This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

His work covering the advisor tech space began in 2007 when he joined InvestmentNews as the advisor industry’s first dedicated technology reporter. Prior to his six years with WM , Janowski worked for Forrester Research as an analyst covering Digital Wealth Management. now Pontera).

His work covering the advisor tech space began in 2007 when he joined InvestmentNews as the advisor industry’s first dedicated technology reporter. It has become a challenge to keep up with new rollouts. Let’s take just this week. In edition, he has worked for two FinTech startups, Wealthfront and New York-based FeeX, Inc. now Pontera).

Davis Janowski , Senior Technology Editor, WealthManagement.com June 20, 2025 5 Min Read Dr. Naomi Win, a behavioral finance analyst at Orion, gave a presentation entitled, “Aligning Lives and Portfolios: Meeting the Moment for Modern Investors” at Wealth Management EDGE. Given the title, I was at first worried, but her talk was fascinating.

Bonds with duration are now more volatile than they used to be and that volatility is less reliable than it used to be making them a less effective diversifier for the equity portion of a diversified portfolio. The simplest example would be the person to retired at the end of 2007 and then 12 months later, the stock market was 39% lower.

You hear the word recession and might be reminded of the Great Recession from late 2007 to mid-2009. The red numbers in your portfolio are only losses on paper. Look into your emergency fund, consider picking up a secondary source of income, and explore other options before dipping into your portfolio. It is their natural cycle.

It was 101% at the end of 2019, and 137% just before the financial crisis in 2007. That’s up from 183% at the end of 2019, and close to the 219% we had back in 2007, except now it’s happened without households taking on as much leverage. That’s up from 210% at the end of 2019, and 160% in 2007.

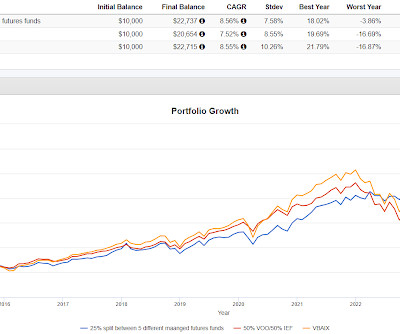

There's no way to fit that many into a portfolio without having a portfolio of diversifiers hedged with a little bit of equity exposure which I don't think would be optimal. To my knowledge, RYMFX was the first managed futures mutual fund and it had the space to itself for several years after in launched in 2007.

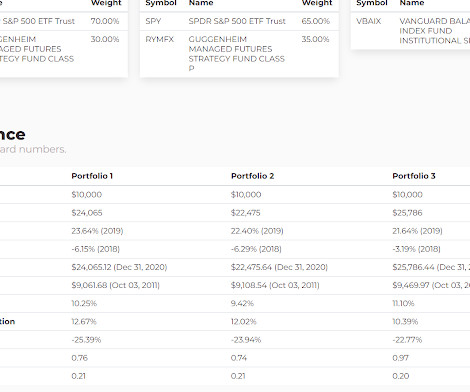

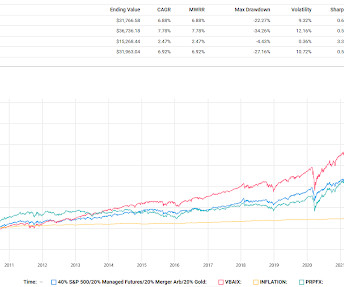

When they talked about portfolio allocations he said they want to have enough in managed futures to have an impact on the portfolio. Portfolio 1 as follows Portfolio 2 is 50% VOO and 50% iShares 7-10 Year Treasury ETF (IEF). Portfolio 1 is 0.06, VOO/IEF is 0.61 We looked at a similar chart the other day.

William Priest, chairman, co-chief investment officer, and a portfolio manager at TD Epoch, picked Meta (+66 percent), which handily beat the S&P 500, but his other four picks did not. In 2007, Steve Ballmer, then the CEO of Microsoft, said , “There’s no chance that the iPhone is going to get any significant market share.

If you put 3% into Ariba Networks into a diversified portfolio in 2000 or bought a house you could comfortably afford in 2007 then you had a setback but weren't blown up. I posted the above joke on Bluesky a few days ago. This person will get blown up if anything bad ever happens, absolutely destroyed.

If you have a taxable portfolio of at least $1 million where selling or rebalancing would hit very hard tax-wise, you can exchange your portfolio for shares in a 351 ETF. We build portfolios here all the time with similar return profiles but with less volatility. 351's are kind of like 1031 exchanges in real estate.

Barron's has an article about how to protect your portfolio , er sort of. Basically, after a couple of quotes from William Bengen, father of the 4% rule, about his tactical portfolio currently being 37% allocated to equities, there are a couple of suggestions from William Bernstein about just having less equity exposure. Portfolio No.

When you get it wrong, it crushes your retirement plans. My own track record at making big calls is pretty damned good, but none of our clients wants me slinging around their retirement monies based on my gut instinct. The dotcom top, the double bottom in Oct 02-March 03; the highs in 2007, the lows 2009.

