This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

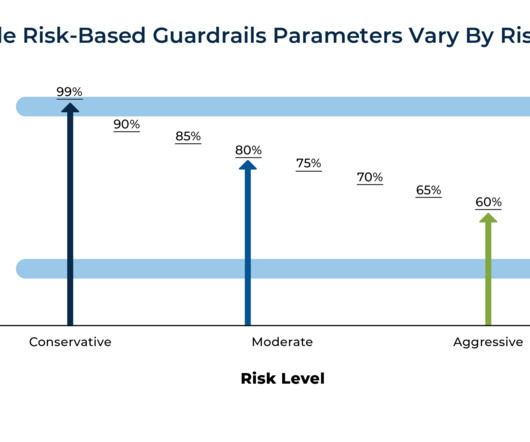

HiMaVs leverage the brain's natural preference for narrative and visual information by showing how a retirement income plan – such as a risk-based or guardrails-based strategy – would have fared during actual historical periods like the Great Depression, Stagflation of the 1970s, or the 2008 Global Financial Crisis.

But the numbers you can’t argue with, I mean, we all know that the brutal math of investing before costs investors collectively will earn the market return after costs. And then when I left the journal for the first time in 2008, they said, well, who should we hire to replace you? I did it in 2008 in oh nine.

Obviously math, there’s a ton of symbolic logic wherever you look, that classic syllogism, right? But in 2008 in the financial crisis, I turned 50. I find, you know, I was always in high school, my favorite math was, was geometry because everything was a puzzle to me. Absolutely. Everything will be fine.

The math is just Earnings * (Price / Earnings) = Price, since the Earnings parts cancel. So, we should be able to avoid a financial crisis, a la a 2008-style meltdown in markets and the economy. Its a way of getting a stock index price forecast by breaking it into two important pieces.

Top seeds have only lost to 16 seeds twice in the seeded era – since 1979 – and both occurrences are recent (that said, 2008 was the only year all four top seeds made the Final Four). Motoyuki Mabuchi went all-in with four aces in the main event hand of the 2008 World Series of Poker but lost to Justin Phillips’ royal flush.

And I did a lot of options math, which I thought was interesting. But it, it, summer of 2008, as you can imagine, was a really interesting time, particularly for the convertible bond desk because we were the busiest desk. 00:07:26 And then I moved on to the equities team afterwards. And I just learned a tremendous amount.

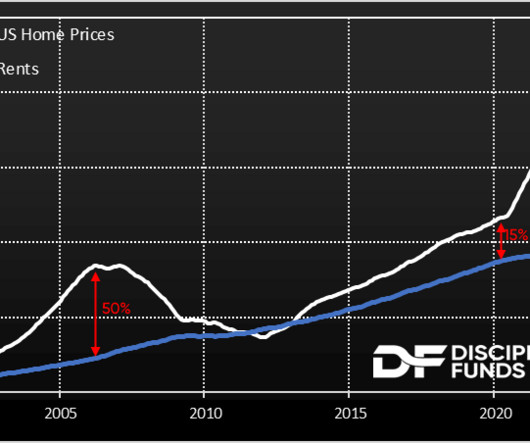

Since 2008, the Census Bureau has included government transfers in its Supplemental Poverty Measure. Call it ” ‘ America’s Enormous Math Mistake’s Mistake. ” In 2008. If this were true, it would mean we have been measuring income inequality incorrectly (perhaps wealth inequality as well). It is untrue.

In fact, we’ve been vocal that this isn’t a repeat of 2008. And that’s where the math on renting comes into play. Especially not in an environment where the demand for buying is drying up as the Fed raises rates aggressively and the average mortgage rate surges back to 7%. I don’t intend to sound alarmist.

By Ben Carlson I do the math, they do the physics. By Jeremy Schwartz Prudent lending was the concern in 1907; moral hazard was the concern in 2008. Max Exuberance and a herd mentality can exist without passive management present.

That is difficult to pull off but if you do the math on that it shows long term outperformance. As bad as 2008 was, we're 3x from there. He makes a good point about not relying solely on math to assess markets and portfolio construction, that the psychology of markets is important too.

The way portable used to primarily be implemented was to leverage up with correlated assets and it ended up going very badly in 2008 when equities dropped 40%. The risk to 40% or 30% of managed futures via leverage is that in a year like 2008, instead of going up like they "should," managed futures drops 15 or 20%.

I had my first child in June of 2008. Now, the first half of 2008, I was doing pretty well in the fund. But of course, I didn’t know the world was gonna meltdown in 2008. I bought Priceline on November 1st, 2008. And we would go on to sell that business to Microsoft in 2008. So here’s the math, Barry.

The way the math works, a 67% allocation to NTSX replicates 100% into a 60/40 portfolio which leaves 33% left over to do something. You can see the backtest proxy of RSBT has a slightly higher CAGR very similar standard deviation but a much better worst year which was back in 2008.

