This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Mike McGlothlin , CFP, CLU, ChFC, LUTCF, NSSA, Executive Vice President, Retirement, at Ash Brokerage , is the 2024 recipient of the Kenneth Black Jr. McGlothlin served on the Society of FSP National Executive Committee from 2018 to 2021 and was National President in 2020-2021. Leadership Award.

Be sure to check out our Masters in Business next week with Dominique Mielle, (retired) partner at Canyon Capital, a $25 billion hedge fund where she worked there for 20+ years. The book is a fun romp covering the 1998-2018 era. The post MiB: Cliff Asness, AQR appeared first on The Big Picture.

Focus went public in 2018, and then private again in 2023 , when it sold to Clayton, Dubilier and Rice, and Stone Point Capital.) Dixon-James launched Resilient Wealth Management in 2020 and now manages about $250 million in advisory, brokerage and retirement plan assets. His team was previously with Osaic for 12 years.

Also in industry news this week: Most businesses that operate in the U.S., Also in industry news this week: Most businesses that operate in the U.S., Also in industry news this week: Most businesses that operate in the U.S.,

In 1974, Congress passed the Employee Retirement Income Security Act (ERISA) that, among many other provisions, provided for the implementation of the Individual Retirement Arrangement. Amounts rolled over from employer retirement plans are entirely exempt. This IRA history is updated occasionally as new provisions are added.

When putting away for retirement, we often dream about all the things we’ll be able to do with that money – traveling, going out to eat, maybe trying new hobbies. . Of course, there are always the everyday household expenses to account for in your post-retirement budget. Ways to Start Planning Early for Retirement Health Care Costs.

Estate Planning Legal Battle Over the Control of Jimmy Buffett’s $275M Estate Heats Up Legal Battle Over Jimmy Buffett’s $275M Estate Heats Up Jun 18, 2025 Sign Up for Newsletters Sign up to receive the latest insights, trends, and analysis.

At 50 though, you do need to have some context for how viable your idea of retirement is. My reasoning is as it has always been, my income is levered to the ups and downs of the stock market, I don't ever want to retire, we have been living below our means for ages and now all the more so having just paid off our mortgage.

2000-13 : Secular bear market did not make new highs until March 2013 2018 : ~20% pullback as the economy slowed, FOMC hiked. By then, we began to have meaningful assets in our savings/retirement accounts and the bear markets had a bigger economic impact on those finances.

Roth IRA conversions present a significant challenge for retirement planners: pay taxes now or later? Moving funds from traditional IRAs to Roth accounts triggers immediate taxation but promises tax-free withdrawals in retirement. This flexibility becomes increasingly valuable as your retirement portfolio grows more complex.

NOW 2018 | Closing the Gender Wealth Gap achen Thu, 05/31/2018 - 11:51 The typical woman who works full time earns 79 cents for every dollar earned by a typical man. We hear this income statistic a lot. It’s disheartening, more so when you learn that the disparity is even worse along racial lines.

NOW 2018 | Closing the Gender Wealth Gap. Thu, 05/31/2018 - 11:51. Other solutions are often more obvious, such as programs that offer financial coaching on budgeting, saving for a down payment on a house, saving for retirement and other aspects of financial planning. We hear this income statistic a lot.

Construction Physics ) • When Your Career, and Retirement, Are the Family’s Business : Succession plans, or the lack thereof, can hinder the transition to a new generation — and affect how loved ones fund their later years. ( The book is a fun romp covering the 1998-2018 era.

NOW 2018 | Engaging the Next Generation in Public Service achen Wed, 05/30/2018 - 15:15 Our NOW 2018 conference dealt with a variety of forces that are tearing at the fabric of society, from social inequities, to political strife, to technological disruption. Rye Barcott, a retired U.S. He sees U.S.

NOW 2018 | Engaging the Next Generation in Public Service. Wed, 05/30/2018 - 15:15. Our NOW 2018 conference dealt with a variety of forces that are tearing at the fabric of society, from social inequities, to political strife, to technological disruption. Rye Barcott, a retired U.S. He sees U.S.

” This is backed by a 2018 study outlined in the Harvard Business Review that revealed CEOs work on average 9.7 Suddenly, they realize the clock is ticking and retirement may be in less than 10 years. By Jaslyn Ng If there is one word to describe CEOs, it would be the word “busy.” hours per weekday and 62.5

In its annual Retirement Confidence Survey of current workers and retirees, the Employee Benefit Research Institute found that workers’ confidence in their ability to fund retirement fell by the largest extent since the financial crisis of 2008, to levels not seen since 2018.

Ray Dalio, multibillionaire and founder of Bridgewater Associates—the largest hedge fund in the world—retired in October of last year to great fanfare, with much lauding from his and his firm about the transition. In 2018, Bridgewater pledged to shift control of the firm from the founder (Dalio) to top employees. .

Salary and Cricket Income Though Sachin Tendulkar retired from every type of cricket in 2013, his income throughout his playing years was huge. He continues to get a pension from the government of India and the BCCI as a retired Rajya Sabha member even after retirement. Apollo Tyres: Brand ambassador appointed in 2018.

