This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

If you have any questions or would like to discuss your investment approach, were here to help. Tobias Financial Advisors is registered as an investmentadvisor with the SEC. Lets make sure your strategy continues to support your financial goals!

Let’s explore the role of investmentadvisors in helping individuals avoid these pitfalls and make informed decisions. By becoming an investmentadvisor, you can assist others in achieving their goals and strengthening your own financial journey. By diversifying investmentsadvisors can help with assetallocation.

Wealthfront Advisers is a registered investmentadvisor, and that means we have a fiduciary duty to act in your best interest. As part of that commitment, we are always looking for opportunities to help you earn more and keep more.

We make it easy by matching you to vetted advisors that meet your unique needs. Matched advisors are all registered with FINRA/SEC. Click to compare vetted advisors now. Rebalancing a 401(k) refers to adjusting the assetallocation of your investment portfolio back to its original target percentages.

Tax Loss Harvesting: Upside To A Down Market ajackson Thu, 03/26/2020 - 14:08 The market's path forward is extremely uncertain right now, but there are still planning steps that investors can implement today to generate positive results down the line. TAX LOSS HARVESTING: WHAT IS IT? Assets should not be sold solely for tax reasons.

Tax Loss Harvesting: Upside To A Down Market. Tax loss harvesting (the process of realizing a loss on the sale of an asset, in order to mitigate taxes on subsequent capital gains) is one of those planning steps. TAX LOSS HARVESTING: WHAT IS IT? TAX LOSS HARVESTING: KEY TAKEAWAYS. TAX LOSS HARVESTING 101.

Lack of choice: When you invest in an HF of a particular fund house, your investments are managed by the debt and equity team of the same fund house. When you invest separately in pure equity and debt funds, you are in better control to align the overall assetallocation suitable to your risk profile.

In stark contrast, Personal Capital is an investmentadvisor. This is absolutely key with any financial advisor you talk to, whether in person or online. You can also get information on your performance and assetallocation. They use several tactics as part of tax optimization.

An individual who learns to manage $4,000 a month after taxes will be equipped to manage $14,000 or even $40,000 a month as their earnings increase over time. By Lisa saving $6,000 into the plan, she reduces her federal taxable income to $94,000, meaning she will have a lower annual tax liability. Build Positive Financial Behaviors.

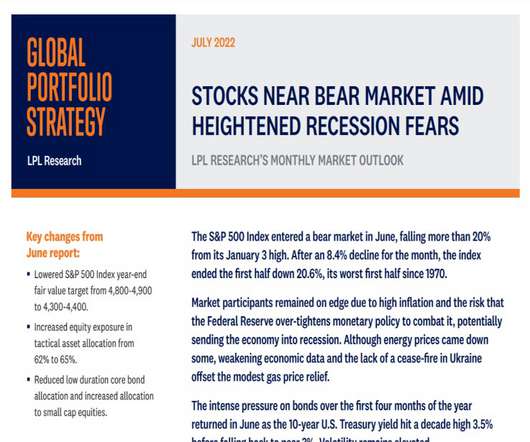

Increased equity exposure in tactical assetallocation from 62% to 65%. Reduced low duration core bond allocation and increased allocation to small cap equities. The Strategic and Tactical AssetAllocation Committee (STAAC) changed its recommended assetallocation for July, shifting from core bonds to small cap equities.

They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. All investments carry a certain risk and there is no assurance that an investment will provide positive performance over any period of time.

The Strategic and Tactical AssetAllocation Committee (STAAC) made no changes to its recommended assetallocation for August. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing. If sold prior to maturity, capital gains tax could apply.

When Malkiel is describing “a random walk”, he is saying that the short-run changes in the market are unpredictable, so using chart patterns, earnings forecasts or using an investmentadvisor is useless. If you’re just learning about investments, be sure to check out Part Four, A Practical Guide for Random Walkers and Other Investors.

With the advent of fractional shares available at some custodians , improved software for tax efficient implementation, and competition driving prices lower, the perfect storm for direct indexing appears to be now. Better After-Tax Result? Potential tax savings on an after tax basis. What is Direct Indexing?

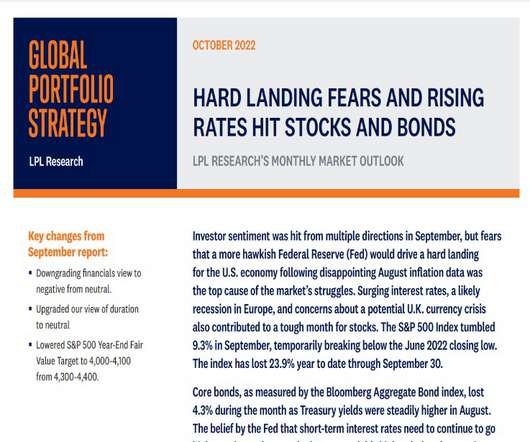

The Strategic and Tactical AssetAllocation Committee’s (STAAC) S&P 500 year-end fair value target of 4,000-4,100 is based on a price-to-earnings ratio of 17.5 To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

The Strategic and Tactical AssetAllocation Committee (STAAC) upgraded its view of duration to neutral. There is no assurance that the views or strategies discussed are suitable for all investors and they do not take into account the particular needs, investment objectives, tax and financial condition of any specific person.

