This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

That means if your retirementplan underestimates medical costs, you risk serious shortfalls. For instance, a retired government employee receiving a fixed monthly pension of ₹40,000 ten years ago might find its value significantly reduced today if inflation averaged around 6% annually. on June 6, 2025 , and cut CRR by 100 bps.

As a result, financial advisors should start honing the services Gen X members will likely benefit from the most, including retirementplanning, estate and tax planning and mortgage refinancing. trillion annually over the next decade as part of the great wealth transfer, a new report finds. trillion annually.

Understanding the Current Economic Landscape Before diving into goal-setting, it’s crucial to acknowledge the economic environment we’re navigating. Interest rates remain a significant factor in financial planning, affecting everything from mortgage rates to investment returns.

The post Investing for Retirement: Strategies for Long-Term Success appeared first on Yardley Wealth Management, LLC. Investing for Retirement: Strategies for Long-Term Success Introduction Investing for retirement is a journey that demands careful planning, patience, and discipline. What lifestyle do you envision?

Do you know when you want to retire? Are you saving enough for the retirement you want? In fact, data from the American Institute for Economic Research showed that when older workers were surveyed, 82 percent reported that they successfully changed to a new career after age 45. And then, there are the un-retirees.

This is also what makes retirementplanning so difficult – you effectively lose an asset in your portfolio when your income stops or declines. And this is why I’ve become such a big advocate of defining our durations within our financial plans. You’re temporally diversified by your income.

While an investor’s timeline affects their risk tolerance and allocation decisions between stocks and bonds, it’s important to remember how long a retirement time horizon can truly be. As economic conditions and income needs change, so too will your asset allocation. After all, investment management is an ongoing process.

During times of economic, financial, and political uncertainty, investors often wonder where to invest or what changes to make to their portfolio. Again, every recession or economic downturn is different. Swings in the financial markets also highlight the benefitsand limitationsof diversification. But history offers a helpful lens.

Introduction to GIFT City and Its Legal-Economic Status The Gujarat International Finance Tech-City, commonly referred to as GIFT City, is a landmark initiative by the Government of India aimed at creating a world-class financial centre within the country.

Consider topics like: “The Top 5 Retirement Mistakes I See Wealthy Professionals Make” “How Market Volatility Actually Affects Your Long-Term Goals” These videos position you as the expert while providing genuine value to viewers. Current events commentary also performs exceptionally well.

Additionally, we have news that FinCEN has announced an extension of the BOI reporting deadline and a temporary halt in enforcement, an analysis on the implications of wealth taxes in Europe, and a refresher on how the new ‘Savers Match’ program aimed at enhancing the retirement savings of millennials and Gen Z functions.

Unexpected events can derail your progress toward your goals and even your financial security if you don’t have a plan for managing them. Financial planning should ideally involve every area of your financial life because they are all interrelated. Plan for retirement. Maximize your use of tax-advantaged accounts.

Comprehensive Financial Planning is Included Many AUM advisors charge extra for estate planning, tax strategies, and retirementplanning. Ongoing Portfolio Monitoring AUM advisors continuously review your investments and adjust strategies based on market conditions and economic trends.

Recession-proof businesses are more than just smart, they’re essential when economic uncertainty hits. Content related to challenging financial times Final thoughts: Start building a recession-proof business today Recession-proof businesses can thrive despite an economic downturn. Should I start a business during a recession?

Or do you want to attract families who are planning for retirement? Share useful articles, tips, and advice about personal finance, investing, and planning for retirement. Are they interested in retirementplans? Create several posts that explain how to plan for a safe retirement.

Or are you focusing on older people who are concerned about estate planning for retirement or retirement income planning? Financial Goals: These include saving for retirement, managing money, and paying for education. Share economic signs and how they might affect your investment strategies.

