This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

When you get it wrong, it crushes your retirement plans. My own track record at making big calls is pretty damned good, but none of our clients wants me slinging around their retirement monies based on my gut instinct. The dotcom top, the double bottom in Oct 02-March 03; the highs in 2007, the lows 2009.

For example during the 2008-2009 market debacle I looked at funds to see how they did in both the down market of 2008 and the up market of 2009. If a fund did worse than the majority of its peers in 2008 I would expect to see better than average performance in the up market of 2009. Markets will always correct at some point.

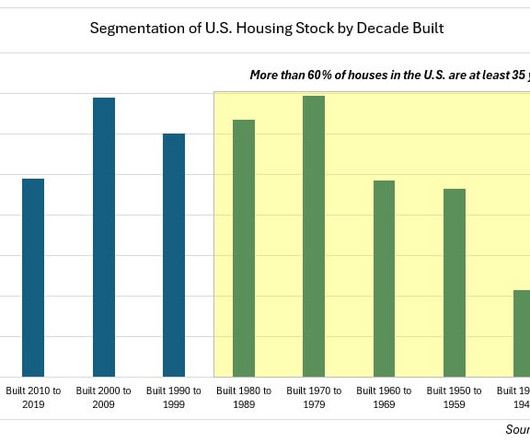

The housing bubble and subsequent bust that was largely responsible for the 2007 – 2009 financial crisis resulted in depressed housing starts for more than a decade; in fact, from 2008 through 2019, single family housing starts averaged just 660,000, not even 60% of the long-term average. averaged more than 1.1 million per year.

At its 2009 trough, SSO was down more than 80%. For as much as we explore using leverage and the concept of portable alpha, this post turned into a great example of how what appears to be a valid strategy (I do think it's valid) can get done in by an adverse sequence of returns, depending on how it's built.

I wasn't surprised to learn that 350,000 people have at least $1 million saved in a retirement account. I was surprised to learn that there are 350,000 retirement accounts at Fidelity alone. Fidelity just published their Q1 2019 retirement trends and there are some encouraging things going on.

The returns are normalized total returns of various bond indices during the 2008 -2009 financial crisis. When rates are low, corporations often retire high-cost debt in favor of issuing new bonds at a lower rate and a longer duration to lock in favorable rates. How do bonds perform during a recession?

You hear the word recession and might be reminded of the Great Recession from late 2007 to mid-2009. Also, do not forget that liquidating your investments early may come with penalties or tax consequences, especially if you are pulling from retirement accounts, such as the Individual Retirement Account (IRA) or the 401(k).

In its annual Retirement Confidence Survey of current workers and retirees, the Employee Benefit Research Institute found that workers’ confidence in their ability to fund retirement fell by the largest extent since the financial crisis of 2008, to levels not seen since 2018.

Ray Dalio, multibillionaire and founder of Bridgewater Associates—the largest hedge fund in the world—retired in October of last year to great fanfare, with much lauding from his and his firm about the transition. The post Bridgewater’s Dalio Gets Billions To Retire appeared first on Validea's Guru Investor Blog.

That’s one reason why the 2008–2009 recession was as bad as it was—households were much more levered and when unemployment rose and home prices fell, everything crashed. The greater the leverage, the harder the crash (like in 2008-2009). It was 101% at the end of 2019, and 137% just before the financial crisis in 2007.

The Satyam scam (Satyam computers scam) was finally exposed early in 2009. As the investors were still coping up with the failed acquisition of Maytas and the allegations by the World Bank on January 7th, 2009 the markets received the resignation by Mr Raju and along with it a confession that he had manipulated accounts of Rs.

If you're inclined to read the SeekingAlpha post, it is from 2009, you might find some interesting things. There are a few points made that pretty much are exactly what we talk about today but then I think it is possible to read where some other ideas have evolved, I would say slowly, since then.

Most of us of course lived through that from 2000 through to 2009. It then had a huge snap back year in 2009. The returns are not unprecedented, the 1990's were similar as one example but then when it ends, the "backside of the mountain" as Meb put it can be pretty rough.

Listeners think to 2009, the bottom, at the bottom, um, stocks have almost been a 10 bagger. And you’re going to see a big sea change in the next three to five years of asset managers and RIAs optimizing taxable tax, and then non-taxable retirement accounts for various type of investments. And that’s the broad market.

