This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

We have previously discussed ( see this , this , this , and this ) why the 20% bull/bear frame of reference is simply noisy nonsense. They all have different sensitivities to economic factors like trade, inflation, commodities, and growth. Note we have not even referencing the valuation debate.

My greatest contribution to the field of economics is my General Theory of Assflation. I am referring to my explanation of “asset price inflation” relative to QE. I jokingly referred to this as assflation because how else can you respond to things that seem obviously wrong, except with a joke? But are they?

Economic news that showed a 2.2 9 This Week: Key Economic Data Tuesday: Fed Officials Neel Kashkari and Patrick Harker speak. Source: I nvestors Business Daily – Econoday economic calendar ; November 8, 2024 The Econoday economic calendar lists upcoming U.S. The yield on the 10-year Treasury fell to 4.307 percent.

As a result, its often incumbent upon the retiring advisor to either accept a discounted valuation for the book and/or show a great deal of flexibility in how their next gen ultimately takes the reigns of the business. But is that fair? After all, shouldnt the retiring advisors be compensated fairly for their lifes work?

Estates Estate Planning in this Economic Climate Schedule a Complimentary Financial Review CLICK HERE TO SCHEDULE. Between inflation, increasing interest rates, federal changes to monetary policies, and global conflict, many factors are putting a strain on the current economic situation. Create a Trust . Work with the Professionals .

This refers to the strategy where you just move everything into T-Bills and “chill” 1 This move sounds increasingly enticing. These are the highest rates we’ve seen since the mid-2000s so it’s a welcome change from the 10 years of ZIRP (zero interest rate policy). After all, 5.5%

At this rate, home sales will likely continue to slow and residential investment could turn out to be a drag on Q3 economic growth. Any economic forecasts set forth may not develop as predicted and are subject to change. References to markets, asset classes, and sectors are generally regarding the corresponding market index.

at year-end can largely explain the compression in valuation, especially for higher multiple equities, primarily during the first half of the year. Since 1995, there are four rather distinct periods during which forward earnings estimates for the S&P 500 Index declined, tied to a specific event and/or economic downturn. by year-end.

The official arbiter of business cycle dating is the National Bureau of Economic Research (NBER). had never before experienced the massive swings in economic activity during the 2020 pandemic, making even the current analysis more difficult. The economic growth outlook has weakened. Of course, the U.S. However, after a 12.6%

This can be due to various reasons like global economic concerns or shifts in investment strategies. High Valuations and Sector Underperformance which Disappointed FIIs Most of the FIIs sold Indian stocks due to high valuation concerns and sector-wise underperformance. February -1538.88 March 35098.32 April -8671.27 May -25586.33

The National Bureau of Economic Research (NBER) is the official arbiter of U.S. business cycles, and they consider a wide range of economic indicators other than just the quarterly GDP metric. The three factors for defining a recession are depth, diffusion, and duration – conveniently referred to as the “three D’s.”

Economic activity does not stop like an airplane eventually does, but rather the economy will settle into a steady state where growth is consistent with factors such as population and productivity. Perhaps that was not the first time market watchers used the term, but the conversations at the Economic Club of New York were prescient.

Later in the year, markets became anxious about other topics, such as a potential economic slowdown, a new level of dysfunction in Washington (including unusual executive challenges to the Fed's independence and an extended partial government shutdown), and escalating trade disputes between the U.S. equity exposure.

Understandably, rising prices, slowing economic growth, and a challenging first half for both stocks and bonds have many investors on edge, and fatigue from more than two years of COVID-19 measures doesn’t make it any easier. Lower inflation tends to bring higher valuations (Fig.1). If the U.S. If the U.S.

Lessons learned: Economic forecasts The Fed’s bark was as bad as its bite! economy to avoid recession, and support above-average valuations. The hit to valuations in the form of about 4 P/E points (21 to 17) translates into a roughly 20% drop in the S&P 500 Index. Here are some of our lessons learned from 2022.

This has resulted in skyrocketing valuations of the stock markets. Nifty currently is trading at a multi-year’s high valuation. Whereas, the complete economic recovery is still far away and uncertain in terms of its timing and structure. Rising number of cases in Europe has been affecting the economic recovery.

