This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

For many financial advisors, a core part of the retirement planning process involves simulating whether the client's assets will last through retirement. One way that advisors can help bridge this gap is by using Historical Market Visualization (HiMaV) as a more intuitive alternative for illustrating retirement income strategies.

Also on the site The question with emerging market equities is if, not when. morningstar.com) Bull markets have four distinct stages. econbrowser.com) How retirement can open you up to new possibilities. humbledollar.com) When it doesn't make sense to move in retirement. peterlazaroff.com)

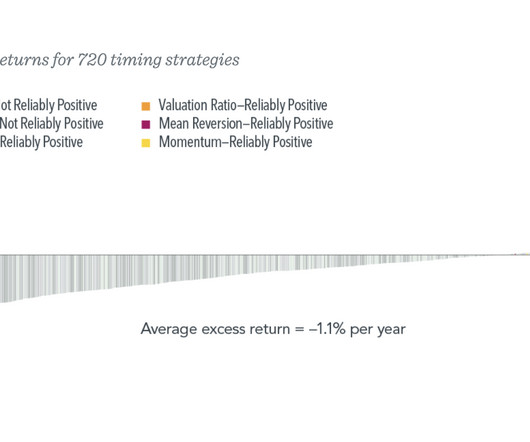

This weekend Jeff Sommer discussed a DFA research paper on market timing; both are well worth your time to read. The broad strokes are: Market timing is extremely difficult, very few people (if any) do it consistently well. Low Stakes : The most successful market timers are often those people who do not have actual assets at risk.

These days, turning on the TV to get the latest news about the markets and the economy can be enough to send anyone into panic mode. The second section of your book focuses on Bad Numbers, or in other words, misleading numbers that could drive the economy, the markets and ultimately, your investments.

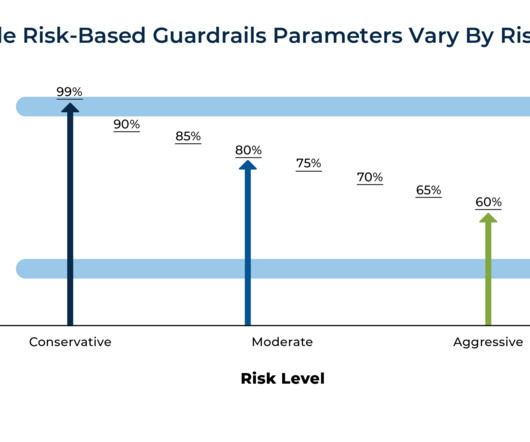

When planning for retirement, it’s effectively impossible to precisely forecast the performance and timing of future investment returns, which in turn makes it challenging to accurately predict a plan’s success or failure.

downtownjoshbrown.com) What's driving stock market returns? humbledollar.com) Why planning in retirement is so challenging. humbledollar.com) Doing the math on a hybrid vs. conventional ICE. (wsj.com) The wealth management industry is going to be slammed with demand.

(peterlazaroff.com) Bogumil Baranowski talks with Brian Feroldi, author of "Why the Stock Market Goes Up." open.spotify.com) Retirement Nine things to consider in retirement. tonyisola.com) Retirement is, in part, about saying no to obligations you don't like. humbledollar.com) How to find abandoned retirement accounts.

(wsj.com) Housing Options are few for people looking to get into the housing market. awealthofcommonsense.com) Home buying math is bad right now, but will it be any better a year from now? bloomberg.com) Personal finance Things to do before pulling the plug on your job and retiring. msn.com) Five formulas for wealth.

If only there were some ways to prevent investors from interfering with the markets greatest strength the incomparable and guaranteed ability to create wealth by compounding over time. Drawdowns, corrections, and crashes are not the problem your behavior in response to market turmoil is what causes long-term financial harm.

Let’s be honest, retirement isn’t what it used to be. The traditional blueprint of working until 65, collecting a pension, and retiring feels outdated, especially for mid-level professionals who’ve started thinking early about what their ideal retirement should look like. What’s the earliest you can retire?

Autos Ben Carlson and Michael Batnick talk with CarDealershipGuy about the state of the American car market. theirrelevantinvestor.com) Peter Lazaroff talks with Jesse Cramer about the math behind car ownership. peterlazaroff.com) Retirement How retirement can open you up to new possibilities. Life intervenes.

million in assets to both retire and pass on a legacy interest (though many have yet to establish an estate plan), according to a recent survey. Enjoy the current installment of "Weekend Reading For Financial Planners" – this week's edition kicks off with the news that affluent Americans believe they need an average of $5.5

Morgan Housel Finance types tend to focus on attributes like intelligence, math skills and computer programming. You can know everything about math and data and markets, but if you don’t control your sense of greed and fear and you’re managing uncertainty in your behavior, none of it matters. None of it matters.