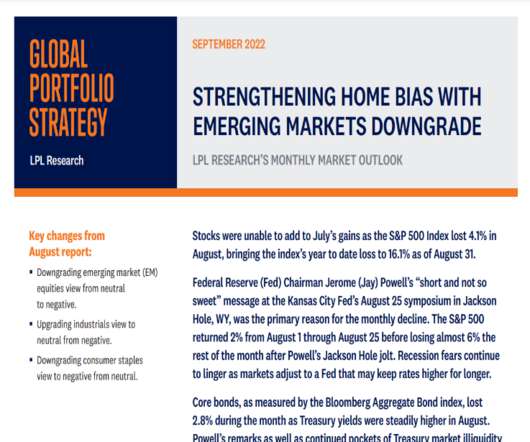

The Strategic and Tactical AssetAllocation Committee (STAAC) downgraded its view of emerging market (EM) equities in August. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing. Interest income may be subject to the alternative minimum tax.

Adapt your approach Late starters should consider a strategic shift in their assetallocation. Balancing risk with stable, reliable investments is crucial to minimize the impact of market volatility and ensure a steady income stream during retirement.

Their funds include Active funds, Absolute Funds, Liquid Funds, Overnight Funds, Gilt Funds, Tax Plans, Large Cap, Dynamic AssetAllocation Funds, and others. 26,644 crore, Quant ELSS Tax Saver Fund’s AUM of around Rs. 9,500 crore, Quant Tax Plan AUM is around Rs. 3,936 crore.

As with many things in life, the truth is somewhere between the extremes: While both simulated and real-world data suggest momentum may not be suitable as a driver of long-term assetallocations, we believe momentum considerations can be integrated in a cost-effective way to help inform daily portfolio management decisions.

You wouldn’t be surprised to learn the tax consequences of owning a mutual fund is a part of it. Tremendous track record, unusual background comes from computer science and software and, and pivoted into quantitative investing. And actually Ben Inker is the head of our assetallocation group. Really fascinating guy.

The scope of wealth management goes beyond traditional financial planning and investment advisory services, encompassing a more holistic approach to personal finance. Wealth managers collaborate with their clients to develop customized strategies for assetallocation, tax planning, estate planning, and risk management.

2 It is reasonable to assume a portion of that trading activity represented assetallocation changes motivated by market viewpoints, rather than buy-and-hold position accumulation. UNITED STATES: Dimensional Fund Advisors LP is an investmentadvisor registered with the Securities and Exchange Commission.

One of these options is a Roth 401(k) plan, which allows employees to contribute after-tax dollars toward their retirement savings. The primary difference between a traditional and Roth 401(k) is how they are taxed. However, you will have to pay income tax on the funds when you withdraw them in retirement.

Changes in their assumed rate of return can impact decisions ranging from assetallocation to the spending level that a portfolio can rationally support. McKinsey points out that the after-tax profit margin of publicly traded North American companies increased from 5.6% Thus, it’s important to have a view on this key question.

Changes in their assumed rate of return can impact decisions ranging from assetallocation to the spending level that a portfolio can rationally support. McKinsey points out that the after-tax profit margin of publicly traded North American companies increased from 5.6% Thus, it’s important to have a view on this key question.

They also offer tax advantages, such as tax-deferred growth or tax-free withdrawals with Roth accounts that can enhance your long-term earnings. However, these benefits also come with tax implications, so it is important to understand how these withdrawals will affect your taxable income.

Along with achieving strong long-term returns, protecting our clients’ capital is a critically important part of our challenge as investmentadvisors. An important tool in this regard is diversification, or spreading risk across various asset classes and investment opportunities, each of which has a different return profile.

Along with achieving strong long-term returns, protecting our clients’ capital is a critically important part of our challenge as investmentadvisors. An important tool in this regard is diversification, or spreading risk across various asset classes and investment opportunities, each of which has a different return profile.

Further, it helps to avoid concentrating all your money on investments that provide a return that is not at par with inflation, such as bank accounts, money market accounts, etc. Capital appreciation is one of the primary objectives of investing. Investing increases your money’s value by offering you returns over time.

Calculate your 2023 after tax income and expected after tax 2024 income. AssetAllocation and Goals. We are big advocates of time based assetallocation. Most people just build a big messy homogeneous basket of assets (don’t worry, we did that too and everyone on Wall St is trained to do it).

To be sure, the Biden administration, while focused squarely on its policy of transitioning the economy towards a non-fossil fuel environment, has been trying to alleviate the burden of rising gasoline and diesel prices by trying to introduce a federal gasoline tax holiday. The breakdown in savings comes from the 18.4 IMPORTANT DISCLOSURES.

The report examined the results of two types of funds7, each holding a mix of stocks and bonds: Balanced: Minimal change in allocation to stocks. Tactical AssetAllocation: Periodic shifts in allocation to stocks. As a thoughtful financial advisor once observed, “A portfolio is like a bar of soap.

Not that Robinhood is how they should be necessarily investing, but hey, it gets them interested in finance, it gets them thinking about money. It’s actually great and especially because you can do some basic kind of assetallocation models, so the robo-advisor… RITHOLTZ: Right. I could do my own taxes.

Daily portfolio management can spare investors from such style drift by rebalancing portfolios incrementally over time, keeping them focused on the targeted assetallocation and putting investors in a better position to capture higher returns. Please read the prospectus before investing.

Think of it like a one-time increase in the sales tax. But there were opportunities too, including potential rate cuts by the Fed and favorable tax policy from Congress. Securities offered through Cetera Advisor Networks LLC, Member FINRA/SIPC. Cetera Advisor Networks LLC is under separate ownership from any other named entity.

This would take any meaningful risk of tax increases on households or businesses off the table. Barry Gilbert , PhD, CFA, AssetAllocation Strategist, LPL Financial. Securities and advisory services offered through LPL Financial (LPL), a registered inv estment advisor and broker -dealer (member FINRA/SIPC).

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content