This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Ideally you’ve been rebalancing your portfolio along the way and your assetallocation is largely in line with your plan and your risk tolerance. You should continue to monitor your portfolio and make these types of adjustments as needed. Assess whether your portfolio has held up in line with your expectations.

Sherman oversees and administers DoubleLine’s investment management subcommittee; serves as lead portfolio manager for multisector and derivative-based strategies; and is a member of the firm’s executive management and fixed-income assetallocation committees.

It has been my experience when reviewing portfolios that diversification is typically expressed simply as a number of various stocks owned, or owning a handful of asset classes, usually stocks of various sizes and geographies, and bonds of varying maturities.

Their focus is on generating alpha with high conviction concentrated portfolios. As you, as you may recall, the insurance companies had huge commercial loan portfolios in those days that they were using to backstop long dated life insurance liabilities. 00:14:50 [Speaker Changed] Yeah, it was about the middle of 2009.

If you have a taxable portfolio of at least $1 million where selling or rebalancing would hit very hard tax-wise, you can exchange your portfolio for shares in a 351 ETF. Based on Cambria's other multi-asset funds, ENDW will probably have fixed income duration but that's a space I will continue to avoid. The results.

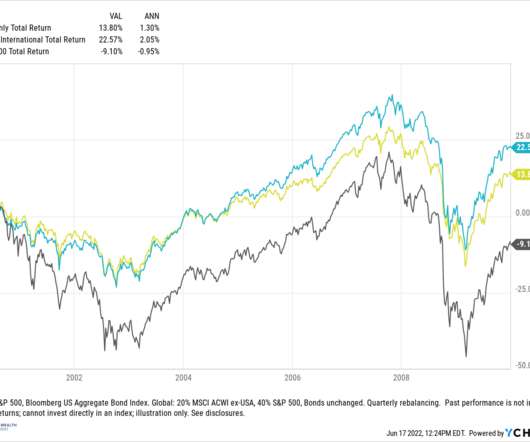

Between 2000 – 2009, the cumulative total return for the S&P 500 was negative 9.1% Since trying to time regime changes is very difficult in real time without the benefit of hindsight, there are reasons to consider allocating both U.S. equities to an assetallocation. These bouts can be significant. vs positive 30.7%

In this blog, I am going to give you insights on the important aspects of investment management employed by the best investors and how we can use them to maximize our portfolio returns besides minimizing the risk. Use tactical allocation to make your portfolio future-ready. Be Cautiously Optimistic.

At the time, those funds were having success because of Hussman's generally defensive portfolio posture. The funds might play a role in a diversified portfolio but hard to peg either one as a single portfolio solution. The idea of a single fund, all-weather portfolio is intellectually appealing even if it probably doesn't exist.

Meb Faber had a poll on Twitter that asked "how many years do you think you could withstand your portfolio underperforming the S&P 500?" Sure, I'm $200,000 short of my goal but you know what, I beat the market five years in a row from 2009-2013." It's a great question. That outperformance would be meaningless.

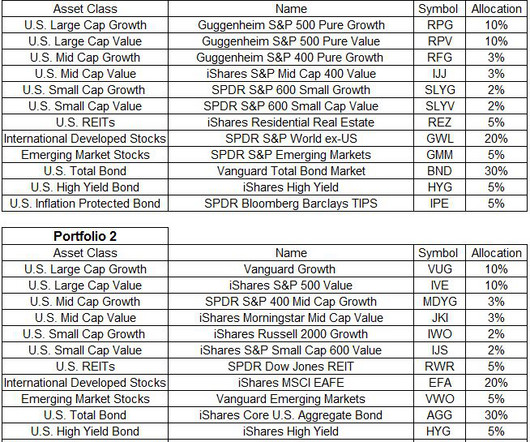

Below are two nearly identical portfolios; both are sixty percent stocks and forty percent bonds. Each portfolio has twelve slices, with identical allocations in each sleeve. For example, portfolio 1 has a 10% position to U.S. Portfolio 2 also has a 10% position to U.S. Portfolio 2 sold after the 23.3%

One thing that I have craved for investors is a tool that allows you to sync all your financial accounts – your investment portfolio, checking and savings accounts, credit cards and other loan accounts – in one place, and then provides an investment-related analysis of your entire portfolio.

With the wild swings in the stock and bond market this year, it's likely that your assetallocation has gotten a bit out of whack. For example, a portfolio that started the year 60/40 (U.S. A portfolio rebalance is simply the act of returning to your pre-determined assetallocation. stock.bond) is now 54/46.

