This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

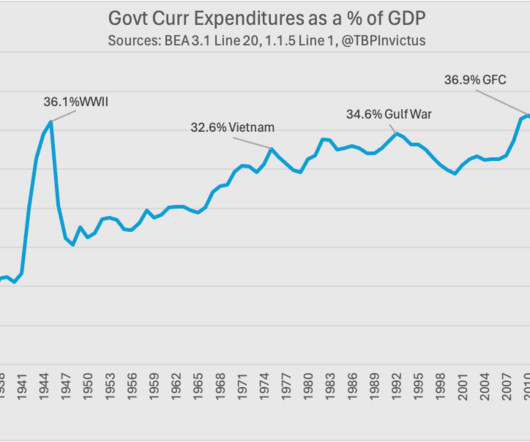

Let’s delve into a case in point of Coase’s theorem: If you wanted to peddle the narrative that government spending is out of control, you might present a chart like the one above, which is an exact replica of a chart that appeared recently in a piece of research from a major Wall St. investment firm.

It has further been estimated that as we approach retirement, this ratio increases to a factor of five times more pain for a loss as opposed to the joy we experience for a gain. There’s no shame in admitting that factor – for a lot of us, math can be very tough.

And the way math works, you end up with a stock that goes up a bunch. It’s not just going to be random, what everybody happens to present to you. We’ve done the math on some of these high-yield portfolios and taxable accounts. And that’s the broad market. We like to call it in house indexing.

If you adjust it for only the working age and retired population then inventory is even higher. And that’s where the math on renting comes into play. Or, at least, that’s true at present. In fact, housing inventory, by this metric, has never been higher.

Advisors offer insights on retirement, long-term care, or market trends over lunch at a local café or conference room. One advisor noted that these events draw not only current clients but also curious prospects who are actively exploring retirement planning options. How do I promote an advisor event effectively?

This is very important for retirement, and knowing what your target net worth by age should be will help you better understand how to reach your personal financial goals. You will likely want to retire in the next decade, so it's important to save and invest as much as possible while also not being too risky. Rowe Price.

Parents might not be able to spend hundreds of dollars on toys at Christmas during tough economic times, but they will still buy presents. Demand is likely to continue as more and more people in the Boomer generation reach retirement. Babies grow fast and constantly need new clothes.

Self-employment tax calculations and considerations When examining the math behind self-employment taxes , the total 15.3% Transportation costs present another substantial deduction opportunity. Self-employed individuals enjoy unique advantages when it comes to health insurance and retirement planning.

She has a really fascinating background, very eclectic, a combination of math and law. You, you get a, a BS in Mathematics and a JD from Boston University Math and Law. It is something, math has always come easy to me since a child. I didn’t get an advanced degree in math. Not the usual combination. What happened?

I think as presented, this will go very poorly for him but he does say that he would be shocked if his portfolio looked like this three years from now which makes another point, as presented this doesn't really let him take full advantage of the equity market's ergodicity.

Calculation Breakdown Let’s break down the math to find out how much you could earn annually with a $30 hourly wage: Consider an average workweek of 40 hours and an average year consisting of 52 weeks. Let’s do math again! Retirement/Savings $832.00 . $30 an Hour Is How Much a Year? Utilities $300.00 Groceries $300.00

I’m pleased to present you with a list of low cost financial advisors! They charge $495 per month for on-going investment management, retirement planning and financial advice as-needed. Retirement Portfolio Partners. Advisors who don’t take the time to present their fees this way aren’t transparent!

The BRM, more formally known as the Price-to-Earnings ratio or P/E, is supposed to be based on a mathematical estimate of the present value of all future dividends you will receive if you hold a stock for the entire life of the company. In short, the short term BRM is just a measure of the present moment’s balance of greed and fear.

Parents might not be able to spend hundreds of dollars on toys at Christmas during a tough year, but they will still buy presents. Demand is likely to continue as more and more people in the Boomer generation reach retirement. While they aren’t totally recession-proof, children's products tend to be recession-resistant.

