This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

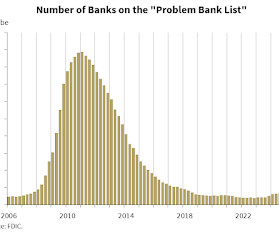

The PDNA rate for commercial real estate (CRE) loan portfolios is the highest it has been since fourth quarter 2014 at 1.49 While banks reported quarterly decreases in PDNA credit card loans (down $2.7 billion, or 9 basis points to 3.22 percent) and auto loans (down $2.6 billion, or 48 basis points to 2.84

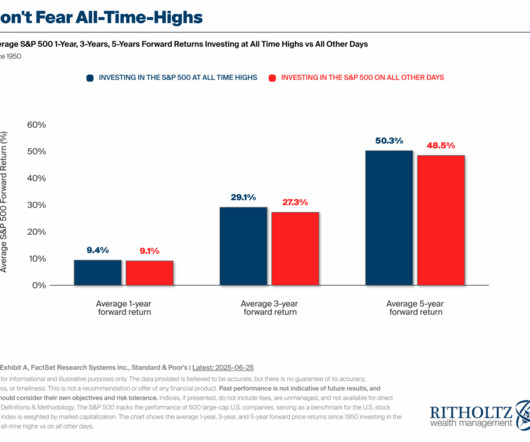

“One of the most bullish things that can happen to any market is for it to reach new multi-year highs.“ Bloomberg, March 5, 2014 Markets closed at a new all-time high today. ” A column I wrote for Bloomberg in 2014 pointed out that the Dow made 492 new all-time highs from 1982-1999; in the 12 years covering 1952 to 1965, it made 279.

2014 : Even with the U.S.’s Bloomberg, May 5, 2014 Big Picture mirror The Bonds That Can Cure America’s Ills A lot of what ails the U.S. The costs of funding the repair and renovation of Americas decaying infrastructure are as cheap as they have been since World War II. But the era of cheap credit may be nearing its end.

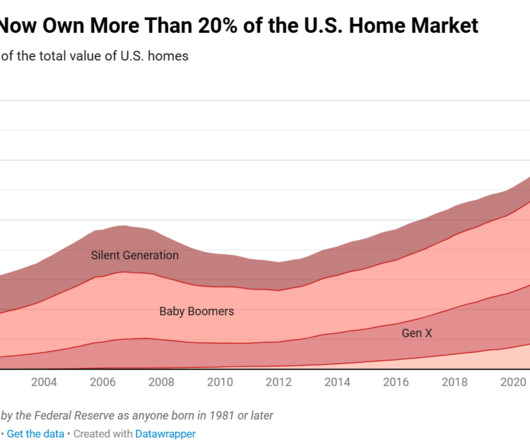

As I noted in 2014, demographics were positive for apartments, and more recently positive for homeownership. Note: This is using the 2023 projections main series. There will be plenty of "gray hairs" walking around in 2030, but the key for the economy is the large cohorts in the prime working age.

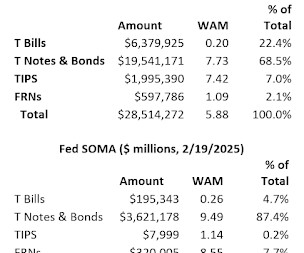

BILLION of Treasury notes and bonds (ex TIPS) that were not on its balance sheet at the end of 2023, with a weighted average maturity at the end of 2014 of 8.11 At the end of 2024, SOMA held $184.8 years, as well as 3.49 BILLION of TIPS not on its balance sheet a year earlier with a weighted average maturity of 10.52

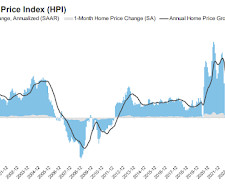

Source: ICE Home Price Index (HPI) Annual home price growth edged slightly higher in December, closing out the year at +3.4% That marks the lowest calendar year home price growth of any year since 2011 when the housing market was nearing its trough following the Great Financial Crisis In fact, 2024s growth was a full percentage point below the +4.4% (..)

The Paris Review, February 3, 2014) The post Tulipmania! Previously : 1 2 3 See also : Is This a Bubble? Ben Carlson, January 31, 2025) Tulipomania! appeared first on The Big Picture.

