This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Nvidia is not the first giant tech company to trade at a rich valuation. Irrelevant Investor ) see also “No matter how you cut it, you’ve got to own Cisco” (2000) 23 years ago, Fortune magazine’s cover story about networking gear maker Cisco was published. We can’t compare things to the future, so we look to the past.

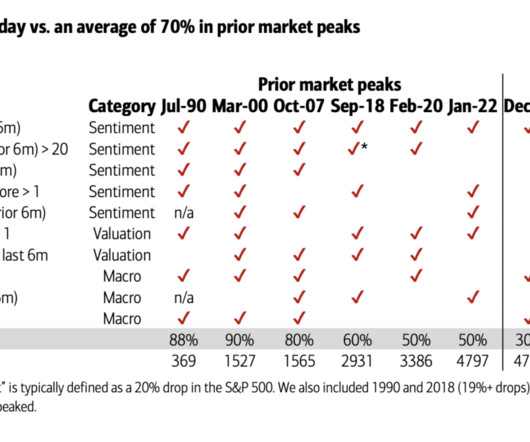

She observes it is less about the things investors tend to focus on — “technical analysis, geopolitics, behavioral finance and even skirt hemline trends” — and more about specific measures she tracks in sentiment, valuation, macro-economic areas. The table above shows the major market peaks going back to 1990.

but the giveback off the highs was substantial: S&P 500 was down ~23%, Russell 2000 was off 27%, and the Nasdaq 100 came down 32%. Recall John Kenneth Galbraith’s observation: “The only function of economic forecasting is to make astrology look respectable.” Blame whatever you want – Too far, too fast? End of ZIRP?

The Russell 2000, an index of 2,000 small-cap companies widely used as a benchmark for U.S. 7 This Week: Key Economic Data Tuesday: Consumer Confidence. Source: I nvestors Business Daily – Econoday economic calendar ; November 21, 2024 The Econoday economic calendar lists upcoming U.S. small-cap stocks, rose 4.50

Weekly Market Insights | December 2nd, 2024 Solid Gains for Thanksgiving Week Stocks posted solid gains over a short and busy holiday week as investors parsed fresh economic data, comments on potential future trade policy, and a few Q3 reports from technology companies. One area of concern has been the economic impact of proposed tariffs.

Even with bear markets like 2000-2002 and 2008-2009, the portfolio had strong returns for a very long period. While some of that outperformance was due to improving fundamentals and earnings, most of it the returns came from the valuation investors assigned to these stocks. Source: [link]. The yellow metal then saw two positive years.

The Russell 2000® Index (which tracks small-cap stock performance) was up only 0.44%. Are the Russell 2000’s weak returns a sign of slowing economic growth, or is the recent underperformance of small caps reflecting investor sentiment about current market opportunities? times earnings over the same period.

By Justin Carbonneau ( Twitter | LinkedIn | YouTube ) — Over the past few weeks, I’ve seen a number of charts highlighting the opportunity in small-cap stocks given their absolute and relative valuations. The chart below, also from our market valuation tool, compares small cap value to large cap growth stocks. Only 12.4%

He began with a single restaurant, a single cookie store, and eventually parlayed that into a series of acquisitions, mergers, expansions, ultimately leading to the Panera Bread concept, which now has 2000 locations and does about six and a half billion dollars. He sold the company in 2017 or so for about seven and a half billion dollars.

With the Fed swiftly raising rates and the slowing of economic growth, small-cap stocks have gotten pummeled. The Russell 2000 has declined 32% from its November 2021 high through June 2022—worse than the S&P 500’s 24% drop. And the Russell 2000 is now up 14.3% from that June bottom, outperforming the S&P 500’s 12.6%

Yields rose after traders speculated that strong economic data might persuade the Fed to raise rates. for the first time since 2007, while mortgage rates hit 8%–the highest level since mid-2000. Economic Strength, Housing Weakness The economy continued to evidence surprising strength according to data released last week.

