This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

One of the best tax deductions for a small business owner is funding a retirementplan. Beyond any tax deduction you are saving for your own retirement. You deserve a comfortable retirement. If you don’t plan for your own retirement who will? You need to start a retirementplan today.

The report suggests this might be due in part to increased RIA valuations and the assumption of some firm founders that next-generation employees won't be financially able to buy out the firm from them, though additional data indicates that many firms don't have career paths in place that could help next-generation advisors envision their path to firm (..)

Which could prove to be a boon for the financial advice industry as more consumers are willing to entrust their assets to an advisor (while at the same time possibly making it tougher for some advisors to differentiate themselves primarily by how they put their clients' interests first?).

Attorney’s Office said he failed to report the fraud proceeds on his personal income tax returns, which generated a tax loss of about $3 million. Today’s sentencing shows how seriously the courts take federal tax crimes.” "We and Mr. Mason respect and appreciate the court’s judgment yesterday," said Michael J.

Enjoy the current installment of "Weekend Reading For Financial Planners" - this week's edition kicks off with the news that SIFMA, which represents broker-dealers, investment banks, and asset managers, released a white paper that argues that CFP Board "increasingly functions as a de facto private regulator for CFP certificants" and proposes that CFP (..)

We’ve covered a lot of ground with regard to how various tax laws impact your retirementplans: pensions, IRAs, 403(b) and 401(k) plans. But we’ve primarily focused on the US income tax laws (the IRS) affect your plans – and there are many nuances that you need to take into account with regard to state tax laws.

Also in industry news this week: A recent survey indicates that younger "DIY" investors are more likely to be interested in working with a human advisor than their older counterparts, suggesting an opportunity for advisors to tap into this demographic (perhaps by setting minimum planning fees that ensure these clients can be served profitably today (..)

Like native-born workers, foreign workers need to think about saving for retirement, planning for their children’s college, managing healthcare costs, and all manner of other financial goals. For example, the tax benefits of certain accounts can sometimes work in the other direction if a non-U.S.-born

When you have the bulk of your financial assets in retirementplans, you might accidentally expose yourself to some risks that you haven’t thought about… since retirementplanassets are much more likely to be impacted by changes to legislation – as we have seen in the past. No related posts.

Seth is the founder of Heartwood Financial Planning, an advisory firm affiliated with PlanMember Securities Corporation that is based in Fresno, California, and oversees approximately $100 million in assets under management for 850 client households.

Many of us are covered by one or more types of defined contribution retirementplans, such as a 401(k), 403(b), 457, or any of a number of other plans. What many of these plans have in common is that they are referred to as Cash Or Deferred Arrangements (CODA), as designated by the IRS. How, you might ask?

Having a retirementplanning checklist can help make this final commute the time of reflection and joy it should be. While you simply cant plan for everything, having the essentials in place can give you the confidence and clarity you need to enjoy the freedom retirement can provide.

Unlike most types of retirementplans, the SEP IRA is funded by the employer. Here’s more on what a SEP IRA is, tax benefits, contribution limits, and important deadlines. The SEP IRA is a straightforward and cost-effective way for small business owners to save for retirement. What is a SEP IRA?

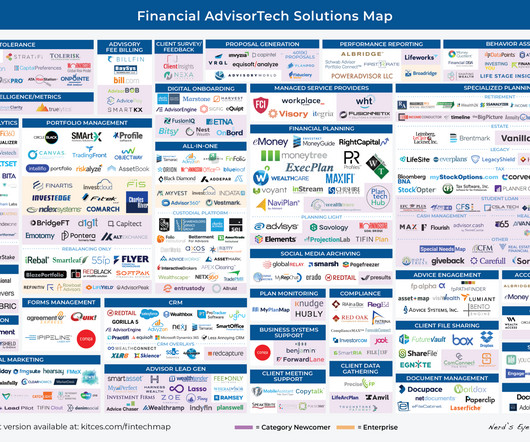

The survey also suggests that a firm's tech stack can affect its ability to attract and retain clients, with 93% of advisors who said they work with state-of-the-art technology reporting that they have added new clients as a result of another firm's bad technology, and 58% of all advisors surveyed reporting they had lost new business due to bad technology. (..)

This guide consolidates what we’ve learned to help you refine, update, or pressure-test your current retirement and estate strategy with confidence. Getting Started: What First-Time Planners Should Know Even for seasoned investors, key decisions around taxes, estate structure, and long-term income planning can carry significant implications.

