This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The firm has ~$100 billion in assets under management. The firm can go decades where they don’t talk about value (Post-GFC to 2017), because most everything else they do was working. This week, we speak with Cliff Asness , co-founder and managing partner at AQR Capital Management.

equity valuations: “Baby-boomers’ huge flow of 401K plan contributions helped to drive equities higher; now that ~70 million Boomers are retiring, when do demographics flip this from a huge positive to a net drag?” Can this one-two punch explain why it is so easy to get so much wrong in the capital markets so often ?

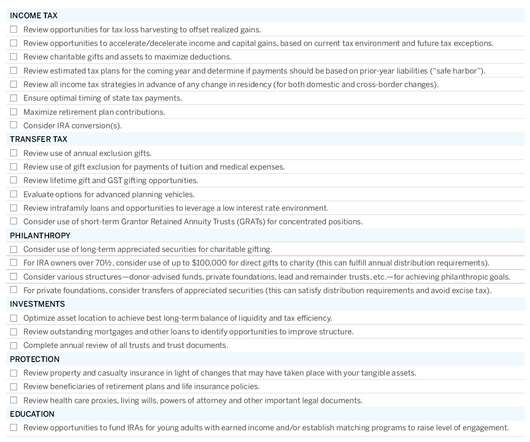

2017 Year-End Planning Letter. Mon, 12/04/2017 - 13:10. We are closing 2017 with nearly the same stance as last year. Spotlights for Prudent Planning in 2017. There have been very few changes to tax law in 2017, given that Congress has been focused on the longer-term tax reform effort. Since last year’s U.S.

He sold the company in 2017 or so for about seven and a half billion dollars. And but to be, to be clear, I sold Panera in 2017 and have not had anything to do with it since then. billion, literally in 2017. And I, I looked at her and I said, you know what, if I had any guts, I’d monetize every asset we have.

Key takeaways Tax planning impacts every facet of an acquisition, from initial valuation to post-closing integration, with early strategic decisions potentially saving millions in future tax liabilities. Asset deals In asset deals, purchase price allocation among asset categories is crucial, as each has its own tax implications.

Lakh Cr worth of Assets Under Management (AUM), which grew by 29% from the previous year. Assets Under Management (AUM) ₹2,47,379.00 Lakh Cr worth of Assets under Management (AUM), which grew by 36% from Rs. Chola’s Vehicle Finance business is its largest segment with assets worth Rs. The Company currently has about Rs.

Most valuation models start with the risk free alternative and with short term treasuries yielding well above 4%, the growth necessary to support high multiple growth stocks is just that much higher. From 2017 – 2021 growth outperformed value by a staggering 119%. Growth vs Value – There was no alternative. 60-40 is reborn.

IBM’s return was fueled by growing earnings, growing dividends, and buying back stock at cheap valuations. Even Buffett, whose BKB made the list, was about to buy (he bought into IBM in 2011, although the trade didn’t turn out well; he was out in 2017, having earned about 5 percent per year, including dividends).

Throughout 2017, our meetings and conversations with clients very frequently focused on the topic of risk. While February’s volatility did not materially change our asset allocation views, it reinforced to us the importance of a comprehensive discussion about how we think about risk and how we manage it. Fri, 03/30/2018 - 11:57.

But the drop in valuations experienced at year’s end, alongside higher bond yields, offer a foundation for better long-term return expectations across most asset classes. This is also a fitting moment to review the intersection of risk and valuation. This is also a fitting moment to review the intersection of risk and valuation.

The Company has over 6 years of experience in the execution of infrastructure projects since 2017. Under the Bharatmala Pariyojana plan, the Government approved Phase-I of the project in October 2017 with an aggregate length of 34,800 Km with an estimated outlay of Rs. The IRB InvIT was listed on the exchanges in June of 2017.

EUROPEAN RE-ENTRY: Why We Are Shifting Portfolios Toward European Stocks achen Thu, 06/01/2017 - 02:47 Asset allocation—at least for us—is an exercise in nuance. We move slowly and carefully when it comes to shifting our portfolios away from one asset class or region and toward another. is not particularly notable.

