This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

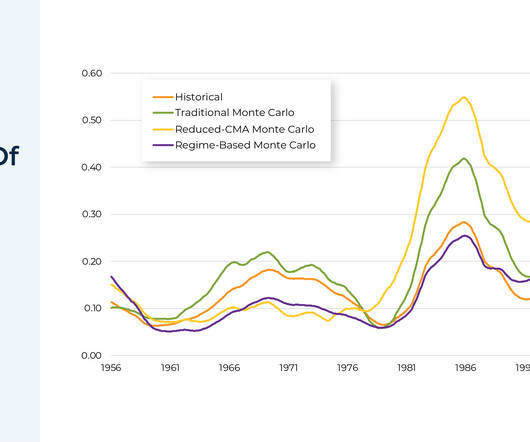

For many financial advisors, a core part of the retirement planning process involves simulating whether the client's assets will last through retirement. One way that advisors can help bridge this gap is by using Historical Market Visualization (HiMaV) as a more intuitive alternative for illustrating retirement income strategies.

The magic of having $1 million for retirement is no longer what it once was. million as being sustainable for a 25 year retirement assuming 4%/$50,000/yr. million as being sustainable for a 25 year retirement assuming 4%/$50,000/yr. How much do you have now and how much are you likely to have when you retire?

Compounding, Denominator Blindness, Survivorship Bias all affect our abilities to make good decisions about the future when even basic math is involved. If you are retiring in the next 12-36 months, you have a right to be concerned. How should a person who is approaching retirement NOT invest?

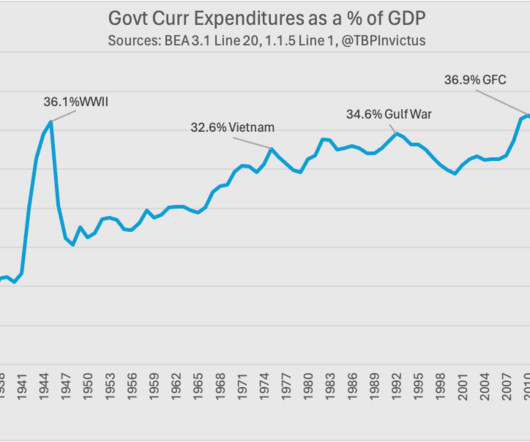

As Paul Krugman recently wrote on his excellent Substack , using a chart identical to the one immediately above (Paul used FRED ): “People may imagine that government is a bigger part of the economy than it is because of all the money we spend supporting retired Americans, covering their health bills, and so on [Chart 1].

My buddy could pay off his mortgage and car loans, pre-pay the kids colleges, fully fund retirement accounts, and still have cash left over. These two possibilities a 10-fold increase versus a 90% drop are roughly symmetrical in terms of math (but probably not probabilities). Torn about what to do, he asked my opinion.

While a Roth conversion may never make sense for some individuals, for others, early retirement years may be the best time to convert pre-tax accounts to tax-free Roth. Converting a traditional IRA to a Roth doesnt make sense unless you have cash to pay taxes without dipping into your retirement savings.

According to a recent survey commissioned by Kestra Financial and Bluespring Wealth Partners, less than half (41%) of first-generation advisors have transferred equity to successors, and just 6% of those planning to retire within 10 years have a fully documented succession plan. There was no succession plan coming.”

If that money is in an IRA, that is going to change your math considerably due to having to withdraw all of that inherited IRA within 10 years. Maybe you have very few moving parts or have many more moving parts but it is important to realize that no one's retirement plan will be done in by everything going exactly as planned.

Let’s be honest, retirement isn’t what it used to be. The traditional blueprint of working until 65, collecting a pension, and retiring feels outdated, especially for mid-level professionals who’ve started thinking early about what their ideal retirement should look like. What’s the earliest you can retire?

And the way math works, you end up with a stock that goes up a bunch. And you’re going to see a big sea change in the next three to five years of asset managers and RIAs optimizing taxable tax, and then non-taxable retirement accounts for various type of investments. And that’s the broad market.

Self-employment tax calculations and considerations When examining the math behind self-employment taxes , the total 15.3% Self-employed individuals enjoy unique advantages when it comes to health insurance and retirement planning. rate is comprised of two components: 12.4% for Medicare, which has no earnings cap.

Math errors and typos Minor mathematical errors and typos can disrupt the IRS’s automated processing systems and can result in discrepancies that can flag your return for manual review. Taking early withdrawals from retirement accounts Withdrawals before age 59 are scrutinized due to the potential complexity of penalty exceptions.

The value of the S&P 500 index of stocks, where most of us hopefully have a good chunk of our retirement savings stashed into index funds, is up about fifty seven percent in just the past two years. Does this make it more vulnerable to a huge crash in the future, and will it affect my retirement? Its just basic math.

Demand is likely to continue as more and more people in the Boomer generation reach retirement. If you’re good with math, then turning to financial planning or accounting or opening up a similar company could be one of the best recession proof businesses to start!