How do you contextualize the economic data and the broad stamp recession when you’re thinking about managing risk? I had a buddy who in the late ‘90s, in early 2000s, the last time the dollar was as strong, was flying to Europe, buying 911s and Z8s, and other European sheet metal Ferraris, bringing them back to the U.S.,

Commentators continue to shout the doom-and-gloom forecasts of a hard landing recession, but after an economic hurricane in 2022 there are some signs the financial clouds have begun to lift this year. Investors Waiting for Another Flood While the calls for a hard economic landing remain, healthy GDP growth ( +2.9% 1, 2023).

For example, if the house brings in $2000 per month ($24,000 each year) and the sale price is $240,000, the next investor is buying a business with a price-to-earnings ratio of 10, because 240k/24k=10. But if you manage to convince someone to hand over $480,000 for that same house, youve sold at a P/E of 20.

at year-end can largely explain the compression in valuation, especially for higher multiple equities, primarily during the first half of the year. Since 1995, there are four rather distinct periods during which forward earnings estimates for the S&P 500 Index declined, tied to a specific event and/or economic downturn. by year-end.

A bachelor’s in economics from Northwestern and then an MBA from University of Chicago. And so I kind of leveraged that when I went to Morningstar because they’re very focused on quality, the whole concept of economic moats, but also about buying companies when they’re trading at a discount to intrinsic value.

Less than two years later, Palo Alto Networks purchased the company for $200 million—a more than 25-fold surge in valuation. In November 2015, Square, a San Francisco-based creator of mobile payment technology, went public at $9 per share and immediately rocketed 45% to a valuation of more than $4 billion. Not necessarily.

Although we expressed some worry about the long-term effects of mounting deficits, we concluded that stocks and other assets were not in bubble territory and represented good value despite what we saw as a weak economic recovery. If stocks with no earnings were included, the P/E ratio in 2000 would have been much higher than shown.)

Recent economic data has pointed to continued growth—giving rise to the “no landing” narrative. However, the pressure on valuations from higher interest rates, which have made bonds attractive alternatives, led to the Committee’s recent decision to reduce the size of the overweight from 5 points to 3.

There’s also quantitative metrics that we look at Those have evolved, but always within that capa, that cluster of high returns on investment stability across the economic cycle are consistent and strong balance sheets. In 2000, right. Going back to the eighties and nineties, I told you kind of the fundamental definition.

Rising economic and political risks— including weak global growth and increasing nativism and protectionism in several countries such as the U.S., For example, we found opportunity in small-cap stocks during their 2016 rally because of their relatively low valuations and limited vulnerability to flagging global economic growth.

Capital Market Magazine Capital Market is a fortnightly publication that analyses 2000 Companies and provides an in-depth analysis of the fundamental performance of the stocks, as well as their business operations. The article was published in ‘The Economic Times’ bringing lots of fame to the agency and its founder.

Small Caps Shine Small-cap stocks, as measured by the Russell 2000 Index, have pushed higher in recent weeks, which is a telling move for some Wall Street observers. The Russell 2000 has outperformed the S&P 500 by more than 4 percent during Q3 so far. 7 This Week: Key Economic Data Monday: Empire State Manufacturing Index.

We tend to be strategic rather than tactical in our approach to investing, but a combination of recent fundamental developments and valuation changes has caused us to add a note of caution in conversations with clients and in the management of their portfolios. From an economic perspective, growth in the U.S. In the U.S.,

We tend to be strategic rather than tactical in our approach to investing, but a combination of recent fundamental developments and valuation changes has caused us to add a note of caution in conversations with clients and in the management of their portfolios. From an economic perspective, growth in the U.S. Incremental Equity Risks.

1999, 2000, the internet was blowing up. The SNL crisis Tiger Chase had started, you know, in the wake of the internet melding down in 2000. I I was speaking at the Javits Center, 2000 people in the audience. If you think back to 2000, Amazon was the disruptor to Walmart or to Macy’s. And that was 25 years ago.

Investors Facing Rising Risks Need Solid Defense, Savvy Offense achen Mon, 09/12/2016 - 02:00 As rising economic and political risk fuels market volatility worldwide, investors need to maintain adequate liquidity, stability and diversification to shield against any protracted economic downturn. France and Germany.

As rising economic and political risk fuels market volatility worldwide, investors need to maintain adequate liquidity, stability and diversification to shield against any protracted economic downturn. Innovation and dynamism are alive and well despite several years of low economic growth. Mon, 09/12/2016 - 02:00.