Key Takeaways: 2023 could be a really good year to fund a Roth account because of low tax rates and changes to how the standard deduction, tax brackets, and retirement account contribution limits are adjusted for inflation. Plus, you’ll be increasing your tax diversification for retirement. One option is to contribute to a Roth IRA.

In 2018, the brackets dropped to 10%, 12%, 22%, 24%, 32%, 35%, and 37%. Mortgage interest will once again be tax-deductible on larger loans As a result of the 2017 legislation, between 2018 and 2025, interest on new mortgages is only tax-deductible up to $750,000 of mortgage debt on a primary or second home.

INTU late Thursday beat Wall Street expectations for its fiscal second quarter and announced the retirement of its longtime chief financial officer. Chief Financial Officer Michelle Clatterbuck, who has held the role since 2018, plans to step down as CFO on July 31, Intuit said. Clatterbuck is retiring after 20 years with the company.

4] Even though the stock market may recover as the economy bounces back, the extent of recovery for these 60/40 portfolios is uncertain and may alter how you choose to spend or maintain investments in retirement. Sinking Bond Markets. In a 60/40 allocation, this negatively affects the whole portfolio. 1] [link]. [2] 2] [link]. [3]

Fully Utilize Tax-Advantaged Retirement and Savings Accounts There are multiple steps you can take using retirement accounts to reduce your taxable income. Contribute to Tax-Advantaged Retirement Accounts Do your best to fully contribute to one or multiple tax-advantaged retirement accounts, such as 401(k), 403(b), or IRAs.

Khabib Nurmagomedov – $40 Million Khabib retired undefeated at 29-0. He was one of the UFC’s biggest draws, especially after his huge fight with McGregor in 2018. After retirement, he launched his own MMA promotion, Eagle FC, and invests in businesses in Russia and the Middle East.

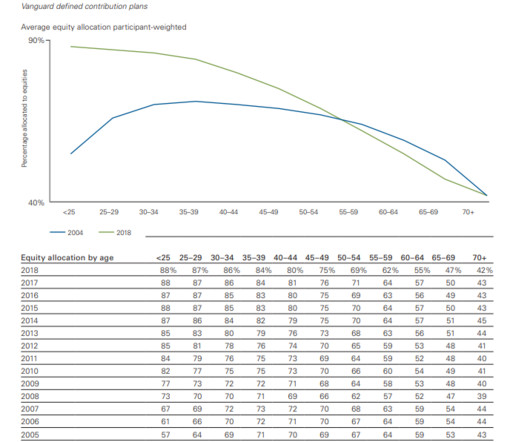

In 2018, 52% of all participants at Vanguard were invested in a single target-date fund. In 2018, two out of three new participants were in plans that adopted automatic enrollment. Six in ten people making more than $150,000 contributed the maximum account in 2018. That number fell to 19% in 2018.

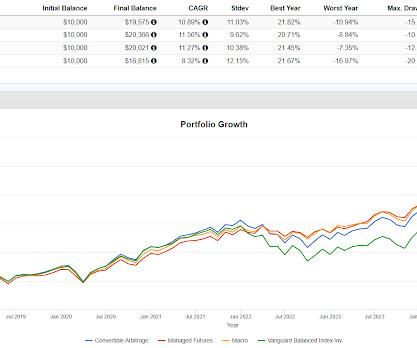

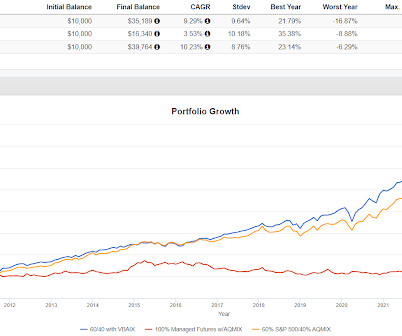

In 2018 you can see that two of them helped with just a few basis points. A year like 2018 constitutes down a little and is probably less important than protecting against down a lot like in 2022. In terms of crisis alpha in rough times, convertible arb didn't really help in 2022 but managed futures and macro did.

Someone retiring on Dec 31, 2021 being all in on traditional 60/40 had a real problem from an adverse sequence of returns. Someone retiring on Dec 31, 2021 with one of the managed futures-heavy portfolios had no such problem. It only back tests to 2018 but here's what you get. 90/40 was down 1.56% and Portfolio 3 was up 3.25%.

The 1987 crash was partly attributed to selling portfolio insurance and there was the so called Volmageddon of 2018. 2018 was not 1987 and if there is another event where volatility ends up being a major determent then it will be different than the other two but with some overlap. Events don't repeat but the can rhyme.

It's growth rate since inception is 3.58% going back to September, 2018 but a lot of that comes from a 15% lift in 2021 (numbers per testfol.io). RPAR is indexed and I think that fund's result shows that risk parity doesn't lend itself to an indexed approach. TRTY is a tough hold.

CAPE Fear: Why CAPE Naysayers Are Wrong As Dow Tops 25,000, Individual Investors Sit Out Bracing Yourself For a Possible Melt Up Bubbles for Fama Is Saving 10% Enough For Retirement? 10 Things Investors Can Expect in 2018 How We Got to Now is one of the best books I've read in a while. Past is Not Prologue Thanks for listening!