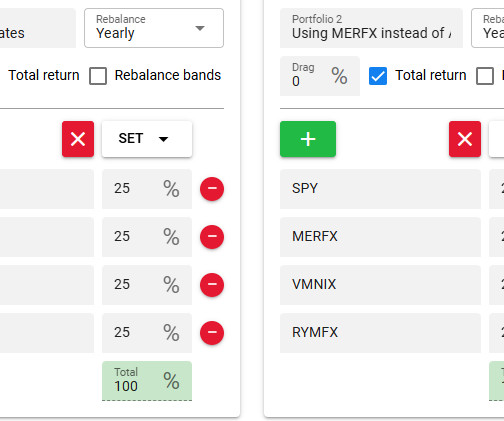

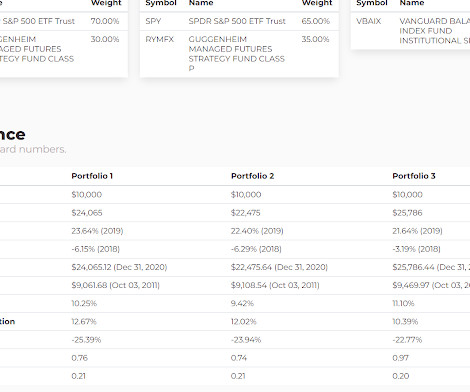

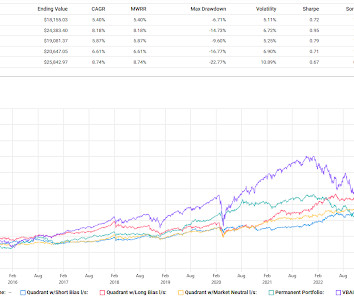

They talked about "four pillars" as being "economic growth (equities), income defensiveness (bonds), absolute return (alpha) and trend following (tail risk)." Research Affiliates (RA) threw its hat in this ring with a long writeup about managed futures. Portfolio 1 is an attempt to be true to the RA paper using AGG for bonds.

He tailors his approach to support long-term goals, whether it’s retirementplanning, saving for education, or managing major life transitions. Chad earned his degree in economics from San Diego State University before relocating to Florida to be closer to family and enjoy the outdoor lifestyle.

As someone deeply entrenched in financial planning and chronologically standing on the threshold of pre-retirement, the book was more than just a leisure read—it was a revelation. My reading list is usually dominated by stock market noise, economic reports, and client-related materials.

The Wall Street Journal looked at an issue near and dear to us by profiling four people who in middle age, had their hand forced into early or retirement or otherwise unexpectedly forced to find a new job. The first profile was a guy who was head of retirement research at Bank of America. I remembered to use the gift link.

Nate Geraci Tweeted out that "a ny sort of market, economic, or political turmoil offers a window into your financial advisor, portfolio manager, etc" Tough but fair. The S&P 500 was at 6000. If you can buy it at 4500, that is buying low, regardless of whether it goes to 4000 before going back up.

From the fund page : the goal is seeking stable returns across a variety of economic and financial market conditions, consistent with the preservation of capital. Offering diversified exposure to U.S. Treasuries, real estate, gold, and agricultural commodities."

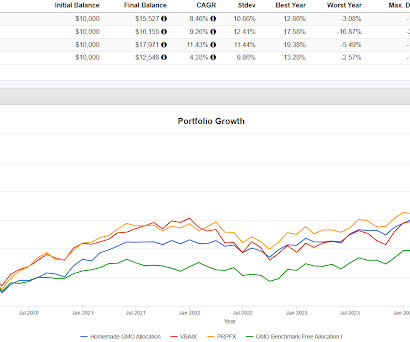

In addition to all the economic commentary, Jim manages the WisdomTree Bianco Total Return Fund (WTBN). It would be tough for me to put that much into Japan and 32% into MBXIX is fine for blogging purposes but I wouldn't even go 1/3 of that amount into any single macro strategy fund.

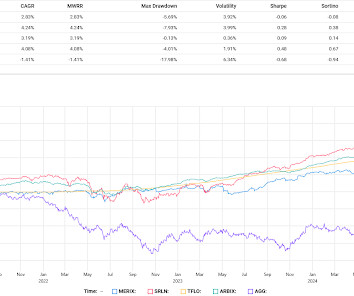

I excluded it for being a shock caused from outside the world of capital markets and economics. MERIX is a client and personal holding. My long time thesis of course has been that bonds no longer function as reliable diversifiers, they've instead become a source of unreliable volatility.

Economic uncertainty, shifting policies, and global events can make it difficult to know what comes next. You may be wondering how all of this impacts your financial future and the plans youve worked hard to build. With everything happening in the world right now, its natural to feel a bit unsettled.

spyglass.org) Alternatives Private equity keeps popping up in retirementplans. rogersplanning.blogspot.com) Retirementplan provider Empower will start including private markets investments in its defined contribution plans. (cnbc.com) The path to a successful IPO is longer than you think.

Last month we looked at Research Affiliates' take on quadrant style investing with allocations to equities for economic growth, bonds for income and defensiveness, absolute return for alpha and trend following for tail risk. In that last post we equal weighted a possible portfolio to express their idea.

In today’s economic environment, many individuals preparing for retirement are thinking more carefully about when to begin claiming Social Security benefits. While this trend highlights the need for thoughtful planning, the decision to take Social Security early is highly personal and depends on a variety of factors.