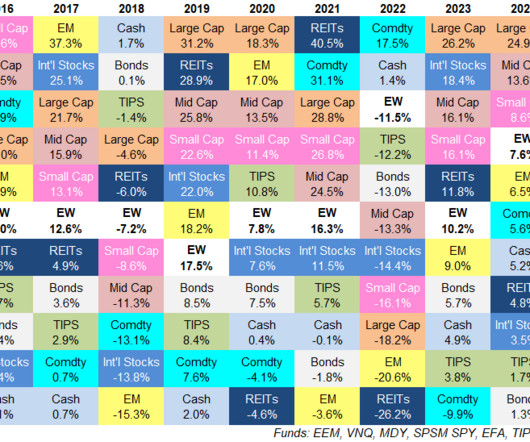

The first asset allocation quilt I created for this site covered the ten-year period from 2005-2014. Those returns look nothing like the last 10 years which is the whole point of this exercise. Here’s the latest quilt: Some observations: Inflation outperformed TIPS.The average inflation rate over the past 10 years was around 2.9%

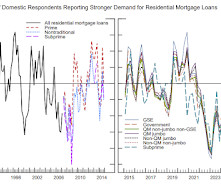

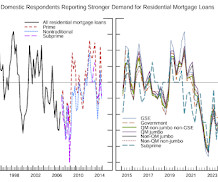

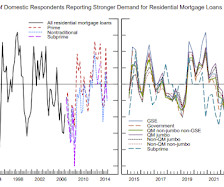

The left graph is from 1990 to 2014. This graph on Residential Real Estate demand is from the Senior Loan Officer Survey Charts. This graph is for demand and shows that demand has been weak since late 2021. The right graph is from 2015 to Q4 2024.

It quickly became a perennial favorite on Nerd's Eye View, and so I've updated it every year, with new lists of books in 2014, 2015, 2016, 2017, 2018, 2019, 2020, 2021, 2022, 2023, and a fresh round last year in 2024.

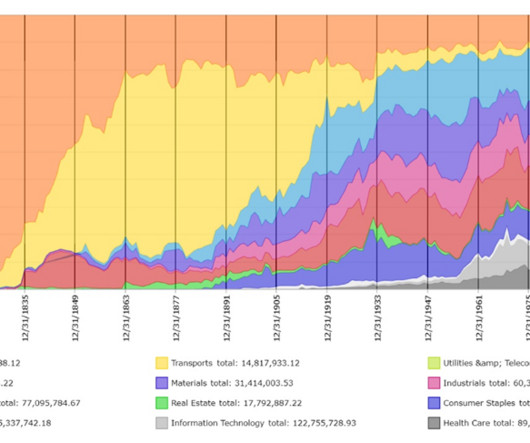

Bryan Taylor, Chief Economist at Global Financial Data, breaks these into seven distinct eras over the past 235 years: 1790 to 1840 The Bank of the United States Dominates 1840 to 1875 The Rise of the Railroads 1875 to 1929 The American Commercial Revolution 1929 to 1964 The First (..)

February 17, 2015) Click for video [link] Source: Economics Media Library The post The Daily Show: Wage Against the Machine appeared first on The Big Picture.

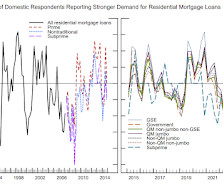

The left graph is 1990 to 2014. Standards tightened for all consumer loan categories; demand weakened for auto and other consumer loans, while it remained basically unchanged for credit cards. emphasis added Click on graph for larger image. This graph on Residential Real Estate demand is from the Senior Loan Officer Survey Charts.

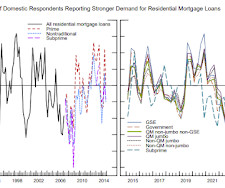

The left graph is from 1990 to 2014. This graph on Residential Real Estate demand is from the Senior Loan Officer Survey Charts. This graph is for demand and shows that demand has been weak since late 2021. The right graph is from 2015 to Q1 2025.

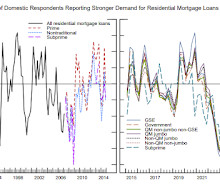

The left graphs are from 1990 to 2014. This graph on Residential Real Estate demand is from the Senior Loan Officer Survey Charts. This graph is for demand and shows that demand has declined. The right graphs are from 2015 to Q2 2024.

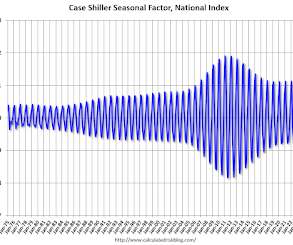

For in depth description of these issues, see Jed Kolko's article from 2014 "Let’s Improve, Not Ignore, Seasonal Adjustment of Housing Data" Note: I was one of several people to question the change in the seasonal factor (here is a post in 2009 ) - and this led to S&P Case-Shiller questioning the seasonal factor too ( from April 2010 ).