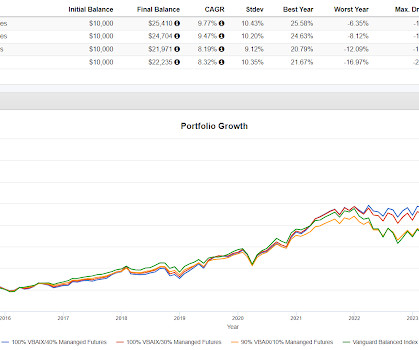

From page 6, "Because managed futures can benefit from both rising and falling markets, so long as trends present themselves." What if trends don't present themselves, meaning what if they don't persist? The Aspect paper mentions the risk sort of. They mention it without acknowledging it. In 2008, VBAIX was down 23%.

As a financial advisor or other investment professional, you’re no doubt already well aware that the “math” side of the conversation is a large part of what your clients need help with every day. It’s just that the key here – as always – comes down to presentation and usability. Retirement Planning.

You can turn these earnings into the beginning of your retirement nest egg or even fund your college expenses in a few years! By starting your savings early , you could have millions of dollars by the time you get to retirement age just from saving small amounts. Wouldn't that be nice?

I — I loved math, but really, I was going to go down that literature route more than anything else and — and study Spanish literature. BITTERLY MICHELL: … difficult situations for those who were retiring, right, and those …. So he was President of the university for 35 years, very present — very, very present.

In the big picture, this usually leads to having a “successful” life, because of this basic math: Traditional Success. =. She had more than enough to retire , twenty years ago! To many people who are less fortunate, the present situation would still sound like great fortune, and in some ways, it is. How much work you do.

I have this one-hour presentation I do on money. RITHOLTZ: if you’re one latte away from your retirement being messed up you got bigger … SETHI: Bigger problems. RITHOLTZ: What are your thoughts on the early retirement fire movement? It’s much deeper than math. No kidding. And they would never show up.

With more money at our disposal, we maxed out our retirement accounts and invest in real estate, while we travel 12 weeks annually.” – Holly Johnson, Freelance Writer and Blogger at ClubThrifty.com Holly has become so successful as a freelance writer that she now offers a course helping others succeed on the same path.

Most professionals approaching retirement know they need a plan. Retirement is no longer just about 401(k)s and Social Security. This article is a deep dive into healthcare costs in retirement. The overlooked cost of retirement: Healthcare expenses Let’s start with a number most people underestimate, by a lot. to 2 times.

We split the amount and bought a zero coupon bond of the present value upfront. SEIDES: And I put that in a presentation I had as he had just given his reason for losing the bet. RITHOLTZ: So hold the duration risk aside with those two, but just for an investor in treasuries, I know you’ve done the math before.

It was not, not an unknown, like many of my, you know, retired predecessors are, you know, when they joined Vanguard in the eighties, it was really off the radar. But of course, Jack Bogle was still sort of around his present on campus. Vanguard had to be a really interesting place. What was it like during that period?

But the numbers you can’t argue with, I mean, we all know that the brutal math of investing before costs investors collectively will earn the market return after costs. But that’s when the most amount of fascinating things happen and the most amount of opportunities present themselves. You went 95% into stocks.

And we literally talk about during the show, I got a tag to present to the SEC, about their new single stock product. I was the one reviewing marketing copy and doing presentations to groups of institutions about how to use the darn things. Let Mr. Market do his thing and we’ll find out how we did when we get ready to retire.

Financial education and the PowerPoint presentation. If you have a 401k, you may have been invited to sit down for some retirement education. In my experience, they give a PowerPoint presentation. Some were told they were not good in math, that this was not for girls, or that this is not a topic for Black people!

The biggest thing, though, was that my much-better-half retired. As you will see, to honor her retirement, students and former students lined the entire route from her classroom to our house to applaud her. The median loss in the present value of household lifetime discretionary spending for those aged 45-62 is $182,370.

In this regard, financial planning seems to differ from science, technology, engineering and math (STEM) careers where many women leave their jobs in their mid-thirties after a few years of experience on the job.” women tend to live longer, making it much more important to plan for a longer retirement) or a subjective one (e.g.