Thu, 06/01/2017 - 02:47. Asset allocation—at least for us—is an exercise in nuance. We move slowly and carefully when it comes to shifting our portfolios away from one asset class or region and toward another. stocks as of the end of 2015 on an EV/EBITDA basis; that gap widened to 20% by the end of April 2017.

Balancing Act | Pulling the FANGs Apart achen Thu, 12/14/2017 - 11:34 The “FANG” companies—Facebook, Amazon, Netflix and Google—have been a dominant investment story in recent years. All of these companies have generated attractive returns in recent years, and in 2017 in particular. Through Nov.

Thu, 12/14/2017 - 11:34. All of these companies have generated attractive returns in recent years, and in 2017 in particular. Their fear is bolstered by historical precedent: In the 1960s and 1970s, the “Nifty Fifty” ran up to extremely high valuations, and many performed quite poorly during the 1970s bear market. Through Nov.

Two weeks ago, I wrote an article where I looked at the valuation of the median stock and how it has changed over time. 12/29/2017 2.9% 12/29/2017 49.5% And with intangible assets rising in the economy, standard earnings calculations are becoming less and less accurate. By Jack Forehand, CFA, CFP® ( @practicalquant ) —.

This year, two factors will be important considerations in our year-end planning work: 1) current market dynamics (specifically, ongoing market volatility, low interest rates and a flat yield curve), and 2) the 2017 tax overhaul and our ongoing integration of new tax rules into clients’ long-term plans. Non-Taxable Gifts.

Investor enthusiasm, coupled with high valuations, has preceded all major market bubbles. He writes: The one reality that you can never change is that a higher-priced asset will produce a lower return than a lower-priced asset. stocks are based on traditional valuation metrics, via Michael Cembalest.

These planning opportunities are driven primarily by four factors: Materially lower market values for publicly traded securities, and a likely downturn in valuations of real estate and other illiquid assets. GIFT AND ESTATE TAX PLANNING Outright Gifting. Intra-family Note Refinance.

These planning opportunities are driven primarily by four factors: Materially lower market values for publicly traded securities, and a likely downturn in valuations of real estate and other illiquid assets. GIFT AND ESTATE TAX PLANNING. Outright Gifting. Intra-family Note Refinance.

Balancing Act | For Good Measure: How We Value Global Leaders achen Wed, 04/18/2018 - 11:03 Valuation is a critical component of active investment management, yet many investors restrict themselves to a very narrow view of valuation by focusing on simple metrics like the price/earnings (P/E) ratio.

Valuation is a critical component of active investment management, yet many investors restrict themselves to a very narrow view of valuation by focusing on simple metrics like the price/earnings (P/E) ratio. This makes ratios like the P/E ratio dangerous as a valuation tool. Wed, 04/18/2018 - 11:03.

Whether rates are rising or falling, we manage risk using the same consistent process: We look for bonds with attractive valuation relative to our view of their potential cash flows. For one, we reduced our exposure to shorter-duration fixed-rate municipals, as their valuations grew increasingly unattractive last year. (We

Whether rates are rising or falling, we manage risk using the same consistent process: We look for bonds with attractive valuation relative to our view of their potential cash flows. For one, we reduced our exposure to shorter-duration fixed-rate municipals, as their valuations grew increasingly unattractive last year. (We

We tend to be strategic rather than tactical in our approach to investing, but a combination of recent fundamental developments and valuation changes has caused us to add a note of caution in conversations with clients and in the management of their portfolios. Concentration: Much of the U.S.

We tend to be strategic rather than tactical in our approach to investing, but a combination of recent fundamental developments and valuation changes has caused us to add a note of caution in conversations with clients and in the management of their portfolios. Concentration: Much of the U.S. Risks in Bonds.

The ambiguity surrounding securities levels is sometimes a point of frustration for NFP staff, especially in the valuing of less liquid, harder-to-ascertain level 2 and 3 assets. Explain the timing difference and cutoff on valuations. To help efficiently support the leveling process, we recommend a four-step process: 1.

In this article, our head of asset allocation discusses how we are managing trade risk, while still embracing global growth opportunities in our portfolios. After an unnaturally serene 2017, volatility roared back into equity markets this year, fueled by worries over interest rates, inflation, tariffs and data privacy. From a U.S.