Tax deductions can save you thousands annually by reducing your taxable income through legitimate business expenses. Understanding these deductions is more critical than ever as tax laws evolve, presenting new opportunities for savings. Understanding this distinction is crucial for maximizing your tax benefits effectively.

Without proper planning, taxes can unexpectedly take a large bite out of the proceeds, potentially reducing financial security and the legacy. When you understand various exit strategies and their tax implications early, you position yourself to make informed decisions that maximize after-tax value while ensuring a smooth transition.

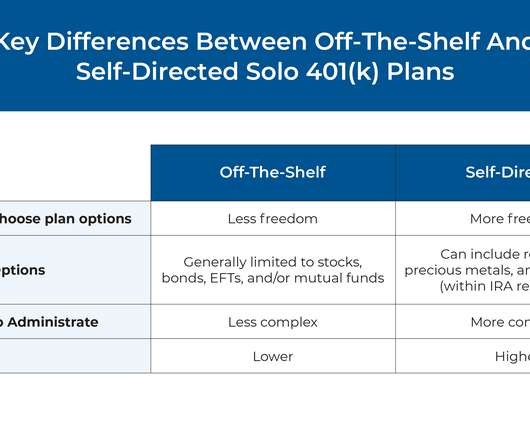

Among the several different types of retirementplans that are available to self-employed workers, solo 401(k) plans can offer the most flexibility and the ability to contribute the highest amount of tax-advantaged savings.

Retirementplanning is a critical part of financial security that many women still overlook. However, remember that as a woman, you have a longer life expectancy than a man, which means retirementplanning is even more important. Consider early retirementtaxplanning. Educate yourself about finances.

The post Tax Strategies for High-Income Earners 2025 appeared first on Yardley Wealth Management, LLC. Tax Strategies for High-Income Earners in 2025. In this comprehensive guide, we’ll explore proven strategies to help you minimize tax liability while staying compliant with current regulations.

This month's edition kicks off with the news that robo-advisor Betterment entered into a $9M settlement with the SEC for misrepresenting its tax-loss harvesting practices in its client agreements and marketing materials compared with its actual practices (e.g.,

This month's edition kicks off with the news that digital estate planning platform Wealth.com has raised a whopping $30 million in Series A funding, following on the heels of Vanilla's follow-on $20M capital round just a few months ago – which on the one hand reflects the anticipated enthusiasm for solutions that can help advisors efficiently (..)

As a result, financial advisors should start honing the services Gen X members will likely benefit from the most, including retirementplanning, estate and taxplanning and mortgage refinancing. Gen X, or those currently aged between 45 and 60 years, will receive nearly $13.9 trillion annually.

A recent study shows that while many consumers have expressed an interest in ESG investing, such funds within retirementplans have received limited allocations from investors. A survey showing how millionaires allocate their assets and the importance they place on the recommendations of their financial advisors.

Freelancers and contractors may enjoy greater flexibility and independence than full-time employees, however, this autonomy brings increased tax responsibility. Unlike W-2 employees, freelancers and independent contractors are responsible for managing their own tax obligations, which can be a complex process.

April 15 marks the IRS tax return filing deadline for 2025. Although this is the traditional tax filing deadline, given the spate of recent natural disasters (such as the California wildfires and Hurricane Milton), the IRS is granting certain filing and payment extensions beyond this date.

It’s held jointly between you and your employer and contains contributions from you both, and it consists of stocks, bonds, mutual funds, and other assets. The contents of a 401(k) are not taxed until they are withdrawn and taken directly out of your paycheck, which may be useful depending on your financial situation.

While a Roth conversion may never make sense for some individuals, for others, early retirement years may be the best time to convert pre-tax accounts to tax-free Roth. Your current and projected future tax rate is often a main component of the decision, but there are other considerations and benefits as well.

often fail to consider sequence of return, housing, longevity, health or family risks faced in retirement. Focus on Your RetirementPlan Rather Than a Magic Number. would be “How do I plan for retirement?“ Consider breaking assets into three columns: cash, investment assets and personal property.

Notably, this decision has provided both qualitative and quantitative benefits for these advisors, as 85% said they now have more control over their future and 80% saw their assets under management subsequently grow, with a median increase of 42%.