One, one is true and I’ve always said is that I wanted people to stop, ask if I could doing math. And no one asked me if I can do math anymore with a degree from Booth, particularly in econometrics and statistics. So people really ask you, you take French and can you do math. Two reasons.

I’d say management consulting is any of the other thing that least at that time was the other career trajectory, just my personality, more of a math oriented introvert. I could maybe flip that around a little bit since I think particularly post 2008, 2009, the quality style of investing has become a lot more popular.

Duke math professor Jonathan Mattingly claimed the average college basketball fan has a far better chance of achieving bracket perfection than one in 9.2 Motoyuki Mabuchi went all-in with four aces in the main event game of the 2008 World Series of Poker but lost to Justin Phillips’ royal flush. quintillion.

So like a component of it was like the standard derivatives math, right? And so like, you know, I got there and I learned derivatives math, right? And it stopped in like September of 2008. It was derivatives math, it was like working with the traders on like risk management. And so for six months there were no deal.

The maths are exactly the same. These sorts of math problems are the focus of this week’s TBL. Math Problems As this TBL goes live, just 16 games and one day of the NCAA Tournament are in the books, yet my bracket is a mess. We notice the unlikelihood of 100 in a row because of the pattern. Thanks for reading. quintillion.

It started on January 1 of 2008. SEIDES: In Warren’s 2008 annual letter, I think it was 2008, he made a statement. RITHOLTZ: So hold the duration risk aside with those two, but just for an investor in treasuries, I know you’ve done the math before. SEIDES: That’s right. So that’s how it came about.

And I did the math, and I think at that point in time, roughly speaking, assets in ETS were roughly just 10 percent, 12 percent of assets in mutual funds and I was pretty convinced that that number was to increase significantly. Think about the two founders of Global X, Bruno and Jose, they set up Global X in 2008. BERRUGA: Exactly.

But it was — on the other hand, it was just a great place, well, first to try it but the second thing is when 2008 came along, it was one of the few places that we’re making money. But it just didn’t become a great success. RITHOLTZ: Just not a great fit. ILMANEN: Yes. RITHOLTZ: Right. That makes a lot of sense.

It’s fun math – a 20% drop in prices means you get 25% more shares for your dollar, and a 50% drop means twice as many , or 100% more shares per dollar invested.). the current blowup) -20% so far What’s your guess? In today’s market, you are getting about 25% more shares for each dollar that you invest.

It didn’t happen overnight for me, but then few blogging resources were available when I started out in 2008. But a major in any common subject, particularly math or science, combined with above-average command of the subject matter are more important. But like everything else, you can learn how to blog.

It’s now up 35 percent since the SVB collapse, and the crypto faithful say it’s just more proof that the lack of trust in government institutions that led to Bitcoin’s birth following the 2008 financial crisis is alive and well. MIT Technology Review ) • How the World Is Spending $1.1

In the last 10 years (2008 through 2017), Berkshire’s shareholders’ equity per share and share price grew at 10.5% Buffett noted that the math of the buyback would get even better if Apple’s shares went down (but not its intrinsic value), something people often misunderstand. equity market. annually, respectively, compared with 8.5%

In the last 10 years (2008 through 2017), Berkshire’s shareholders’ equity per share and share price grew at 10.5% Buffett noted that the math of the buyback would get even better if Apple’s shares went down (but not its intrinsic value), something people often misunderstand. equity market. annually, respectively, compared with 8.5%

So I took it upon myself to go off and took a course in bond math, took another course in derivatives and realized the underlying fundamental concepts were barely, I mean, it wasn’t even high school math in most cases. And then I moved back to London at the end of 2008, which was a really interesting pivot.

To do math, neither maturity nor knowledge of human nature and experience are required. Back in 2008, then Exxon CEO Rex Tillerson noted that the company spends a billion dollars a day to run the business. Make sure you’ve got your math correct. The problem is corporate greed, collusion & profiteering.

MIELLE: After 2008? RITHOLTZ: 2008, ’09. MIELLE: And then the biggest luck of it all, is I joined Canyon in the ‘90s and there was a tsunami that literally lifted all waves of hedge funds from ‘90 to 2008 and even beyond. I guess other than Lehman Brothers, most of them were either rescued or absorbed into another entity.

I led the Union Square Ventures investment in Etsy, I became a venture partner for that, and then became a GP in the 2008 fund. And you know, the only thing math works on recognition by peers, and there’s some prizes. WENGER: Because I knew both Brad and Fred really well, and so it was kind of a natural thing to do.

As a matter of math, it cannot repeat the run from 8.5% Using Vanguard funds as proxies, VFINX for domestic equities and VGTSX for international equities, an investor who retired with $1 million on Dec 31, 2007 who immediately took out their 4% for 2008 would have had $576,000 at the end of 2008. in November.