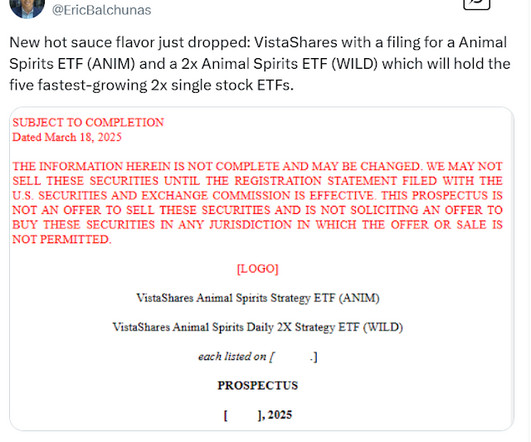

There was an article on LinkedIn (via Abnormal Returns) by Victor Haghani that dug into the math working against leveraged ETFs. Eric Balchunas from Bloomberg was baffled because the 1x version only has $60 million in AUM and trades about $1 million per day.

Podcasts Barry Ritholtz talks retirement with Christine Benz, author of "How to Retire: 20 Lessons for a Happy, Successful, and Wealthy Retirement." ft.com) Retirement Three things about retirement that Christine Benz has changed her mind about. wsj.com) On the bankruptcy risk of CCRCs. What Gen Z is facing.

And checking in on the GraniteShares YieldBoost SPY ETF (YSPY) that sells put spreads on a levered S&P 500 ETF; Yes, that is a rough start, clearly, but interestingly the math checks out. YSPY sells put spreads on a 3x fund. Oddly, the fund page no longer mentioned targeting a 2x outcome, it appears to now say 3x.

It’s sort of like math with dollar signs attached to it. But, 00:51:57 [Speaker Changed] And and what about, you know, we always have clients who are looking into their retirement, you know, I just want X dollars and not worry about taxes. It was about, you know, I love math statistics, all that stuff. I really like it.

I can walk you through the math or simulate a few scenarios. Compounding asymmetry : Over time, the inverse ETF may underperform due to daily resets, even if AMZN trends downward. Would you like to model how this plays out over a week or month with hypothetical returns?

But the numbers you can’t argue with, I mean, we all know that the brutal math of investing before costs investors collectively will earn the market return after costs. I realized I had enough to retire if I wanted to. But learning how to spend in retirement. So I made a plan to get out of there. It varies enormously.

For example, Michael Moore, famous for being one of the few people who predicted Donald Trump’s election win in 2016, confidently declared that Mr. Trump would not win again in 2024 ( Do The Math: Trump Is Toast ). Happy Retirement, Paul! That’s further proof that even a stopped clock is right twice a day.

We’re serving family offices, we’re serving institutions, we’ve done acquisitions in, in the stock plan businesses, in the retirement businesses. They want a financial plan, they want some advice, they want to think about whether it’s saving for a home or college or, or retirement. Remember that.

Christine Benz wrote 4 Key Decisions for Early Retirement. Really though, the word early could be removed from the title of her article because they are relevant questions for any retirement age. There's no single right path or template for retiring. Will you continue to work? What lifestyle changes do you plan to make?

Most professionals approaching retirement know they need a plan. Retirement is no longer just about 401(k)s and Social Security. This article is a deep dive into healthcare costs in retirement. The overlooked cost of retirement: Healthcare expenses Let’s start with a number most people underestimate, by a lot. to 2 times.

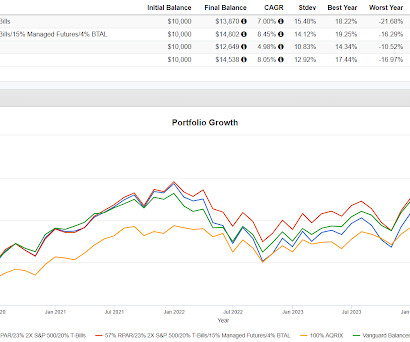

Do the math, it would be a fantastic long term result but very difficult to pull off. Maybe the model providers don't really want their models to differentiate. Something like a 75/50 portfolio might fit in the discussion of endowment style. 75/50 seeks to capture 75% of the market's upside with only half the downside.

Yeah, you have to, you know, the conceit of finance is that basically the math is all there is to it. So you mentioned half math, half Shakespeare. Let’s talk about the math side. Ivanka said, oh no, you don’t have to be able to do math to do real estate 00:20:13 [Speaker Changed] Or investing for that math.

Wasn’t the Excel spreadsheet error, which changed their math. Problem is, the math doesn’t work 01:20:33 [Speaker Changed] Well, you know, math, who really believes numbers should add up. My dad was in the military, so we lived all over the place. I mean that was, that was the problem.

It was not, not an unknown, like many of my, you know, retired predecessors are, you know, when they joined Vanguard in the eighties, it was really off the radar. Vanguard had to be a really interesting place. What was it like during that period? Karin Risi : It was an interesting place. We were starting to gain traction.