Between 2014 and 2024, Mason transferred client funds into his own accounts and those of the two entities without clients’ authorization, according to the SEC. Mason, who ran Rubicon Wealth Management, a registered investment advisor in Gladwyne, Pa., He pleaded guilty to all of the criminal charges.

The left graph is 1990 to 2014. Moreover, for credit card, auto, and other consumer loans, standards reportedly tightened, and demand weakened on balance. emphasis added Click on graph for larger image. This graph on Residential Real Estate demand is from the Senior Loan Officer Survey Charts. This shows that demand has declined.

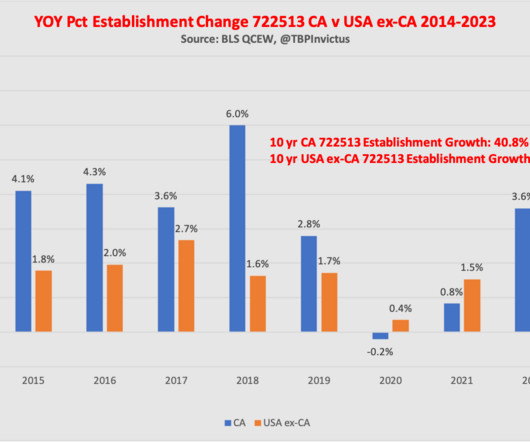

Let’s have a look: Over the 10 year period from 2014 to 2023, CA has grown its QSR workforce by 31.5% The fact that California has trounced the rest of the country over the course of a decade tells me much more than a relatively small loss over the course of three quarters. to only 19.5% to just 18.8%

Coming into 2025 the S&P 500 had just two down years out of the past 15: 2010 +14.8% 2024 +24.9% We were all probably a little spoiled. Regardless of the reason for the recent swoon, we were due.

Real GDP Growth Year Annual GDP Q4 / Q4 2005 3.5% 2008 0.1% -2.5% 2009 -2.6% 2020 -2.2% -1.0% 2024 1 2.8% 1 2024 estimate based on 2.8% Q4 SAAR annualized real growth rate.

The SEC said on Friday that Pimco failed to disclose key information to investors about how swaps could impact its PIMCO Global StocksPLUS & Income Fund between 2014 and 2016.

This week, Michael Batnick, Cathie Wood, and Downtown Josh Brown discuss investing in innovation, AI fact vs fiction, how big Tesla can get, why Ark bought Nvidia in 2014, Zoom vs Google Meet vs Microsoft Teams, and much more! Welcome to the latest episode of The Compound & Friends. Listen here: Apple podcasts Spoti.

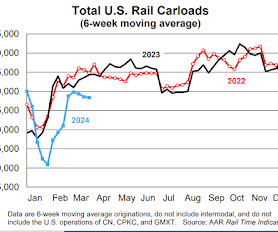

million units, virtually the same as the average for the first quarters from 2014 to 2023 (3.28 The second graph shows the six-week average (not monthly) of U.S. intermodal in 2022, 2023 and 2024: (using intermodal or shipping containers): U.S. railroads originated 1.02 It’s their seventh straight year-over-year gain. million).

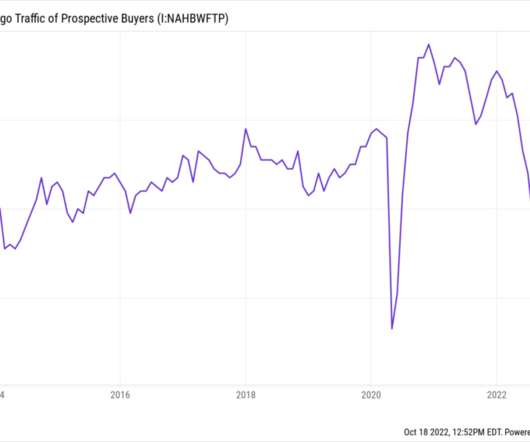

This brings us to the chart: The one above shows the traffic of prospective buyers looking at a new home (2014- 2022); the one below goes back to the 1980s. The four largest drops occurred during distinct periods of economic distress: 1990 (recession), 2006-09 (GFC), 2020 (pandemic/recession), and today (FOMC 300 bp rate hike).

In the past decade alone the total value of the housing market has more than doubled (from $23 trillion in 2014). According to Redfin, the U.S. housing market is now worth a stone’s throw from $50 trillion: Depedning on the day, that puts the housing market roughly on par with the total value of the U.S. stock market.

As I noted in 2014, this was positive for apartments, and more recently positive for housing. In 2022, the top 6 cohorts were under 45 (the Boomers are fading away), and by 2030 the top 10 cohorts will be the youngest 10 cohorts.