It reaffirms that life insurance should be the starting point of any secure financial plan—providing a strong foundation for long-term goals like children’s education, homeownership, and retirement. Addressing this challenge on a war footing is crucial to maintaining our society’s socio-economic resilience and security.

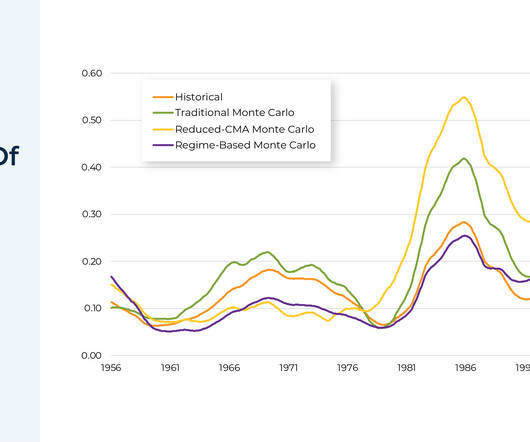

When planning for retirement, it’s effectively impossible to precisely forecast the performance and timing of future investment returns, which in turn makes it challenging to accurately predict a plan’s success or failure.

How much do I need for retirement?” Your financial needs in retirement can depend on dozens of factors – some known and some unknown. One or two million dollars may seem like a lot of money to have set aside for retirement. A Retirement Reality Check. The concept of retirement continues to evolve with the world around us.

Enjoy the current installment of "Weekend Reading For Financial Planners"– this week's edition kicks off with the news that a recent analysis from Morningstar suggests that the Department of Labor's (DoL's) new Retirement Security Rule (aka Fiduciary Rule 2.0)

After decades of saving and planning, many pre-retirees (non-retired investors aged 55-65) are reconsidering their retirementplans in response to rising inflation, high interest rates, and an uncertain economic environment. The biggest threat to a secure retirement?

In recent months, Americans are rethinking what life in retirement looks like because of economic uncertainty, opting to adjust their personal priorities with financial stability in mind. Working after retirement on the rise. Similarly, 41% want to continue working because it gives them a sense of purpose.

This month's edition kicks off with the news that held-away asset management platform Pontera has raised $60 million in venture capital funding as advisors increasingly seek to directly manage clients' 401(k) and other outside assets – although an ongoing investigation by Washington state regulators over whether advisors' use of Pontera violates (..)

The 2022 economic climate has been bumpy for most and, in some cases, even bumpier for retirees. Americans and the world at large dealt with the economic ramifications of the Russia-Ukraine war, post-pandemic industrial effects, and rising inflation and interest rates. Interest Rate Hikes Hit Retirement Accounts. 1] [link]. [2]

In 1974, Congress passed the Employee Retirement Income Security Act (ERISA) that, among many other provisions, provided for the implementation of the Individual Retirement Arrangement. Amounts rolled over from employer retirementplans are entirely exempt. billion in the first year (1975). billion by 1981.

The Five Phases of RetirementPlanning Published January 29, 2025 Reading Time: 2 minutes Written by: The Zoe Team Retirement is a journey with distinct phases, each requiring its own focus and preparation. The Transition Phase Approaching retirement brings the need for a shift in priorities. Ready to Grow Your Wealth?

Retirementplanning is an essential aspect of financial security, especially as one transitions from a phase of regular income to relying on savings and investments. The concept of retirement has undergone a significant transformation in recent times. Traditional retirementplans often rely heavily on pension schemes.

Our current economic situation is complex and, in some ways, unprecedented. Because of the pandemic, we have seen massive changes in how the market behaves, and we are having to readjust how we approach retirementplanning. Changes in the Global Economy For many years the world has been growing economically.

This phenomenon generally affects retirement funds as well – this is called the gender retirement gap. [1] 2] The gender pay gap has lasted throughout history, affecting global economic potential, and has cost the US an annual $1.6 trillion [3] in potential economic activity. Lower Retirement Income. Lower Savings.

As multiple recessionary signs flash red including bank failures, persistent inflation, and ongoing volatility, investors of all ages are increasingly nervous about the state of the markets and economy and what it means for their retirementplans and their ability to save for retirement.

Planning for retirement can seem premature when you have only been in the workforce for a decade or so. But as the oldest Millennials begin to hit middle age, retirement suddenly does not seem so far away. Here are five things Millennials should consider when planning for retirement. Free Money May Be Available.

Key Takeaways: According to a new Nationwide Retirement Institute® survey, the overall outlook on retirement for Americans has changed significantly since 2021, as roughly one in four employees feel they are on the wrong track for retirement and fewer than six in 10 have a positive outlook on their retirementplan and financial investments.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content