The budget gap for nonprofits has widened because of a slump in their three sources of funds—donations, grants and portfolio returns. 1 Also, from fiscal year 2009 until fiscal year 2016, federal agencies cut annual grants to private and public organizations by 3.4% Consider changes to portfolio construction.

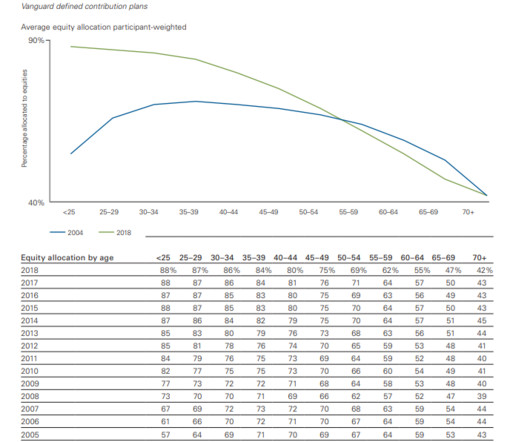

. ($18,500, $24,500 for people 50 or older) The chart below shows overall assetallocation in these plans. Inside a retirement account, I can't think of a good reason why 9% of your portfolio should be earning next to nothing. The biggest takeaway for me here is the cash number. There is way too much of it.

As with many things in life, the truth is somewhere between the extremes: While both simulated and real-world data suggest momentum may not be suitable as a driver of long-term assetallocations, we believe momentum considerations can be integrated in a cost-effective way to help inform daily portfolio management decisions.

We are currently experiencing one of the most volatile times in decades, on top of the start of the pandemic and the 2008-2009 recession. That’s why, when facing market volatility, stewards of long-term assets held at all types of nonprofit institutions recognize the importance of a well-thought-out investment process. .

In advising clients over the years, we have seen the value of helping families buy into the longterm orientation essential to successful investing and portfolio management through all market conditions. Determine both your annual level of spending and a five- and 10-year goal for portfolio returns.

If you’re at all interested in focused portfolios, the concept of quality as a sub-sector under value and just how you build a portfolio and a track record, that’s tough to beat. Dick Mayo was a traditional, I’d say portfolio, strong portfolio manager focused on US stocks. He’s a big picture guy.

However, the impending end of the Federal Reserve (Fed) rate-hiking campaign, and the economy’s and corporate America’s resilience, help make the bull case that steers LPL Research toward a neutral, rather than negative, equities view from a tactical assetallocation perspective. All index data from FactSet.

Hundreds of academic studies and thousands of media commentaries have taken different angles on this issue, with the conversation centered on one key question: Does the incorporation of ESG factors in portfolios help, hurt, or do nothing to returns? Can we also generate predictable utility from managing portfolios around an "ESG factor?"

Hundreds of academic studies and thousands of media commentaries have taken different angles on this issue, with the conversation centered on one key question: Does the incorporation of ESG factors in portfolios help, hurt, or do nothing to returns? Can we also generate predictable utility from managing portfolios around an "ESG factor?"

built up substantial reserve capital while recovering from the Great Recession in 2008-2009. By Taylor Graff, CFA, AssetAllocation Analyst. We are recommending that clients consider high-yield bonds and other asset classes that can offer the prospect of solid gains that diverge from the path of traditional stocks and bonds.

We found there were two times during the tech bubble that stocks gained 20% and again moved to new lows, and it also happened during the global financial crisis of 2007-2009. It was developed a decade ago and is a key input into our assetallocation decisions.

Almost exactly five years ago, we wrote a piece entitled Bubbles, which discussed the sharp rally in stocks from the lows of early 2009 and the risks of the growing federal deficit that resulted from government bail-outs and fiscal stimulus during the financial crisis. Simply stated, asset classes tended to move together: When U.S.

Instead, they’ve turned to indexing their portfolios to the S&P 500 ® Index or some other relevant benchmark, thereby accepting “average” performance rather than trying for something better. Portfolios with greater active share could be said to reflect more independent thinking on the part of the managers.

Instead, they’ve turned to indexing their portfolios to the S&P 500 ® Index or some other relevant benchmark, thereby accepting “average” performance rather than trying for something better. Portfolios with greater active share could be said to reflect more independent thinking on the part of the managers. Manager Characteristics.

From a longer-term perspective, stocks rose from 2009 until this recent correction with only a few setbacks along the way. increase in the average hourly wage rate, the fastest rise in that rate since 2009. (It Still, it’s incumbent upon us to position client portfolios to endure periods of volatility like the present one.

