This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The idea of living off dividends in retirement sounds nice, but investors often don’t realize how much money they’ll need invested to generate enough income from dividends to cover lifestyle expenses. If you own 10,000 shares, you receive $40,000 in dividend income (before taxes) and have a portfolio currently worth $2M.

All costs impact your returns, but high or excessive fees have an enormous impact as they compound or, more accurately, lessen your portfolios compounding over time. My buddy could pay off his mortgage and car loans, pre-pay the kids colleges, fully fund retirement accounts, and still have cash left over.

Interest rates going up doesn't worry me from a portfolio perspective, I pretty much don't have any interest rate risk in the portfolio. My first thought is to think about the all-weather attributes of Permanent Portfolio-inspired, quadrant investing. Portfolio 3 is sort of close to what we blog about regularly.

There was no version of the word complexity in the article but I think Jason was trying to sort out the idea of complexity in a portfolio. I would imagine he'd be less inclined than me to include a little complexity into a mostly simple portfolio. The issues with interval funds make them complex complexity.

Mutiny Funds put out a paper on the hows and whys of using alts for The Cockroach Portfolio that they manage and that we've looked at a few times. Picture retiring in 2010 versus 2020. Mutiny makes a point that I've been writing about and have embedded into my process since 2004. There are expectations embedded in these numbers.

There are about 13 different portfolio managers each focused on a different sub-sector. 00:06:36 [Speaker Changed] So in, in 2004, I joined Morgan Stanley equity research. He, he had retired, retired, but he was still active. Since then, it’s grown to about $7 billion. And they are not the typical hedge fund.

Outside of a retirement account, I see nothing wrong with holding six months of living expenses or something like this. Inside a retirement account, I can't think of a good reason why 9% of your portfolio should be earning next to nothing. The biggest takeaway for me here is the cash number. There is way too much of it.

Making changes to client portfolios' overall volatility through the duration of a stock market cycle predates when I started blogging in 2004. Certain funds and stocks when added to a portfolio can either increase or decrease volatility, here's a good example with ARKK. The ways in which I do that have evolved over that time.

Yeah, that lot that talks about terms like compounding, risk profile, returns, retirement planning, budgeting, Investing, and whatnot! It aims to generate long-term capital growth from a diversified portfolio of predominantly equity and equity-related securities. It has been in existence since August 16, 2004. 1-yr return 2.5

One of the partners of the firm where I have been since 2004 was found to have done illegal trading and he was immediately terminated. My blogging evolved a lot over the last 12 months into a lot more of what I would call portfolio theory with the capital efficiency and return stacking stuff. Thankfully a few weeks later they did.

Both in terms of the aggregate revenue of our company, size of our portfolio, we’re probably now something like 150 total investments, many hundreds of billions of revenue, hundreds of thousands of employees if you add up all of the companies in which we’re invested. And, you know, why is that? We started doing deals on our own.

There's a lot of neat things about 19+ years of blogging, I started in Sept 2004, including circling back around to ideas that we started talking about a longggggg time ago. With that preamble, I started thinking about the 75/50 portfolio that I first started writing about during the Financial Crisis. ARBFX 3.7%

The title tells you the author's conclusion, Why Your Portfolio Should Hold Way More Than 30 Stocks. If a portfolio starts with 40 holdings each with an equal 2.5% So while it would be rare to have one go to zero without you paying attention and taking action, I think the typical portfolio could ride out something in the 2.5-3.5%

She has a fascinating career, starting a PLS working away up as an analyst and eventually, head of outcome-based strategies for Morningstar, eventually rising from that position and portfolio manager to Chief Investment Officer. Let me give you some background on Morningstar Managed Portfolios. I saw how personal money is.

I’ll have to be when I retire and publish under Anonymous. And they end up being great candidates for us to put into to run the next big portfolio or start a new strategy. It was a spin out from, so this would have been 2004, spin out from a well-known prop group, to my point on doing work for a lot of the prop groups.