In this article, our head of asset allocation discusses how we are managing trade risk, while still embracing global growth opportunities in our portfolios. After an unnaturally serene 2017, volatility roared back into equity markets this year, fueled by worries over interest rates, inflation, tariffs and data privacy. From a U.S.

A Moment of Zen: The Wisdom of Staying Invested achen Wed, 07/19/2017 - 15:28 When discussing the merits of cash as an investment, Warren Buffett doesn’t pull his punches, saying that those who hold cash or its equivalents “have opted for a terrible long-term asset, one that pays virtually nothing and is certain to depreciate in value.”

Wed, 07/19/2017 - 15:28. When discussing the merits of cash as an investment, Warren Buffett doesn’t pull his punches, saying that those who hold cash or its equivalents “have opted for a terrible long-term asset, one that pays virtually nothing and is certain to depreciate in value.”. Valuations of the U.S.

Further, 2017 overall was extraordinary for its lack of market volatility; the S&P 500 Index rose steadily throughout the year without so much as a 3% pullback—a first in the Index’s long history. For most of 2017, the VIX was exceptionally depressed, signaling that investors expected very little volatility in prices.

Further, 2017 overall was extraordinary for its lack of market volatility; the S&P 500 Index rose steadily throughout the year without so much as a 3% pullback—a first in the Index’s long history. For most of 2017, the VIX was exceptionally depressed, signaling that investors expected very little volatility in prices.

Balancing Act | A New Publication Series achen Tue, 11/28/2017 - 13:39 We believe that investing in equities should be a balancing act, not an exercise in placing bets on one side of the market. It should not be assumed that investments in such securities or asset classes have been or will be profitable.

Tue, 11/28/2017 - 13:39. We will hear equity research analysts talk about risk and opportunity within the sectors they cover, and portfolio managers discuss the dangers of relying too heavily on traditional valuation metrics. It should not be assumed that investments in such securities or asset classes have been or will be profitable.

Any asset subject to such sharp swings may be catnip for traders but of limited value either as a reliable medium of exchange (to replace cash) or as a risk-reducing or inflation-hedging asset in a diversified portfolio (to replace bonds). Gox Bitcoin Customers Could Lose Again,” Reuters, November 16, 2017.

Where we differ, is that he allocates his "side" portfolio to one asset - Facebook. I try to highlight the dangers of being as concentrated in one asset as he is. They don't understand their setting as a marketplace where asset prices reflect and depend on the expectation of the participants. Consistently, and by a lot.

Thu, 08/24/2017 - 15:12. Contrary to the highly publicized booms and busts of some real estate segments, most private real estate investments offer many risk-mitigating benefits to investors, such as low correlation with core asset classes, long-term protection against inflation, income generation and—yes—low volatility over time.

The same process is used with bonds, real estate and other cash-generating assets. Assets that produce no cash (e.g. In addition to having a long history as a financial asset, gold has economic applications in electronics, medicine and jewellery. Catherine D. If history is a guide, it’s anyone’s guess.

The same process is used with bonds, real estate and other cash-generating assets. Assets that produce no cash (e.g. In addition to having a long history as a financial asset, gold has economic applications in electronics, medicine and jewellery. Catherine D. If history is a guide, it’s anyone’s guess.

While we can’t predict the near-term direction of the economy or of markets, there is no denying that safe haven assets are back in vogue, and investors have been voting with their dollars. Treasuries. intermediate and longer-term) allocation to U.S. Downside Protection From Fixed Income.

It makes sense to spread investments into different asset classes and different global regions to balance risk and reward. Then, after six years we regained a greater degree of optimism about Europe and began shifting assets back in that direction, as we noted in an article in 2017. Why Invest in Europe and Asia (Even as U.S.

It makes sense to spread investments into different asset classes and different global regions to balance risk and reward. Then, after six years we regained a greater degree of optimism about Europe and began shifting assets back in that direction, as we noted in an article in 2017. Why Invest in Europe and Asia (Even as U.S.

In this brief paper, we will touch on what we believe are some of the most important issues and questions—including the different types of assets, return potential, fees, liquidity, diversification, volatility and transparency—that investment committees must understand as they weigh adding alternatives to their portfolios. Source: BLOOMBERG.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content