Is retiring with a mortgage a good idea? Retiring with a mortgage doesn’t typically pose a financial risk, and at times it’s the best financial decision. But paying off a mortgage before retirement has upsides also. Here’s when it may – and may not – make sense to pay off a mortgage before retiring.

The value of the S&P 500 index of stocks, where most of us hopefully have a good chunk of our retirement savings stashed into index funds, is up about fifty seven percent in just the past two years. Does this make it more vulnerable to a huge crash in the future, and will it affect my retirement? Now back to the stock market.

The recent stock market activity has given us plenty of opportunities to experience extremes of emotion… but then again, you can pretty much choose any time period and make a similar statement. There’s no shame in admitting that factor – for a lot of us, math can be very tough.

While a Roth conversion may never make sense for some individuals, for others, early retirement years may be the best time to convert pre-tax accounts to tax-free Roth. Converting a traditional IRA to a Roth doesnt make sense unless you have cash to pay taxes without dipping into your retirement savings.

Bill Hester from Hussman Funds had a lengthy write up on diversifiers that track what he called Bear Market Cumulative Returns (BMCR). A portfolio that goes narrower than an S&P 500 500 or total market fund probably has some exposure to low vol, dividends and the others. for example. Now for a little more fun.

Meb Faber : Well, it’s a romping, stomping bull market. And that’s the broad market. And the way math works, you end up with a stock that goes up a bunch. We’ve done the math on some of these high-yield portfolios and taxable accounts.

The simple 40 year trade for bonds of "number go up" is finished and as a matter of math, can't be repeated. Part of where I am coming from on this is how terribly wrong the consensus has been on how to engage fixed income markets for such a long time. Taking volatility out of a fixed income portfolio is fairly simple.

Jason Zweig wrote an article titled How Not to Invest in the Bond Market. The article devoted a good amount of space to bond marketmath, focusing on the pain of owning the iShares 20+ Year Treasury ETF (TLT) and bond funds in general. The title of course piqued my interest.

Matt Kory, Vice President, Retirement Programs As a retirement income vehicle, the 401(k) is second in popularity only to Social Security – and as CNBC reported in 2019 the number of 401(k) millionaires is at an all-time high. But is a million dollars even enough for your retirement needs? Just think of the numbers. Trade wars.

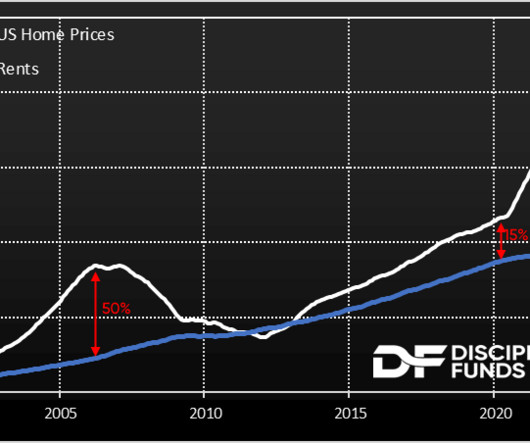

COVID created an incredible disequilibrium in the housing market where house prices surged 40%+ and rents are only just playing catch-up. If we assume that the market is remotely efficient then these prices should converge. Now that’s a bear market in real estate. And that’s where the math on renting comes into play.

For most, Social Security provides a solid foundation for retirement income. As you grow older and retirement looms on the horizon, the decisions you make start to have a more crucial impact on the amount of money you receive, so it’s important that you know what to expect. Plus, it’s guaranteed for life! [2]

My Two-for-Tuesday morning train WFH reads: • Stock Pickers Never Had a Chance Against Hard Math of the Market : In years like this one, when just a few big companies outperform, it’s hard to assemble a winning portfolio. Businessweek ) but see With cash earning 5%, why risk money on the stock market? Can a New One Succeed?

Advisors offer insights on retirement, long-term care, or market trends over lunch at a local café or conference room. One advisor noted that these events draw not only current clients but also curious prospects who are actively exploring retirement planning options.

This is very important for retirement, and knowing what your target net worth by age should be will help you better understand how to reach your personal financial goals. If you own a lot of stocks, keep in mind that your exact net worth could vary depending on the stock market. Basically, it calculates how wealthy you are.