The number of salesperson's licenses started increasing again in 2014 (after house prices bottomed), and peaked again in early 2024 (ignoring weird pandemic distortion). The number of agents peaked at the end of 2007 (housing activity peaked in 2005, and prices in 2006). Click on graph for larger image. year-over-year. year-over-year).

This was written in 2014, but I never published it! A short comment on "short memories". Voters have "short memories". Sometimes "short memories" are good. Albert Schweitzer once said, "Happiness is nothing more than good health and a bad memory".

The Zillow index started in 2014, the ApartmentList index started in 2017, and CoreLogic in 2004. Today, in the Calculated Risk Real Estate Newsletter: Rents Continue to Decline More than Seasonally Normal A brief excerpt: OER and rent of primary residence have mostly moved together.

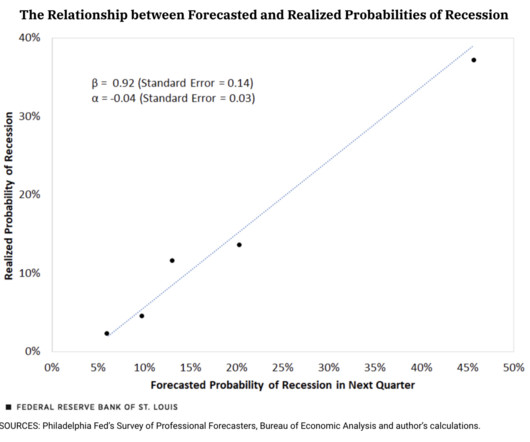

Random Shocks and Business Cycles by Thorsten Drautzburg Economic Insights, Q1 2019 Federal Reserve Bank of Philadelphia An astonishing record – of complete failure Tim Harford FT, May 30, 2014 The post Can Economists Predict Recessions? appeared first on The Big Picture.

How Greenspan Became the ex-Maestro (August 11, 2014). Previously : Farewell, TINA (September 28, 2022). Blame the Fed For Everything! June 9, 2022). Normalization vs Inflation (March 14, 2022). Who is to Blame, 1-25 (June 29, 2009). _. For the full calendar year 2020, the total return for the S&P 50 index was 18.4%; the 67.9%

The left graph is 1990 to 2014. Furthermore, standards tightened for all consumer loan categories; demand weakened for auto and other consumer loans, while it remained basically unchanged for credit card loans. emphasis added Click on graph for larger image. This shows that demand has declined. The right graph is 2015 to Q1 2023.

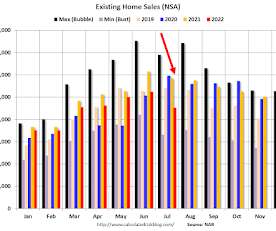

Sales are now below pre-pandemic levels and, excluding the pandemic decline, sales are the lowest level since 2014. Today, in the CalculatedRisk Real Estate Newsletter: NAR: Existing-Home Sales Decreased to 4.81 million SAAR in July Excerpt: ales in July (4.81 million SAAR) were down 5.9% from the previous month and were 20.2%

Using IRS data, University of California at Berkeley’s Emmanuel Saez and Gabriel Zucman’s 2014 study found: The share of total wealth of the top 1% has increased steadily, from below 25% in 1978 to 42% in 2012. And, it has accelerated over the past few decades. The share of total wealth of the top 0.1%

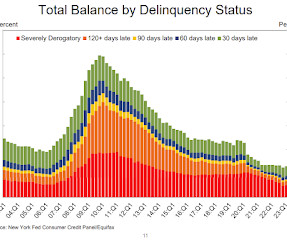

Mortgage originations, which include refinances, dropped sharply in the first quarter of 2023 to $324 billion, the lowest level seen since 2014. In total, non-housing balances grew by $24 billion. The volume of newly originated auto loans was $162 billion, a reduction from pandemic-era highs but still elevated compared to pre-Covid volumes.

For in depth description of these issues, see Jed Kolko's article from 2014 "Let’s Improve, Not Ignore, Seasonal Adjustment of Housing Data" Note: I was one of several people to question the change in the seasonal factor (here is a post in 2009 ) - and this led to S&P Case-Shiller questioning the seasonal factor too ( from April 2010 ).

Prior to founding Oak HC/FT in 2014, Annie spent 28 years at Oak Investment Partners, where she served as a Managing Partner and led the healthcare and fintech practices. This week, we speak with Annie Lamont, Co-Founder and Managing Partner of Oak HC/FT.

Since its 2014 inception, the fund has returned 9.7% You see this all the time: After a huge run of spectacular gains, the media fetes a manager, and buyers pour in late. The inevitable mean-reversion soon follows. The average ARKK investor has seen results far worse than the fund itself, according to data from Morningstar.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content