The rule of thumb is two quarters of negative GDP defines a recession, but the official definition by the National Bureau of Economic Research is broader than that. Market-based interest rates—those not controlled by the Fed—have come down quite a bit, supporting stock valuations. economy contracted for the second straight quarter.

Weekly Market Insights: Stocks Climb After Fed Pause Presented by Cornerstone Financial Advisory, LLC Stocks climbed last week as reassuring inflation data boosted investor hopes that the rate-hike cycle was nearing an end amid fresh economic data pointing to continued economic resilience. Index of Leading Economic Indicators.

Today, we see this happening with the so-called “FANG” stocks—Facebook, Amazon, Netflix and Google (now Alphabet—for consistency we will refer to the company as Google throughout this piece). Investors also tend to naturally focus their valuation fears on big, rapidly growing stocks.

Today, we see this happening with the so-called “FANG” stocks—Facebook, Amazon, Netflix and Google (now Alphabet—for consistency we will refer to the company as Google throughout this piece). Investors also tend to naturally focus their valuation fears on big, rapidly growing stocks. False Connections.

Shifting macro cycles and heightened volatility across financial markets are only half the story, as investors and companies in a post-COVID world grapple with an ongoing geopolitical realignment and the increasing prospects of an economic recession. as a result of meaningful inflation across the economic system (Figure 3).

Recent economic data has pointed to continued growth—giving rise to the “no landing” narrative. However, the pressure on valuations from higher interest rates, which have made bonds attractive alternatives, led to the Committee’s recent decision to reduce the size of the overweight from 5 points to 3. equities.

The challenges are many, with intense cost pressures and slowing economic growth at the top of the list. These headwinds include slower economic growth, cost pressures amid high inflation, ongoing supply chain issues, geopolitical instability in Europe and Asia, and significant currency drag from a very strong U.S. Numerous Headwinds.

The rule of thumb is two quarters of negative GDP defines a recession, but the official definition by the National Bureau of Economic Research is broader than that. Market-based interest rates those not controlled by the Fed—have come down quite a bit, supporting stock valuations. economy contracted for the second straight quarter.

Given the country’s weak economy, due in large part to stringent zero-COVID-19 measures that have led to strict and prolonged lockdowns, coupled with a debt-laden property market, authorities in Beijing and throughout the Chinese provinces will need to focus on reviving the country’s economic underpinning. from an earlier forecast of 5%.

The quantum of money printing jumped massively after Corona-led economic shutdowns. However, we can think of three possible scenarios ahead: Irrespective of what scenario will pan out, equity valuations inevitably have to adjust according to the principle of mean reversion. US Fed increased its balance sheet size from ~$4-4.5

Balancing Act | For Good Measure: How We Value Global Leaders achen Wed, 04/18/2018 - 11:03 Valuation is a critical component of active investment management, yet many investors restrict themselves to a very narrow view of valuation by focusing on simple metrics like the price/earnings (P/E) ratio.

Valuation is a critical component of active investment management, yet many investors restrict themselves to a very narrow view of valuation by focusing on simple metrics like the price/earnings (P/E) ratio. This makes ratios like the P/E ratio dangerous as a valuation tool. Wed, 04/18/2018 - 11:03.

Some recent softening in economic data, coupled with signals from the bond market, may be indicating that Fed policymakers’ concerted inflation fight may be closer to the end than the beginning. We should also have slowing corporate earnings growth and greater economic uncertainty to contend with, some formidable seas to navigate.

The “Magnificent 7” has become a popular term on Wall Street, referring to seven large technology companies that have dominated stock market returns in recent years: Apple, Microsoft, Alphabet, Amazon, Nvidia, Meta Platforms, and Tesla. Strong return on equity (ROE): The company’s average ROE of 18.5%

Still, corporate America delivered the type of upside investors have grown accustomed to in much easier economic environments. We’re counting on inflation pressures easing next year while economic growth potentially picks up from the anemic level in the first half of 2022 to provide additional support. The numbers.

We know that equity valuations in the U.S. CURRENT VALUATION PREMIUMS, S&P 500 INDEX Metric Most Recent Long-Term Average Premium vs. Average Timeframe Trailing P/E 19.4 Please refer to the end of the article for a complete list of terms and definitions. We simply don’t know what might happen three months or six months from now.

