This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Would you like to diversify but also defer paying big capital gains taxes? I’m Barry Ritholtz and on today’s edition of at the money we’re going to discuss how to manage concentrated equity positions with an eye towards diversification and managing big capital gains taxes. And that’s the broad market.

apexmoney.com) Retirement Lessons from a 'faux retirement' including 'Balance is hard!' morningstar.com) On the math of early Social Security claiming. wealthmanagement.com) Taxes The traditional IRA looks less and less attractive. thinkadvisor.com) The interest rate the IRS charges on underpayment taxes is on the rise.

open.spotify.com) Retirement Nine things to consider in retirement. tonyisola.com) Retirement is, in part, about saying no to obligations you don't like. marketwatch.com) The retirement savings system is still way too complex. humbledollar.com) How to find abandoned retirement accounts.

wiredplanning.com) Christine Benz and Jeff Ptak talk retirement income with Kelli Hueler, CEO and founder of Hueler Companies. theirrelevantinvestor.com) Taxes Why clients need to start planning now for the coming dip in the estate tax exemption. thereformedbroker.com) Ten years of helping run a successful and fast-growing RIA.

(morningstar.com) Thomas Kopelman and Jacob Turner talk with Ankur Nagpal about tax considerations when selling a business. wiredplanning.com) Retirement Spending guardrails are important in retirement, but the details matter. wiredplanning.com) Retirement Spending guardrails are important in retirement, but the details matter.

podcasts.apple.com) Dan Haylett talks with financial advisor Ed Combs about the relationship challenges in retirement. awealthofcommonsense.com) On the math of a 0% line of credit. wsj.com) How do estimated taxes work? (ritholtz.com) Jesse Cramer talks with Peter Lazaroff about how to hang in there for the long run. Rockefeller.

million in assets to both retire and pass on a legacy interest (though many have yet to establish an estate plan), according to a recent survey. Enjoy the current installment of "Weekend Reading For Financial Planners" – this week's edition kicks off with the news that affluent Americans believe they need an average of $5.5

While a Roth conversion may never make sense for some individuals, for others, early retirement years may be the best time to convert pre-tax accounts to tax-free Roth. Your current and projected future tax rate is often a main component of the decision, but there are other considerations and benefits as well.

This is before we get to the issue of capital gains taxes, which create a hurdle of (minimum) 20% on those pesky profits just to get to breakeven. When you get it wrong, it crushes your retirement plans. Let’s add some color to the discussion on timing itself and add a little nuance.1 I sure as hell don’t want to either.

. $6300 in today's dollars goes a long way for us, that's quite a bit more than our fixed monthly expenses but might be about equal to regular monthly expenses plus once or twice a year type expenses like property tax, home owners insurance and so on. What's the risk to Social Security income?

Is retiring with a mortgage a good idea? Retiring with a mortgage doesn’t typically pose a financial risk, and at times it’s the best financial decision. But paying off a mortgage before retirement has upsides also. Here’s when it may – and may not – make sense to pay off a mortgage before retiring.

This article will explore how to navigate complex tax situations arising from multiple income sources, examining various income types, reporting requirements, self-employment obligations, and strategic approaches to record-keeping and tax planning that can help protect your financial interests. What is an RSU?

With the new year in full swing, tax season is just around the corner. Filing federal income taxes can be a long and complicated process, and mistakes are bound to happen here and there. As many of us know, these small mistakes can cost you big in tax returns and penalties. Is the Standard Deduction Right for You?

State Income Taxes – should we move? Thinking about moving to lower your state income taxes, or eliminate them? Do the math before you start packing. State income taxes should NOT be the primary decision-making point when considering moving in retirement 2. Take-aways: 1.

change at retirement. Hopefully a mortgage is paid off, hopefully there are no car payments to make and health insurance at 65, if retired, should go down quite a bit on Medicare, especially if income goes way down. Once someone is retired, saving for retirement is one less expense too. 5000 per for 15 years is $75,000.

First, is the math right based on my numbers? They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. If we guess just 2 billion people, and that is just a guess, and divide that into the 15.2 How can it solve anyone's problem?

In this article, well examine the nature of IRS audits, the common audit red flags that result in IRS scrutiny, and how professional tax advisors can help reduce the risk of you being audited. An IRS audit is a formal review of your financial records to verify their accuracy and compliance with tax laws.

Matt Kory, Vice President, Retirement Programs As a retirement income vehicle, the 401(k) is second in popularity only to Social Security – and as CNBC reported in 2019 the number of 401(k) millionaires is at an all-time high. But is a million dollars even enough for your retirement needs? Just think of the numbers.

Yesterday Ben and I did a show on retirement. Once they earn their first taxable income you impose a “Dad Tax” and extract a small amount, and then demonstrate your love by funding it to the maximum allowable with “Dad Dollars”. We should have a sense of urgency about retirement because it's coming, and there are no do overs.

Filing taxes in Idaho requires a clear understanding of the specific forms and regulations that apply to residents and non-residents alike. Navigating the tax landscape can be complex, but having a comprehensive guide to Idaho tax forms can simplify the process significantly. Obtaining Idaho tax forms is straightforward.

Filing taxes in Ohio requires a clear understanding of the specific tax forms mandated by the state. Unlike federal tax forms, Ohio tax forms are tailored to meet the unique tax regulations and requirements set forth by the Ohio Department of Taxation. Why Ohio Has State-Specific Tax Forms Each state in the U.S.