When you get close to retirement, you know what will matter? What will matter is whether you have enough to retire to the lifestyle you want plus maybe having some sort of margin for error in your accumulated savings. Sure, I'm $200,000 short of my goal but you know what, I beat the market five years in a row from 2009-2013."

We had a lost decade from 2000-2009 but there were several years that stocks went up kind of lot. In 2022, that blend was down 89 basis points so some drag (PRPFX did worse than BLNDX that year) but not problematic. Portfolio 3 is sort of close to what we blog about regularly.

From March 9, 2009 through December 31, 2019 equities were up more than 498% and bonds returned 54% while cash alternatives realized little return. We think over the next several years fixed income investors should anticipate a return that is near or slightly below the longer term historical average fixed income return.

Hedge fund fees fall to record low How to Launch and Build an Investment Fund The prophet returns (2009, video) Investing in personal-injury lawsuits Monetizing poor people But maybe payday loans aren't so evil Finally, a bad guy goes to jail Actually, 10,000 boomers are retiring every day Sustaining wealth is basically impossible.Especially across (..)

00:08:57 [Speaker Changed] Well, in 2003, ING acquired Aetna’s financial businesses, and that was the life insurance, retirement and asset management businesses. And, and my boss became head of ING Americas all of the insurance, retirement, and life businesses. 00:14:50 [Speaker Changed] Yeah, it was about the middle of 2009.

National Financial Awareness Day can be a great time to check in with your clients and discuss credit card debt, check their credit score to make sure they’re where they want to be, help ensure they’re on track for retirement, and so much more. Although 53% isn’t ideal, this number shows improvement from 35% in 2009. Budgeting.

this year so far, with the country’s biggest fund—the California Public Employees’ Retirement System (CALPERS) reporting a loss of 6.1%, its worst since 2009. Stock and bond losses are leaving state and local pensions with only enough to cover 77.9% Public funds have seen losses of about 10.4%

For a little context, from the S&P 500's peak in October 2007 to the low in March 2009 when the index dropped 55%, VBAIX was down 37%. The 4% rule is of course the most basic, most elementary rule of thumb for sustainable withdrawals in retirement. this year versus down 24.8% for the S&P 500. The 4% rule was based on this too.

In a Bloomberg column published before Thursday’s data, Dudley, head of the New York Fed from 2009-2018, said there are many reasons to expect the 10-year yield BX:TMUBMUSD10Y to move “considerably higher” than its narrow range near 3.75%. regional banks. s “troubling” fiscal trajectory, among other things.A

Retirement Planner You can often find retirement planners or retirement calculators on various sites throughout the Internet. Personal Capital’s Retirement Planner allows you to run numbers on your retirement to make sure that you will be prepared when the time comes. Is Personal Capital for Me?

Outside of a retirement account, I see nothing wrong with holding six months of living expenses or something like this. Inside a retirement account, I can't think of a good reason why 9% of your portfolio should be earning next to nothing. There is way too much of it. That number fell to 19% in 2018. I think this is fantastic.

Articles The latest embarrassment for a former star who has not bested the stock market since 2009. By Barry Ritholtz Your life is not a retirement calculator. By Ben Inker Choice is great, within reason. By Josh Brown In some respects, it has never been more difficult to be an investor.

Even more impressive is the past four times this happened (1997, 2003, 2009, and 2020) all saw at least double-digit returns. An aging population, with more people retiring and leaving the labor force every day, can also make the numbers noisier. MAY”be we have a positive signal from the strong May. Did you see what I did there?

The S&P 500 fell an eventual 57% from its October 2007 peak before bottoming on March 9, 2009, and finally ending the global financial crisis (GFC) bear market. Retirement funds had been demolished and there was very little hope. For anyone who remembers that time, it was truly a frightening period in history.

Not exactly weak (the hiring rate collapsed below 3% during the 2008-2009 recession), but not too hot either. That is why there’s really no such thing as a mild recession — the three recessions prior to the pandemic recession (1991, 2001, 2008-2009) were all bad from an employment perspective, as it took years for the labor market to recover.

There is tradeoff to being down less which is being up less in years like 2009 and 2023. A smoother ride hopefully reduces the odds of panicking when the market goes down a lot with the idea being that a portfolio constructed to have less volatility than the broad market will probably be down a lot less during years like 2008 or 2022.