00:03:14 [Mike Greene] So that was actually an outgrowth from my experience coming out of Wharton and you mentioned the, the, you know, the transition of people who tended to be skilled at math or physics into finance. In 2008, we didn’t have Uber, right? Very few people want to quote unquote, get onto a smartphone.

RITHOLTZ: Why is it not surprising that a math nerd is also a placekicker? But really, even that experience was about building great friends that I played football with. And many of those gentlemen have gone on to do incredible things as well. It seems to be like the field goal seems to be one of the most mathematical parts of football.

BRYANT: So money, unlike math, money is highly emotional. I mean, there’s 50,000 kids in the Atlanta public school system, so you can do the math there. I believe I love math because it doesn’t have an opinion, that’s a Melody Hobson quote. This was, so you had the 2008, 2009 economic crisis.

In 2008, S&P+PRPFX did worse than 60/40 by about 300 basis points and in 2022 it did better by about 350 basis points. The 75/50 captures 75% of the upside with only 50% of the downside, the math on that works out favorably over the long term. The two are pretty close. I have 75/50 in mind as sort of a benchmark.

Subscribe now Share The Better Letter Get more from Bob Seawright in the Substack app Available for iOS and Android Get the app TRIGGER WARNING: I’m going to do some sports math nerding-out this week. If that isn’t your cup of tea, I understand. This TBL is about football, but I really love to nerd-out over baseball.

RIEDER: — there was — and then, you know, punctuating with obviously 2008. How are we doing in literacy versus math versus science? And then in ‘94 and ’98, you know, all had a different stream to 2002. By the way, it seemed like every four years — RITHOLTZ: Right. Where are we?

My family and I moved to McLean, Virginia in, in 2008. And I was always good at math and, and I had been writing code since I was in the sixth grade. Who, who, who, who else did you speak to when you were there? What, so what was that experience like? Sean Dobson : I lived in Washington, DC for five years.

New York Times ) • Bond Yield Hits Highest Since 2008, Adding Pressure to Borrowing Costs : Bets that interest rates will fall have suppressed 10-year yields for most of 2023, but analysts warn that may be changing.

Yet the fundamental math of bond returns bodes well for 2023, our columnist says. ( Survival Lessons From Past Tech Downturns : The current tech downturn could be much worse than it appears now, say those who lived through the 2001 and 2008 crashes—but those who make it have the chance to fuel the next bubble. New York Times ). •

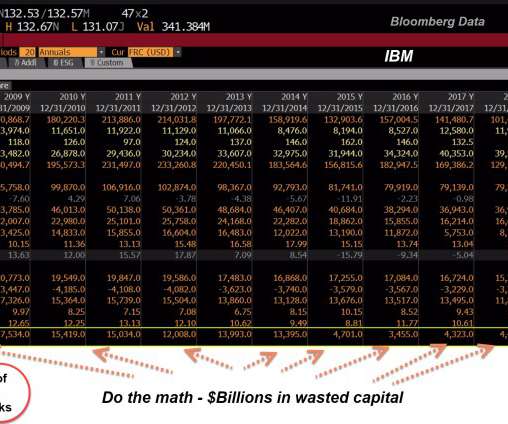

IBM Stock Buybacks since 2008 – Do the Math. However, the bigger issue is that stock buybacks have their roots in a deeper problem, stock option grants. But that’s another whole can of worms. I’ve been a long outspoken critic against stock buybacks for much of my career.

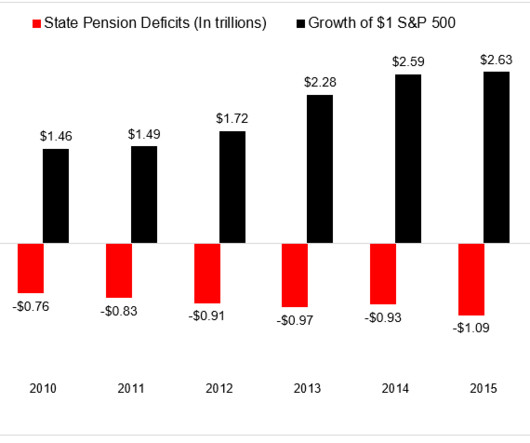

Sri Thiruvadanthai made the astute observation that "even if pensions had put all their money in stocks at the end of 2008, it wouldn't have made much difference to their funding status." If you're curious to learn how the math behind this, read this piece from Econompic. Not so fast.

So, I did the math, 20 million times a hundred. So, let me just repeat the math. And so, again, I went through this simple math. And so, it wasn’t just a fishing boat, it was an oceangoing factory, very impressive. And asked them, how much does one of these things cost, and they said, $20 million new.

Ben Clymer took a buyout offer from UBS in 2008 right in the middle of the financial crisis and said, “I know what I’m going to do. 2008, you launched a blog after you leave UBS in the midst of the financial crisis. RITHOLTZ: Hey, in 2008, that was not nothing. I know a little bit about that. CLYMER: It started for fun.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content