond what is directly agreed upon with our clients.

Risk Factors Clients with unstable financial standing, such as state power firms, pose a threat to the company. With 36% of the overall loan book as of December 31, 2024, the company is also exposed to client concentration risk. EPC contracts are finished, and payments will go up in FY26. Mt, with its metal reserves surpassing 13.1

ZM disclosed in a Thursday filing with the Securities and Exchange Commission that it has fired Greg Tomb, who served as the company’s president. Zoom Video Communications Inc. The “termination without cause” is effective Friday.

Any financial advisor who is registered as an advisor with a regulator has to fill out this form for initial approval by either a state or a Federal (the United States Securities and Exchange Commission) regulator. The Form ADV Part I provides basic business detail about things such as ownership, clients, employees, etc.

You will Like: How Advisors Deal With High Net Worth Clients. Deciding to chase after bigger commissions and targeting high net worth clients, he begins his own firm selling penny and IPO stocks. Moreover, be aware of assets sold at a heavily discounted price (also known as a fire sale.) The Wolf Of Wall Street (2013).

How Conflicts of Interest Shape Financial Advice: A Conversation with Mike Garry and Amy Patterson Conflicts of interest in financial advice can greatly impact the recommendations that clients receive, especially from fee-only advisors. They do not earn commissions from selling financial products.

In the process of growing your accounting firm, building better client relationships is one of the most important elements of long-term success, and that starts with a robust client onboarding process. Table of Contents What is Client Onboarding? Why is Client Onboarding So Important?

Fee-only advisor – This is an advisor that does not charge commissions and hence is believed to be more aligned with the client’s best interests. A financial paraplanner is a junior wealth management professional who supports the research, operations, and client service activities of a financial planner.

Fee-Only financial advisors and firms receive no sales-related compensation or incentives. They are compensated only by the fee the client pays. In contrast, a commission-based financial advisor receives commissions or other forms of compensation from financial product providers for recommending and selling their products.

Fee-Only financial advisors and firms receive no sales-related compensation or incentives. They are compensated only by the fee the client pays. In contrast, a commission-based financial advisor receives commissions or other forms of compensation from financial product providers for recommending and selling their products.

Fee-only financial advisors Average cost: $200 to $400 an hour/ $1,000 to $3,000 per plan/ 1.18% to 0.59% of AUM Fee-only financial advisors are professionals who do not receive commissions from selling financial products. Instead, they charge fees directly to their clients for the services they provide.

The Company earns 11.66% of its revenue from the sale of products while the remaining 88.34% is from the sale of services. The Company’s clients include Coromandel, ArcelorMittal, Nirma, GlaxoSmithKline, Reliance & the Adani Group. The Company has 3 commissioned manufacturing units. Its FY23 revenue was Rs.

Financial advisors provide financial planning or investment guidance to clients. They generally provide advice to help their clients pursue their financial goals. . Most common is charging a percentage of assets managed on behalf of a client. The commission is not paid directly by the consumer.

With retail bakery and institutional segment included, bakery segment sales in Q3FY24 was Rs. It exports to 69 countries on six continents and provides its products to reputable institutional clients with a presence throughout India, in addition to retail customers in 26 states in India. 146 crores, up from ₹127 crores in Q3FY23.

Advisors have different fee structures where you can hire their services on an hourly rate, a retainer basis, or the assets under management (AUM) model where the advisor is paid a certain percentage as fee based on the amount of assets managed by him on behalf of his clients. Avoid paying commissions upfront to advisors.

It earned a net profit of Rs 35 crore on sales of Rs 44 crore in FY23 making it a penny stock with high net profit margin of 78.6% Avonmore Capital and Management Services earned a net profit of Rs 122 crore on sales of Rs 211 crore. Along these lines, it has commissioned two facilities for the expansion of its operations.

Hands-on jobs Administrative jobs Jobs that involve sales People-oriented jobs Highest paying jobs for creatives Computer jobs Expert tip How to apply for and get jobs that pay well without a degree How can I make $100,000 a year without a college degree? These sales jobs could be for you! There’s always money in sales!

At the top of my conflict list is sales contests , which basically tell brokers what “investment opportunities” to sell and give them a financial incentive (and, of course, firm-wide recognition to the winners, which is an incentive in itself) to recommend them to their unwary customers. Apparently not very effectively.

When choosing this, look for a planner with an active license, one who is accredited by a board or association, and one who has experience of working with clients of your profile. After all, if a client feels that a financial planner understands him, then he remains loyal to him. Are you looking for a financial advisor?

This is really none of my business, but I can’t help saying that I hate the new policy at the National Association of Personal Financial Advisors regarding trail commissions. The former partner was telling clients that the commissions on the products they were buying would be used, totally, 100%, to offset his fees.

Then there’s Blueleaf, which I subscribe to for my clients and find to be excellent on both accounts, but it’s not available to the DIY investor. They charge either a percentage of assets managed or a flat hourly rate that can run as high as several hundred dollars per hour, plus trading commissions and administrative fees.

The UK Financial Conduct Authority cited a number of concerns as it prohibited the sale of “cryptoasset” investment products to retail investors last year. Prohibiting the sale to retail clients of investment products that reference cryptoassets,” Financial Conduct Authority, June 10, 2020.

Watch as all h&#@ breaks loose discussing the question of broker vs. financial advisor, commissions, fees, value, and more! We talked about: What is the best, fairest fee model for the client? Does the way you are paid dictate how you serve clients? Does it matter that clients know the fees they are paying?

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content