The way Portfolios 1 and 2 are weighted, the math works for being a 60/40 portfolio and then from there we add portable alpha/capital efficiency/return stacking. As I read the FT article, I had a thought about how to try to make the fund work as part of diversified portfolio, not the entire portfolio.

And when I went there I was gonna be a lawyer and I was gonna major in mathematics and I took my freshman year math and that all went great. And it turned out that half of that class had been the US National Math team and they had all competed internationally and they knew stuff I didn’t. McKinsey is a mandatory retirement age.

New York Times Magazine ) • Wall Street Math Wizards Are Decoding Private-Market Returns : A small band of quants is shining a light into the shadowy world of unlisted assets. But It Is Fighting Back. As revolutionary new weight-loss drugs turn consumers off ultraprocessed foods, the industry is on the hunt for new products. (

Simple math, it looks like the carry index has compounded at less than 3%. This next chart from Bloomberg compares just the carry component of the FOXY fund to the S&P 500 and T-Bills. The black line for carry looks like it is somewhat uncorrelated which is different than negatively correlated. The red line for T-bills is price only.

Advisors offer insights on retirement, long-term care, or market trends over lunch at a local café or conference room. One advisor noted that these events draw not only current clients but also curious prospects who are actively exploring retirement planning options. How do I promote an advisor event effectively?

And so I realized I was going to have to invest and save for my own retirement. I couldnt figure out where it came from; so I worked out the canonical math. I happened to live in a country that, uh, doesn’t have a functioning social welfare system or safety net. And if you understand asset allocation, you understand finance.

We'll start with a couple of different links on the same topic of having enough money or better put, figuring out how much you need to have for whatever your idea of a successful retirement is. If this couple planned it out well, maybe their $2000/mo mortgage gets paid off right as they are retiring.

Do the math before you start packing. State income taxes should NOT be the primary decision-making point when considering moving in retirement 2. State Income Taxes – should we move? Thinking about moving to lower your state income taxes, or eliminate them? Take-aways: 1.

econbrowser.com) How retirement can open you up to new possibilities. humbledollar.com) When it doesn't make sense to move in retirement. thinkadvisor.com) Peter Lazaroff talks with Jesse Cramer about the math behind car ownership. (morningstar.com) Bull markets have four distinct stages. peterlazaroff.com)

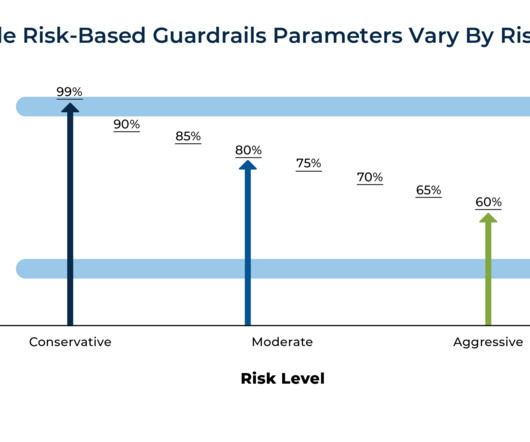

When planning for retirement, it’s effectively impossible to precisely forecast the performance and timing of future investment returns, which in turn makes it challenging to accurately predict a plan’s success or failure.

investmentnews.com) Research The problematic math of passing down generational wealth. blogs.cfainstitute.org) How life events affect retirement planning. wealthmanagement.com) Why 4% retirement withdrawal rates are still a thing. (riabiz.com) Archive Intel has entered the adviser communications archiving space.

humbledollar.com) Why planning in retirement is so challenging. humbledollar.com) Doing the math on a hybrid vs. conventional ICE. (downtownjoshbrown.com) What's driving stock market returns? awealthofcommonsense.com) 11 financial mistakes to avoid including 'Not carrying umbrella coverage.'

open.spotify.com) Retirement Nine things to consider in retirement. tonyisola.com) Retirement is, in part, about saying no to obligations you don't like. marketwatch.com) The retirement savings system is still way too complex. humbledollar.com) How to find abandoned retirement accounts.

wiredplanning.com) Retirement Spending guardrails are important in retirement, but the details matter. thinkadvisor.com) Not everyone is happier in retirement. thinkadvisor.com) Moving states in retirement requires some careful planning. thinkadvisor.com) Solo 401(k) contribution math can be tricky.

whitecoatinvestor.com) RetirementRetirement is filled with all sort of irreversible decisions. nytimes.com) How time feels more precious in retirement. advisorpedia.com) Retirement accounts Just because you can contribute to an IRA doesn't mean you should. humbledollar.com) Don't be ashamed to take senior discounts.

apexmoney.com) Retirement Lessons from a 'faux retirement' including 'Balance is hard!' morningstar.com) On the math of early Social Security claiming. (podcasts.apple.com) The C Word What matters when your mortality stares you in the face. humbledollar.com) An appreciation of Jonathan Clements' work. Why you need a plan.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content