From a longer-term perspective, stocks rose from 2009 until this recent correction with only a few setbacks along the way. increase in the average hourly wage rate, the fastest rise in that rate since 2009. (It Still, it’s incumbent upon us to position client portfolios to endure periods of volatility like the present one.

As head of assetallocation research in our Investment Solutions Group, he is responsible for analyzing the relative attractiveness of various asset classes and investment strategies. Technology has also enabled analysts, portfolio managers and traders to improve their productivity.

As head of assetallocation research in our Investment Solutions Group, he is responsible for analyzing the relative attractiveness of various asset classes and investment strategies. Technology has also enabled analysts, portfolio managers and traders to improve their productivity.

Morgan began tracking this data in 2009. That is the highest level since quarterly data collection began in 2009. . By Stephen Shutz, CFA, Tax-Exempt Portfolio Manager. By Taylor Graff, CFA, AssetAllocation Analyst. The IMF in July downgraded its forecast for global growth this year to 3.3% Rude Awakening.

For the past year, we have been preparing client portfolios for the end of the extended bull market run that began in 2009—building cash and liquidity reserves, and also exploring opportunities in private and alternative asset classes that historically have offered lower correlation with public markets.

For the past year, we have been preparing client portfolios for the end of the extended bull market run that began in 2009—building cash and liquidity reserves, and also exploring opportunities in private and alternative asset classes that historically have offered lower correlation with public markets. MANAGING LIQUIDITY RISK.

With that preamble, I started thinking about the 75/50 portfolio that I first started writing about during the Financial Crisis. I've mentioned 75/50 a couple of times in passing but the big idea was to create a portfolio that captures 75% of the upside of the equity market with only 50% of the downside. ARBFX 3.7%

You would offer three of their stock picks where they were probably touting stocks they wanted to unload from their portfolio. 00:12:41 [Speaker Changed] If nothing in your portfolio is performing badly, you’re not diversified. And then on top of that, of course we ran straight into the 2008, 2009 great recession.

I recall one particularly glaring moment during 2009 when AIG became mostly owned by the US government and failed to meet S&P liquidity requirements, but they just ignored it. It forced me to think in a multi-temporal sense which has completely changed how I think about assetallocation.

So a very different dynamic than we saw back in 2007, 2008, 2009. So when you think about the individual exposure to a specific name, in our funds, it represents less than one half of 1 percent of the portfolio. And I think that what our investors saw is that, number one, our portfolio held up incredibly well. RITHOLTZ: Right.

President Obama’s term, starting in 2009, began when stock market valuations were near the bottom and as is well documented now, the stock market went on to its longest bull market in history. For example, the September 11th terrorist attacks and the 2008 Great Financial Crisis occurred under President G.W. Probably not.

I am guessing they chose that timeframe to coincide with the March 2009 bottom. According to the article, the only "assetallocation" fund to outperform the S&P 500 over the last 15 years has been the PIMCO StocksPLUS Long Duration Fund (PSLDX) which ironically enough is a leveraged fund tracking 100% each to stocks and long term bonds.

President Obama’s term, starting in 2009, began when stock market valuations were near the bottom and as is well documented now, the stock market went on to its longest bull market in history. For example, the September 11th terrorist attacks and the 2008 Great Financial Crisis occurred under President G.W. Probably not.

And it not only has the advantages of there being inefficiencies, so there’s the potential to generate alpha, but if you do it right, it’s pretty non-correlated with probably the rest of your portfolio. We want to focus on the well-being of our clients, our portfolio investments in their communities, and our team members.

The DJIA closed 1999 at 11,497 and 2009 at 10,428. At the GFC bottom, March 9, 2009, the Dow traded at 6,547. Some years ago, The Wall Street Journal asked him how, given his work, he structured his own portfolio. So, he missed it by a mile. The DJIA did reach 35,000 in June 2021, but Dent had long been a permabear by then.

And what we figured out in 2009, really when we started buying homes is that we made the bet that it, I mean, it wasn’t a very exotic bet, but we made the bet that the subprime mortgage market wasn’t coming back at all. And so, so starting in 2009, we, we, there was no flip market.

She was CIO at Merrill Lynch Asset Management, and now CIO at both Morgan Stanley Wealth Management and runs their assetallocation models and their outsourced chief investment officer models. 00:20:56 [Speaker Changed] So, so let’s talk a little bit about what goes into managing a hundred plus billion dollars in assets.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content