Filing taxes in Delaware requires a clear understanding of the specific forms and regulations that apply to residents and non-residents alike. Navigating the tax landscape can be complex, but having a comprehensive guide to Delaware tax forms can simplify the process significantly.

Part of the equation is that he is convinced that tax rates have to go up to pay for out debt and so converting to a Roth now before tax rates do go up will result in people ending up with more after tax dollars versus just going the RMD route at what is now 73 on its way to 75. This has been his thing for a long time.

Filing taxes in Minnesota requires a clear understanding of the specific forms and regulations that apply to residents and non-residents alike. Navigating the tax landscape can be complex, but having a comprehensive guide to Minnesota tax forms can simplify the process and help ensure compliance with state tax laws.

” In this week’s podcast, Tom and Casey debunk this common misconception by explaining the math behind required minimum distributions. In this week’s podcast, Tom and Casey debunk this common misconception by explaining the math behind required minimum distributions.

Filing taxes in Hawaii requires a clear understanding of the specific forms and procedures unique to the state. Unlike federal tax forms, Hawaii tax forms are tailored to meet the state’s tax laws and regulations, ensuring residents and non-residents alike comply with local requirements.

The latest retirement disaster article from Yahoo focuses on 55 year olds who have a "median savings of less than $50,000." Yahoo says it's "bleak" because this cohort is "only about a decade from retiring." A harsh reality is that $50,000 is not a retirement fund but it is a pretty robust emergency fund.

It's been a while since this sort of thing was relevant for my day job so something could have changed, weeklies didn't exist for example, but if my math is correct then it was way over exposed which would account for last week's decline in the fund price. Please leave a comment if I did the work incorrectly.

There was an article on LinkedIn (via Abnormal Returns) by Victor Haghani that dug into the math working against leveraged ETFs. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation.

The term personal finance ratios might be giving you flashbacks to math class. You can use ratios to keep track of many different aspects of your financial situation—from cash flow to savings to retirement and more. You can choose whether to use a gross figure or your actual take-home pay after taxes.

And checking in on the GraniteShares YieldBoost SPY ETF (YSPY) that sells put spreads on a levered S&P 500 ETF; Yes, that is a rough start, clearly, but interestingly the math checks out. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation.

And don't worry if math isn't your thing because we've included 50 30 20 budget spreadsheet ideas to help you stay on top of your budgeting strategies. You start off with your after-tax income , which represents 100% of what you have to work with, and then you work out the different spending groups from there.

The value of the S&P 500 index of stocks, where most of us hopefully have a good chunk of our retirement savings stashed into index funds, is up about fifty seven percent in just the past two years. Does this make it more vulnerable to a huge crash in the future, and will it affect my retirement? Its just basic math.

And don’t worry if math isn’t your thing because we’ve included 50 30 20 budget spreadsheet ideas to help you stay on top of your budgeting strategies. You start off with your after-tax income, which represents 100% of what you have to work with, and then you work out the different spending groups from there.

This is very important for retirement, and knowing what your target net worth by age should be will help you better understand how to reach your personal financial goals. Any medical debt, personal loans, or back taxes are also considered liabilities. Your retirement savings and investment portfolio should be well established by now.

Figure out how much money you make in after-tax income. More accurately, 70% of your take-home pay, or net income after taxes, not pre-tax income. Once you know your weekly or monthly income, you can do the simple math of calculating how much 70% would be. Consider some of these ways to save.

Bloomberg did a survey and found that Generation-X does not feel like it will be "financially prepared for retirement." Anyone closer to the younger edge of Gen-X could probably benefit by cutting expenses now, the impact of that could compound over the next 20+ years as they approach a normal retirement age.

Generally speaking, pensions are less viable than they used to be, the math doesn't work as well. The only pension I am remotely close to is the Arizona Public Safety Personnel Retirement System. The concept of pensions is that they provide a security net to retired workers. Is he right? Is he wrong?

Do the math, it would be a fantastic long term result but very difficult to pull off. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. Maybe the model providers don't really want their models to differentiate.

Calculation Breakdown Let’s break down the math to find out how much you could earn annually with a $30 hourly wage: Consider an average workweek of 40 hours and an average year consisting of 52 weeks. Keep in mind that this calculation represents the gross annual salary, not accounting for taxes, insurance, 401K, or deductions.

The course covers an introduction to personal finance, credit cards, life insurance, health insurance, investment instruments, loans, income tax and planning, budgeting and building a strong portfolio. Also, you will learn how to plan your taxes, credit score importance and how to budget your income to create a portfolio.

With this system, you will use 60% of your take-home pay to build your savings or even an early retirement account , invest, save up for a down payment, or repay debt. Another example is anyone interested in achieving FIRE; Financial Independence Retire Early. It includes the money you earn after you account for taxes.

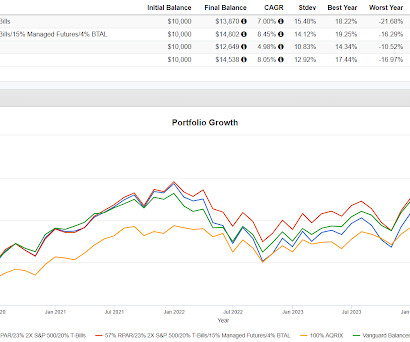

The way Portfolios 1 and 2 are weighted, the math works for being a 60/40 portfolio and then from there we add portable alpha/capital efficiency/return stacking. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation.

The simple 40 year trade for bonds of "number go up" is finished and as a matter of math, can't be repeated. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. Taking volatility out of a fixed income portfolio is fairly simple.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content