It's been a while since this sort of thing was relevant for my day job so something could have changed, weeklies didn't exist for example, but if my math is correct then it was way over exposed which would account for last week's decline in the fund price. Please leave a comment if I did the work incorrectly.

The term personal finance ratios might be giving you flashbacks to math class. You can use ratios to keep track of many different aspects of your financial situation—from cash flow to savings to retirement and more. Money in a checking, savings, or also money market account is highly liquid.

I haven't seen too many scenarios where Roth conversions were optimal as most people don't earn more after they retire. Do the math on your particulars like what your various sources of earned income will likely be, how much your RMDs will likely be and so on. How much are you likely to end up with in your retirement accounts?

In that event, I think doing better than the broad market probably just came down to luck in reiterates a point I should be making more often that fast declines, aka panics, aka crashes are not be feared anywhere near as much as slow declines which typically take much longer to recover.

Recessions can bring layoffs, reduced hours, and shrinking markets. Demand is likely to continue as more and more people in the Boomer generation reach retirement. Freelancing, virtual assistance, tutoring, pet care, and digital marketing services all require minimal startup costs.

In the three months or so since we last spoke, the world has become an entirely different place – at least for those of us who keep up with any sort of international, financial or stock market news. The bottom line is that the overall US stock market is down about 20% over the past three months. Data source: S&P market data.

And so I realized I was going to have to invest and save for my own retirement. Bill Bernstein : I’ll give credit to a guy you may have heard of named Frank Armstrong, who was one of the early efficient market passive indexing advocates. I couldnt figure out where it came from; so I worked out the canonical math.

Interest rates are different and have a much more meaningful impact on the economy by damaging banks and credit markets. In the case of the global bond market we’ve seen a $10 TRILLION decline in value since the Fed began raising rates. This is the basic math behind what’s happened to every consumer who owns these bonds.

The way Portfolios 1 and 2 are weighted, the math works for being a 60/40 portfolio and then from there we add portable alpha/capital efficiency/return stacking. Ok, well that's not the sort of thing you read when markets are fearful. The idea here is to look to see if any value can be added. I'm a research volunteer.

Keep it to something broad like a total market fund or a market cap weighted large cap index. And then just a little math, the "guarantee" based on the 50/50 allocation would be 2.5% Pivoting to an idea for a barbell equity strategy prompted but a short paper about the Simplify Hedged Equity ETF (HEQT).

The math behind Universal Life Insurance Interest Rates is a twisted web and most consumers are deceived. Know how the math works so you can see the potential risks that may exist with your policy. Money market rates crashed to zero (0%) in 2022 due to Covid-19. Don’t be fooled! Are you disturbed yet?

She has a really fascinating background, very eclectic, a combination of math and law. You, you get a, a BS in Mathematics and a JD from Boston University Math and Law. It is something, math has always come easy to me since a child. I didn’t get an advanced degree in math. Not the usual combination. What happened?

By enrolling in this course you will learn to manage your finances more effectively by mastering budgeting and portfolio creating for a healthy retirement corpus. From the above concepts you will learn how to approach financials and plan for your retirement goals with good risk management. You can enroll in the course here.

Once you know your weekly or monthly income, you can do the simple math of calculating how much 70% would be. We all need an emergency fund, and to save more long-term (think: retirement). Don’t put it into a retirement account where you won’t be able to get the money out for years.) Consider some of these ways to save.

She really has an incredible background in everything from capital markets to derivatives, to wealth management. You’ve been involved with capital markets for your entire career. It’s a town of about 4,000 people, so exposure to markets or investment banking or any of the careers in finance was not something that you really envisioned.

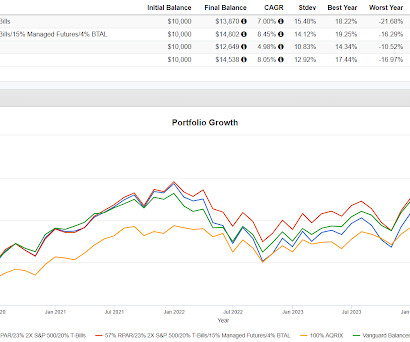

Simple math, it looks like the carry index has compounded at less than 3%. If you've ever heard the cliche that in a crisis, all correlations go to 1, in the face of some sort of market spasm it is possible that stocks and managed futures get hit in the same manner at the same time. The red line for T-bills is price only.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content