GLD started trading on November 18th, 2004. Where a small slice was permanently allocated to gold to reduce the portfolio's correlation to the market, gold is being replaced with a small slice to managed futures for the same purpose. A friend that has been by my side for 17 or 18 years, helping out more often than not.

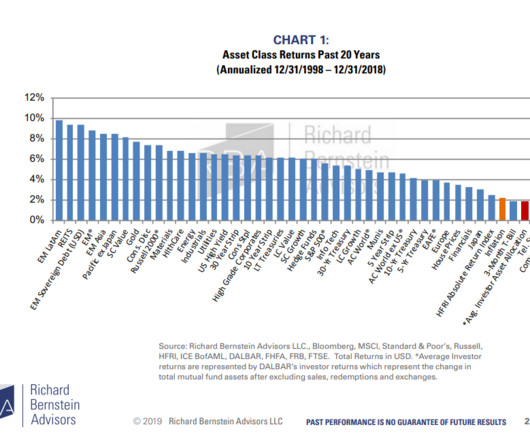

The emerging markets asset class outperformed all others in 2003, 2005, 2007 and 2009, while finishing second in 2004, 2006, and 2012. large cap horse, lest your portfolio run the risk of colliding into a trolley cart of horse manure returns. jigawatts of investing power (and volatility)! Sounds unstoppable, right?

And so, I was doing that in 2000, 2002, 2003, 2004. of that fund had to call himself a portfolio administrator. RITHOLTZ: You made my retirement …. It’s going to be the core of most (inaudible) portfolios because it’s just too — too good of a deal. RITHOLTZ: (Inaudible), right. And in 2006, I got a hand at ETFs.

So the fact that I had a sociology degree really didn’t impede, I think getting into business Barry Ritholtz : And you end up in like what some would think of as kind of a dry, legalistic part of Fidelity, the ERISA Division, which focuses on retirement accounts. Nobody cares about your portfolio.

Since 2004, the tax rate on dividends and capital gains is 15 percent, 18 percent, 21 percent. But if you load up your portfolio with those, God only knows what a year or two from now you’re going to be looking at because these companies are going to be forced to cut their dividends. They match up. RITHOLTZ: Right.

In the earliest days of my blogging at the original URL, I would occasionally describe the blog as a look over my shoulder at how I navigate market cycles and learn more about portfolio construction and management. The Type 1, the new green one, is a 2004 with very low miles and very low hours on the pump. Sidebar, never stop learning.

In 2004, Jonathan Clements wrote: With the formula that Dalbar uses, stock-fund investors don't earn the full monthly return on any money that they invest during that month. The main culprit for the portfolio gap is cash, which we spoke about with Morgan Housel recently. The fully invested 60/40 portfolio would have done 9.4%

You were a portfolio manager, researcher head of trading, and apparently tech geek putting machines together. You know, when you have these quarterly reviews of what’s going in the portfolio, invariably the discussion is let’s talk about the things that are down the most. So at A QR you juggled a, a lot of responsibilities.

The currency devalued by 75 percent and my portfolio, which was above $1 billion, went down 90 percent. And this had an unbelievably positive affect on the value of my portfolio. At that moment in time, 2004, Vladimir Putin became the — becomes the richest man in the world. And so, they defaulted on the domestic bonds.

Early retirements have been taking place a giant uptick in new business formation. And I think, you know, if you look at the 2004, 2007, eight period, boy, it would’ve been really good if we’d done something about subprime mortgage lending, about mortgage underwriting standards.

And arguably, they went from an underpriced position in 2004 I’d say — RITHOLTZ: Right. RITHOLTZ: So I said something at an event where I had said to a group of young people, hey, if you’re in your 20s, 30s, 40s, you really don’t need bonds in your portfolio. I mean, it’s used to be called FANG. SIEGEL: Yeah.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content