However, this is actually a sustainable situation where market returns appear modest but are instead growing into their valuation. The leading economic indicator index was negative for the third-straight month, a historical flag for a looming recession. To many, it may look like the market has stalled. What to Watch.

In the short run, there can be distortions in public market valuations as we saw in 2001 and we saw prior to that in 2007, and prior to that in 2000, in ‘99. Valuations go up and you saw it, of course, in the late ‘90s, in the tech sector. You see these things before they start to show up in the economic data.

Bubbles can last a long time The good news is that these technological achievements can drive investments and economic activity for long periods of time. By 2000 investors were rabid dogs ready to invest in anything that could be associated with the net. I know what you’re saying. It can’t be done. Let’s find out.

This downturn has been driven by a combination of recession fears, disappointing earnings from major tech companies, the unwind of the Yen carry trade and broader economic concerns, including rising unemployment and shrinking manufacturing activity. On Monday, the U.S. Key strengths include: Large market capitalization of $295.7

.: Grantham, who is well-known for identifying bubbles before they burst such as the dot-com bust in 2000 and the housing market crash in 2008, has been outspoken about his belief that the market was in a “super bubble” that has yet to truly burst. Valuations are still high, despite rampant inflation and an economic slowdown.

For instance, the Russell 2000 index (which measures the performance of 2,000 smaller-cap companies) rose 1.90% this week, outpacing the S&P 500 and the technology-heavy Nasdaq. 6 This Week: Key Economic Data Tuesday: Consumer Price Index (CPI). Source: Econoday, June 9, 2023 The Econoday economic calendar lists upcoming U.S.

That metaphor is particularly fitting for economic and credit cycles. Investors in corporate credit are generally looking at the same risks as equity investors, and during times of economic or company-specific stress, value tends to shift “up” the capital structure—i.e., Test enterprise valuation. Test the worst-case scenario.

That metaphor is particularly fitting for economic and credit cycles. Investors in corporate credit are generally looking at the same risks as equity investors, and during times of economic or company-specific stress, value tends to shift “up” the capital structure—i.e., Test enterprise valuation. Test the worst-case scenario.

While new highs were set before bear markets in 1987, 2000, 2007, and 2020 in recent memory, the market has also made spectacular gains following new highs. In other words, the S&P has set more than 1,000 new highs since 1957, so investors shouldn’t treat them as a reason to worry or panic. They are perfectly normal.

Since 2000, the average increase in the 10-year yield during major moves higher is around 1.8%. As we know from historical precedents, when the Fed aggressively raises rates, economic growth slows or outright contracts, which is the Fed’s goal. Any economic forecasts set forth may not develop as predicted and are subject to change.

These planning opportunities are driven primarily by four factors: Materially lower market values for publicly traded securities, and a likely downturn in valuations of real estate and other illiquid assets. to a grantor trust) similarly remain attractive because of low interest rates and potentially low valuations.

These planning opportunities are driven primarily by four factors: Materially lower market values for publicly traded securities, and a likely downturn in valuations of real estate and other illiquid assets. to a grantor trust) similarly remain attractive because of low interest rates and potentially low valuations. Outright Gifting.

.: Grantham, who is well-known for identifying bubbles before they burst such as the dot-com bust in 2000 and the housing market crash in 2008, has been outspoken about his belief that the market was in a “super bubble” that has yet to truly burst. Valuations are still high, despite rampant inflation and an economic slowdown.

Investment Perspectives - The Great Debate achen Wed, 06/21/2017 - 12:35 Aside from some current political and economic topics that dominate the financial media, the most widely debated investment issue today involves the merits of passive investing, or indexing. Reflecting this pattern, Brown Advisory’s U.S. equity universe.

Aside from some current political and economic topics that dominate the financial media, the most widely debated investment issue today involves the merits of passive investing, or indexing. It underperformed primarily during very strong markets, as might be expected given its discipline with regard to valuations. equity universe.

I had an amazing 99 in early 2000, and I had left a hedge fund, so I was probably one of the few people to leave a hedge fund and go to a larger institution in the middle of the tech bubble. The best example I always love to give is that Amazon’s last private round was at a $60 million post money valuation. It was April of 99.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content