My portfolio was tiny; I had no 401k, and my wife’s 403(b), with less than a decade’s worth of contributions, was barely 5-figures. By then, we began to have meaningful assets in our savings/retirement accounts and the bear markets had a bigger economic impact on those finances.

Barron's had an article about rebalancing portfolios noting that the run in stocks was a good time to rebalance the equity allocation back down closer to target, whatever that might be and also rebalance down some of the relative winners. Over the years, I've trimmed here and there when holdings get too big relative to the portfolio.

My Two-for-Tuesday morning train WFH reads: • Stock Pickers Never Had a Chance Against Hard Math of the Market : In years like this one, when just a few big companies outperform, it’s hard to assemble a winning portfolio. If you’re depending on income to fund your retirement, 5% rates are a blessing. 2007-09 Great Financial Crisis 7.

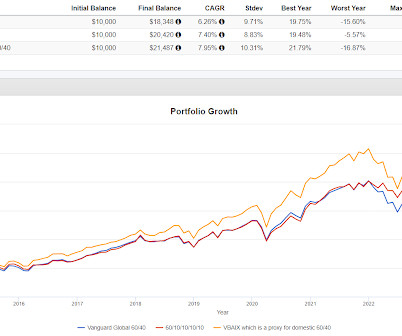

So it is with portfolio construction. The basic, most elementary portfolio construction is 60/40 equity/fixed income. Yahoo Finance has the Vanguard Balanced Index Fund (VBAIX), a proxy for a 60/40 portfolio, down 22.6% Anything unique that an incident calls for builds off the basics. this year versus down 24.8%

Starting back in 2007 or 2008 I wrote about his barbell portfolio idea that goes very high risk with 10% of the portfolio in search of asymmetric returns and then very conservative with the other 90%. The returns generated from the 10% could almost be enough for the entire portfolio. Here's an example of the effect.

At Citi, in 2007, fantastic timing, you take over as Head of Structured Solutions. And so, 2007, I came over to Citi. And when you think about market timing was 2007 the best time to — to make a move, but it ended up being a perfect time actually long-term for — for my career. BITTERLY MICHELL: Always risk.

There is a secondary, more subtle point that relates to portfolio construction and portfolio theory as we discuss here and as I have implemented into client accounts. Back in 2006 and 2007 there were far fewer funds available to help offset large stock market declines.

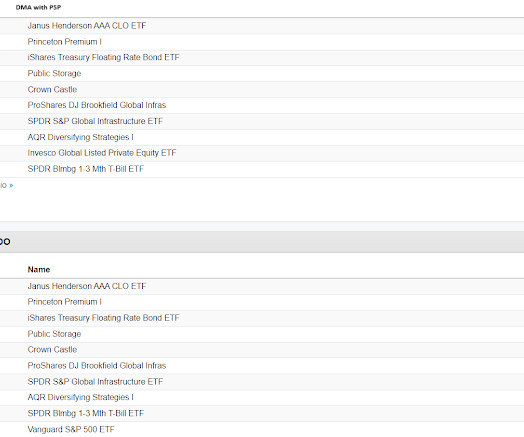

I built two version of this allocation with the only difference being that in Portfolio 1, for private equity I used Apollo Asset Management (APO) and in Portfolio 2 I used the Invesco Global Listed Private Equity ETF (PSP). Portfolio 3 is the Vanguard Balanced Index Fund (VBAIX) which is a proxy for a 60/40 portfolio.

Automatic enrollment has tripled since 2007. Outside of a retirement account, I see nothing wrong with holding six months of living expenses or something like this. Inside a retirement account, I can't think of a good reason why 9% of your portfolio should be earning next to nothing. This is a beautiful chart.

More interesting than the articles sometimes are the comments as was the case today with the following comment: What is really wacky is the Modern Portfolio Theory promoted use of bonds in a portfolio.ballast (or theoretical risk-reducing agent). Small allocations don't become impediments to portfolio growth, simply they are laggards.

Barron's had a fun article that looked at some ideas from William Bernstein titled The Trick To A Bullet Proof Portfolio? Based on the title, it would seem to be in the neighborhood of creating an all-weather portfolio which we've looked at in several different forms over the course of my full 19 years of blogging.

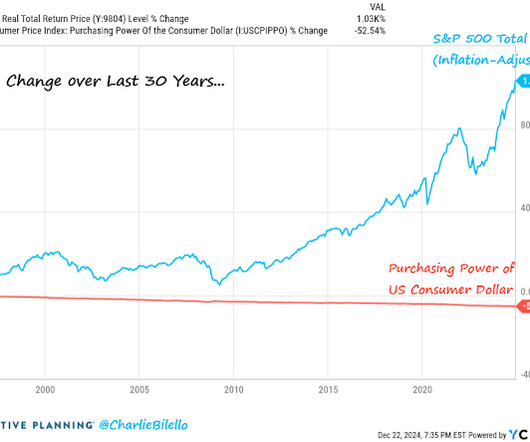

The S&P 500 fell an eventual 57% from its October 2007 peak before bottoming on March 9, 2009, and finally ending the global financial crisis (GFC) bear market. Retirement funds had been demolished and there was very little hope. A diversified portfolio does not assure a profit or protect against loss in a declining market.