00:03:14 [Mike Greene] So that was actually an outgrowth from my experience coming out of Wharton and you mentioned the, the, you know, the transition of people who tended to be skilled at math or physics into finance. People earn wages, whether it’s a retirement account or a tax deferred account or just an investment account.

“ Let’s say you are doing a podcast about NJ Retirement and it isn’t creating any meaning response – no growth in subscribers, no leads, nobody in your NJ following mentions they are listening, etc. Is the topic of NJ Retirement well-suited for the audience? Am I not presenting it to enough people in NJ?

ANAT ADMATI, PROFESSOR OF FIANCE AND ECONOMICS, STANFORD GRADUATE SCHOOL OF BUSINESS: So, my journey starts where I took a lot of math. I was good in math and I love the math. So, I was kind of, in my romantic mind when I was in my early 20s, I was going to take but not give back to math, that kind of thing.

And when you saw the US Ag down 13% last year, for folks, again, who are investing for retirement and in their 529 plans, they’re not concerned about it. But when you translate that to folks who might have a heavy municipal bond portfolio, and those folks who are in retirement, and they don’t like principal losses.

Quick math: If you have $1.828 million in the bank. And , you have to do the math by hand. To What If Analysis, what if I pay… So I’m doing my cash flow planning in my retirement plan, and I say, You know, I don’t wanna have to pay for in as a retirement. There is an admin charge of about $49k.

” After the Dodgers were retired in order in the bottom of the eighth inning, Gibson swung his aching legs down from the training table to hobble toward the clubhouse. However, real love is as present as can be. We all struggle to be truly present. “How you doing, big boy?,” ” Lasorda asked. The coolest.

And I was a math nerd as a kid. You’re 34th, you’re retiring after 34 years and you trounce what’s really the more appropriate benchmark, I would assume the Russell 2000. And a third approach is compare price with the present value of future cash flows from here to eternity. You, you beat the s and p by 3.7%

Jan 10, 2023 The California Public Employees’ Retirement System is making a $1Bn wager that small private equity firms can boost the pension giant’s returns and clout [link] CALPERS has a knack for being late… adding money to two small private equity shops now? It is the opposite, except in the top decile.

If you’re anywhere from an individual to a pension fund, saying how much do I have to save to retire? My mom was a math teacher so — RITHOLTZ: Okay. My mom was a math teacher so — RITHOLTZ: Okay. He’s the genius in math. Now, if you’re sitting there saying, what do I need to retire?

So, I did the math, 20 million times a hundred. So, let me just repeat the math. And so, again, I went through this simple math. And so, I spent like couple days all night putting together the best PowerPoint presentation I could come up with explaining how cheap everything was in Russia. It is $2 billion on the ship.

And so this is one of the few places, really, in the world that unites my pre-Hodinkee and present-day world. RITHOLTZ: So wait, you’re, I’m trying to do the math, if you were 24 in ‘08, so you got this watch in 2000, 99? But this idea of presenting something that was just so much more thoughtful than anyone else out there.

Yeah, you have to, you know, the conceit of finance is that basically the math is all there is to it. So you mentioned half math, half Shakespeare. Let’s talk about the math side. Ivanka said, oh no, you don’t have to be able to do math to do real estate 00:20:13 [Speaker Changed] Or investing for that math.

I’d been ranked i i back in the seventies, if you can do the math. 00:19:54 [Speaker Changed] So you retired if it’s not working and you move on to the next that. Tell us a little bit about the plan for launching an independent economics research 00:09:15 [Speaker Changed] Shop. So at that point, I had a pretty big career.

RITHOLTZ: At least that’s how it’s presented. MORGENSON: And so you have pensioners at Bristol-Myers or Lockheed or Coors is another who are really relying on private equity to do the right thing for their pensions going forward, for their retirement, for their payouts when they need them. And so, you know where you stand.

I went there because I was fearful that being a professor would be like retiring in your 20s. SUNSTEIN: Okay, so one bias is present bias, where today really matters, and the future is a foreign country called later land, and we’re not sure we’re ever going to visit. And that actually has roots in the brain, present bias.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content