In 2000, BPLSX outperformed by 69%, in 2001 it outperformed by 37%, 22% in 2002 and 46% in 2009. I outlined the four years that account for just about all of the long term outperformance. For the last ten years, BPLSX's CAGR is a little more than half of the S&P 500.

Even Mr. Money Mustache, as a person who retired 17 years ago, is still in this boat for the simple reason that my retirement income from dividends and hobby businesses is still greater than my annual living expenses (which still hover around $20,000 per year). (It’s the current blowup) -20% so far What’s your guess?

Running the same study from 2009 to 2021 avoiding those two bad years shows a different result. That worst year column is noteworthy, those numbers come from 2008. 2022 was a similar story with Portfolio 1 down 11.70% versus a drop of 16.87% for VBAIX. VBAIX has a better CAGR with a lower standard deviation.

A recent survey from the Nationwide Retirement Institute® uncovered topics business owners are looking to discuss including economic pressures and business-specific challenges such as access to capital, the tight labor market, employee benefits, and supply chain disruptions. Many are actively seeking the guidance of a financial professional.

The funds did well in the Financial Crisis and they did well in 2022 but from 2009 onward, one of his two long standing funds has a negative annual growth rate and the one with a positive growth rate was less than 1/3 of a plain vanilla 60/40 portfolio.

Retirement plan sponsors. We are currently experiencing one of the most volatile times in decades, on top of the start of the pandemic and the 2008-2009 recession. Investments and economy. OCIO/Investment outsourcing. Nonprofits and healthcare organizations. Institutional (US).

Consider the investor who started buying stocks in early 2009, effectively the bottom of the market in the Great Financial Crisis where stocks enjoyed one of the longest bull markets in history. Did you invest with a clear purpose in mind, such as retirement, buying a home, or funding your children’s education?

The past 10 years were a great market for stock buyers, lousy for newly retired boomers. They were also rough for the retiring class of 2008. At the lows in 2009, the S&P 500 was back to where it was in 1996! According to a 2019 survey from TD Ameritrade , 38% of people ages 60-69 have less than 100k save for retirement.

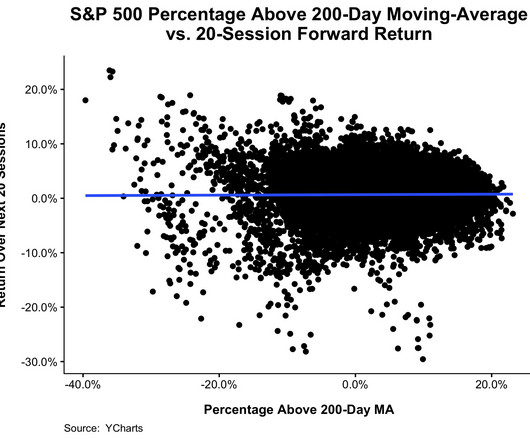

By September 2009, the S&P 500 was 20% above its 200-day moving average even as it was sat 32% below all-time highs. What I absolutely am saying is that if you're saving investing for retirement, you shouldn't be making changes to a portfolio that you don't plan to use for another few decades based on feelings.

Retired or Limited Hermes Constance bag sizes. While the fashion Maison is still manufacturing all the above Hermes Constance sizes, various limited editions have been retired or are created in limited quantities/editions. The Hermes Constance 23 is a retired model introduced in 2007 and discontinued in 2009.

By comparison, the 2008 Troubled Asset Relief Program (“TARP”) was $700 billion, and the subsequent American Recovery and Reinvestment Act (“ARRA”) of 2009 was $831 billion. Relaxation of Penalties on Early Retirement Account Withdrawals for Virus Related Hardship. Enhanced Charitable Deductions in 2020.

By comparison, the 2008 Troubled Asset Relief Program (“TARP”) was $700 billion, and the subsequent American Recovery and Reinvestment Act (“ARRA”) of 2009 was $831 billion. . Relaxation of Penalties on Early Retirement Account Withdrawals for Virus Related Hardship. Enhanced Charitable Deductions in 2020.

That data goes back to 2009. Neither has been close to ANNPX and so the concern is not being able to maintain such a wide lead against the convertible space. It didn't take long though to find a couple of funds I've never heard of that have similar return and volatility profiles. A few posts back we talked about tracking error.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content