Barron's had a very quick look at the recent popularity of private assets to try to figure out whether investors should wade into the space. Another snippet from Barron's was the suggestion from Thad Davis of Aureus Asset Management to allocate 7% of a portfolio to private credit to get a 7% spread over SOFR which works out to 11-12%.

Andy is the owner of Tenon Financial, a virtual independent RIA that oversees $70 million in assets under management for 43 retired client households. Welcome back to the 297th episode of the Financial Advisor Success Podcast ! My guest on today's podcast is Andy Panko. Read More.

I've talked about my asset allocation before being overwhelmingly in cash or cash proxies, about 25% in "normal" equity investments, my exposure to crypto these days might be 2-3% up from 1/2 of a percent from when I bought Bitcoin in late 2018 but down from 6-7% when Bitcoin was higher.

It is March…that means you have just about 5 weeks left to get organized and submit your tax return. The tax deadline is April 18, 2023 (some taxpayers in disaster areas in California, Georgia and Alabama have an extended deadline). Gathering all your documents is crucial to complete a tax return free of mistakes.

In November 2022, proponents of the Massachusetts ‘millionaires’ tax (question 1) won their bid to nearly double the income tax rate on individuals with taxable income over $1M a year. As proposed, the new legislation would increase these tax rates to 9% and perhaps even 16% , respectively, starting in 2023.

So historically, every $1 million invested would yield annual dividend income of $19,800 on average… before tax. If you own 10,000 shares, you receive $40,000 in dividend income (before taxes) and have a portfolio currently worth $2M. Over the last 30 years, the S&P 500’s average dividend yield was 1.98%.

Selecting the right plan depends on individual medication needs, and advisors conduct cost-benefit analyses to reduce out-of-pocket spending. For individuals enrolled in a high-deductible health plan (HDHP), an HSA offers a structured way to build a healthcare reserve that grows with age and changing needs.

equity valuations: “Baby-boomers’ huge flow of 401K plan contributions helped to drive equities higher; now that ~70 million Boomers are retiring, when do demographics flip this from a huge positive to a net drag?” This demographic cohort is simply not a seller due to retirement – the tax expenses would be too great.

RetirementPlanning: Looking Beyond the Basics For 2025, it’s essential to think beyond the standard “maximize your 401(k)” advice. While that remains important, consider diversifying your retirement strategy. While that remains important, consider diversifying your retirement strategy.

Unexpected events can derail your progress toward your goals and even your financial security if you don’t have a plan for managing them. Financial planning should ideally involve every area of your financial life because they are all interrelated. Losses in one asset class may be balanced out by gains in another.

That must mean it’s time to roll up my sleeves and get to work on year-end financial planning – with an emphasis on 2023 income tax. One consideration this year is that we’re two years from the expiration of the Tax Cuts and Jobs Act of 2017 (TJCA). AGI impacts multiple other tax considerations.

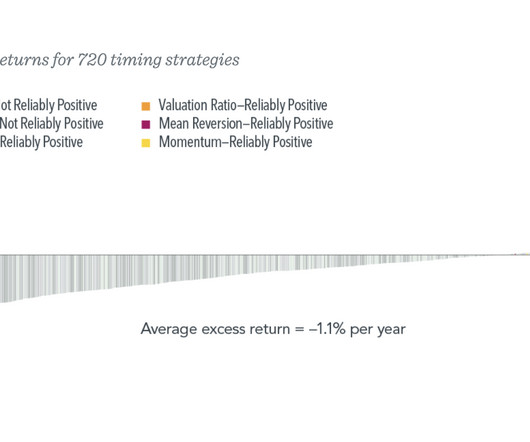

This is before we get to the issue of capital gains taxes, which create a hurdle of (minimum) 20% on those pesky profits just to get to breakeven. Low Stakes : The most successful market timers are often those people who do not have actual assets at risk. When you get it wrong, it crushes your retirementplans.

The 2017 Tax Cuts and Jobs Act (TCJA) brought sweeping changes to the tax code, impacting every taxpayer and business owner. Here’s a summary of the major tax law changes coming in 2026 and some steps individuals and business owners can take to prepare. For some, this may lead to more taxes paid on capital gains.

Roth IRA conversions present a significant challenge for retirement planners: pay taxes now or later? Moving funds from traditional IRAs to Roth accounts triggers immediate taxation but promises tax-free withdrawals in retirement. One of the Roth IRA’s most compelling features?

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content