I think that is attributable to a terrible year for 100/100 in 2018. Terrible year in 2018 or 2022? 2018 was still lousy and 2022 was very good. I am more open to RSST as a core position than I was but 2018 is a good example of how it can go poorly. Notice though that the standard deviation for 100/100 is much higher.

Do you even remember why stocks crashed in late 2018? There will be future events that result in some sort of drop, black swans to you or not, and these become more important as you get closer to retiring in terms of sequence of return risk. Any retirement plan runs the risk of coming up short for any number of reasons.

I was “The Man Who Retired at 30”, and it was so unusual that it would show up in news headlines all over the place. My story was a nine-year working career, and retirement at 30. So at the end of year one, Curelop’s portfolio looked like this: 2018: Bought a second house for $343,000 ($27k down including some upgrades).

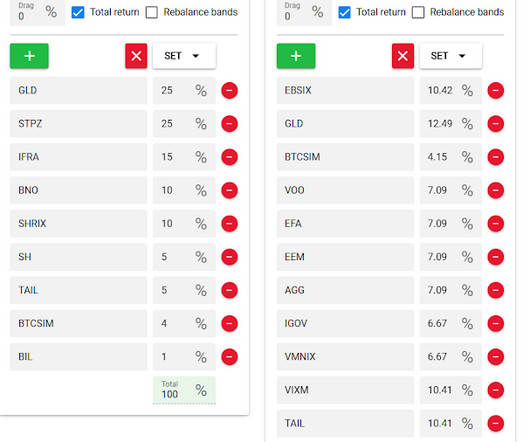

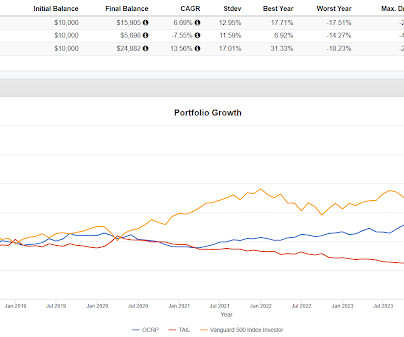

In late 2018 OCRP moved up when the market had a fast drop. OCRP will have 50% in CBOE Holdings (CBOE) and 50% in AGFiQ US Market Neutral Anti Beta ETF (BTAL) which are both client and personal holdings. If they can have single stock ETFs why not an ETF with just two holdings? I threw tail in as well as the S&P 500.

Picture retiring in 2010 versus 2020. As we say all the time, whereas stocks are the thing that goes up the most, most of the time in the modern era I would want more than 25% in equities for anyone needing normal stock market growth for their retirement plan to work. This is in the neighborhood of sequence of return.

Portfolio 3's worst year was 2018 when it fell 7.76%. Portfolio 2 had two years where it was down 5% (those were the worst two) and the leveraged version's worst year was 2018 when it fell 12.26%. The alts in the leverage sleeve all have a low to negative correlation to equities and to each other. BTAL is a client and personal holding.

Starting in 2018 causes the performance to change as follows. Both Portfolio 1 (Cockroach) and Portfolio 2 (the 3 fund mix I made up the other day) each have ways in which they are superior over the period studied from 2018 on. In 2017, as assembled, The Cockroach Portfolio went up 62% versus 21% for 100% SPY and 13% for VBAIX.

It offered no crisis alpha though in the 2020 Pandemic Crash and in 2018 it was down 13.5% There's kind of a mixed bag here for the results. In addition to what is shown above, in 2022 SYLD only dropped 6.12%. versus 4.5% If you're into Calmar Ratio and Excess Kurtosis, neither of those are particularly good for SYLD either.

It’s one of the best strategies to supercharge your retirement savings, especially for early retirement. There's no time like the present to begin preparing for your retirement. This is always true when neither you nor your spouse are covered by an employer-sponsored retirement plan. Ads by Money.

It's only down year was 2018 with a decline of 7.91%. These portfolios don't really look anything like what we usually play around with here but the results are interesting. Despite all the leverage, Portfolio 1 has a very smooth ride including up a lot in 2022. I'm not a fan of leverage but that doesn't mean it can't be used effectively.

Retirement funds had been demolished and there was very little hope. Near bear markets in 2011 and 2018, a 100-year pandemic bear market in 2020 and then another bear market in 2022 made it anything but an easy 15 years. For anyone who remembers that time, it was truly a frightening period in history. We had many scares along the way.

The momentum funds also did not provide early warning for the downturn in late 2018. When the stock market started falling in September 2018, QMOM provided no early warning like I said, but it fell much more into the December 24th, 2018 bottom, 31% vs 19% for the S&P 500 and 20% for MTUM. Here's the last year.

I added SH for clients a little while and have been holding BTAL for them and personally since 2018. Relative to a day or two, the timing was very lucky. BTAL and SH are clearly first responder defensives. Gold can be a first responder, it often is but it's not quite as reliable as BTAL and SH.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content