Basically you allocate most of a portfolio to beta, plainer vanilla, not necessarily just Vanguard Balanced Index Fund (VBAIX) but you could and then add some sort of alpha seeking strategy on top of the beta. The fund has been around since 2007. This typically means incorporating leverage one way or another.

There are enough incidences here though that anyone buying these should expect that they are adding a lot of volatility to their portfolios. It's total return CAGR going back to 2007 was +5.29% and price-only was -3.50%. I'd have thought there'd be a lot that would have fallen 30% but based on a casual glance, it wasn't that bad.

Or you could look at the 2007 high which was within a few points of the 2000 high and say it took 12 years to double. Since we cannot know the path, this really spotlights a couple of important portfolio management concepts. If nothing else, it will make for some fun portfolio theory blogging when the track record is a little longer.

Usually a replication strategy will build a portfolio based on reported hedge fund holdings filed on a 13f or in the case of managed futures will sample maybe the ten biggest futures markets believing they can get 90% (or some high number) of the full effect, do it for cheaper such that the cost advantage ends up being the difference in performance.

Locking in for ten years at 4.50%-5% (this was 2006 and early 2007) made no sense to me. For me, bonds are about mitigating the volatility from the equity portion of the portfolio, the portion where I do want capital gains to come from. The quadrant inspired portfolio above will hopefully be more resilient in times of strife.

A recent survey from the Nationwide Retirement Institute® uncovered topics business owners are looking to discuss including economic pressures and business-specific challenges such as access to capital, the tight labor market, employee benefits, and supply chain disruptions. Many are actively seeking the guidance of a financial professional.

Even Mr. Money Mustache, as a person who retired 17 years ago, is still in this boat for the simple reason that my retirement income from dividends and hobby businesses is still greater than my annual living expenses (which still hover around $20,000 per year). (It’s the current blowup) -20% so far What’s your guess?

If you’re at all interested in focused portfolios, the concept of quality as a sub-sector under value and just how you build a portfolio and a track record, that’s tough to beat. Dick Mayo was a traditional, I’d say portfolio, strong portfolio manager focused on US stocks. He’s a big picture guy.

In the short run, there can be distortions in public market valuations as we saw in 2001 and we saw prior to that in 2007, and prior to that in 2000, in ‘99. How do you use all of this data that’s generated by all of your portfolio companies to navigate the world at large? BARATTA: Yeah. In the long run. We can’t do that.

Years ago, maybe 2007, I said no to being a partner at my firm. My blogging evolved a lot over the last 12 months into a lot more of what I would call portfolio theory with the capital efficiency and return stacking stuff. The work episode helped me better understand how much value I place on simplicity. The reasoning was very simple.

We like to look at the “prime-age” (25-54 years) employment-population ratio, since it gets around definitional issues that crop up with the unemployment rate (someone is counted as being “unemployed” only if they’re “actively looking for a job”) or demographics (an aging population with more people retiring and leaving the labor force every day).

A few days ago I bagged on a strategist from Vanguard for telling investors to stick with bonds in a 60/40 portfolio allocation. In that post we put together a 60/10/10/10/10 portfolio with just 10% to bonds and the other 10% sleeves into different alts that each represented uncorrelated return streams.

The Permanent Portfolio-inspired Cambria Trinity ETF (TRTY) allocates 35% to trend. Saying TRTY is Permanent Portfolio-inspired is my impression, I don't know that Meb has ever described it that way. It made me feel even luckier to have stumbled across the strategy back in 2007. Meb is a huge believer in trend.

In this article, we bring you some top stocks under Rs 2000 that you can consider including in your portfolio. . During his tenure, he scaled the bank multi-fold and became the longest-serving managing director of a private Indian bank till his retirement in 2020. . Is it some fascination with ‘2016’s aaj raat se….’ 852,000 EPS (Rs.)

That’s a really easy portfolio to create. It allows you to understand, generally speaking, what is a reasonable beta for that whole portfolio. By the time I got there in ’92, they had a great venture portfolio and almost nobody else even understood what venture capital was. This is the summer of 2007.

Walter Cabot, the new portfolio manager, wrote: Times change. Portfolio managers would no longer rapidly trade these growth stocks, instead they would invest in blue chips like IBM and Disney, and no price was too rich. With people living longer than ever, we need to expect and be prepared to fund a long retirement.

But what was interesting about that was the quick need to both separate the portfolio between the old stuff and the new stuff, because there were a lot of new investment opportunities. So we have our MAS team, our Multi-Asset Solutions team, who are really providing more of the overall portfolio advice. RITHOLTZ: Really intriguing.

There was a lot of content from various places over the weekend about whether it is time to go back into bonds, what retired investors should do for yield and even whether retirees are better off going 100% into equities. This chart contributes to the logic supporting a 60/40 portfolio. The working answer here has been no.

And this is how I tested it Both Portfolio 1 which I'd say is the truer version and version 2 increased proportionally do a little better than VBAIX but with slightly higher volatility. I wrote about them a couple of times, ages ago including here at TheStreet.com in 2007. AOR is a proxy for a 60/40 portfolio.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content