We know that equity valuations in the U.S. CURRENT VALUATION PREMIUMS, S&P 500 INDEX. Please refer to the end of the article for a complete list of terms and definitions. Any number of factors could cause valuations to quickly readjust or correlations to spike. Most Recent. Long-Term Average. Premium vs. Average.

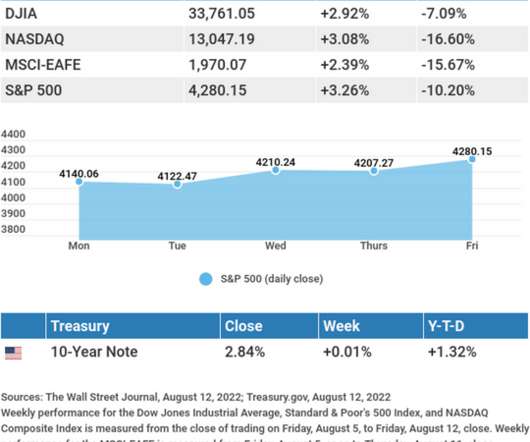

This Week: Key Economic Data. Index of Leading Economic Indicators. Source: Econoday, August 12, 2022 The Econoday economic calendar lists upcoming U.S. economic data releases (including key economic indicators), Federal Reserve policy meetings, and speaking engagements of Federal Reserve officials. Housing Starts.

Likewise, during periods of economic slowdown, temporary workers are typically the first to get the notorious pink slip. One risk is the high number of workers in temporary help services since these jobs often are the first to go during times of economic uncertainty. Investing involves risks including possible loss of principal.

That’s not suggesting another 2008 is coming, but rather highlights how fast the economic environment can change. Along with the statement, the Committee updated the Summary of Economic Projections (SEP), which is arguably more important than the brief monetary policy statement.

Economic and corporate data support the initial strong reads on holiday retail sales despite the macro headwinds, reinforcing the idea that today’s consumer is in a better position than usual at this point in the business cycle. Any economic forecasts set forth may not develop as predicted and are subject to change.

And when I was studying in university economics, I did not really get the passion. ILMANEN: It’s always good to think of starting yields and valuation sort of two sides of the same coin. What else goes into driving valuation factors that can lower future expected returns? Explain that. RITHOLTZ: Right.

And while there’s no guarantee that any job will be immune to cutbacks or layoffs, some industries weather economic storms better than others. CFOs typically have a deep understanding of economic theory and practice and strong analytical and problem-solving skills. One industry that tends to be recession-resistant is finance.

Market strategists and pundits make the relationship between recessions and the stock market seem binary, but each economic contraction is different and has different effects on earnings. First, keep in mind that stocks tend to look forward by four to six months and can provide warnings of changing economic conditions.

economic growth. More specifically, it reflects how the Fed intends to stimulate or slow economic growth by cutting or raising its policy rate. This is referred to as an inverted yield curve, which has been a pretty reliable predictor of economic recessions. The shape of the yield curve is not normal. The shape of U.S

While activity remains muted at best, expectations are focused on 2024, when there is a prevailing consensus that the Federal Reserve (Fed) will be finished with its rate hike campaign, and that economic conditions will be resilient enough to underpin a strong capital markets environment. With economic data continuing to suggest the U.S.

With a series of important economic indicators suggesting the economy is declining and inflation is finally decelerating, albeit very slowly, markets are beginning to factor in that the Fed may soon transition to a less aggressive stance in early 2023. Any economic forecasts set forth may not develop as predicted and are subject to change.

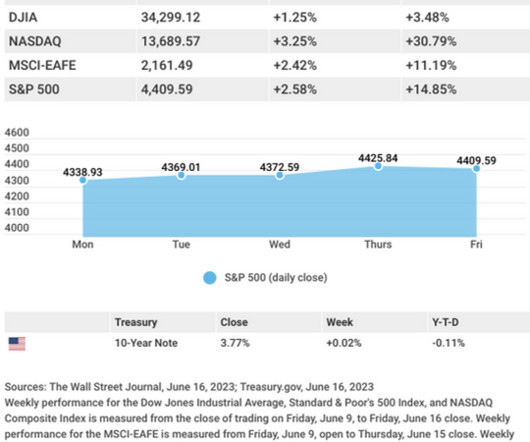

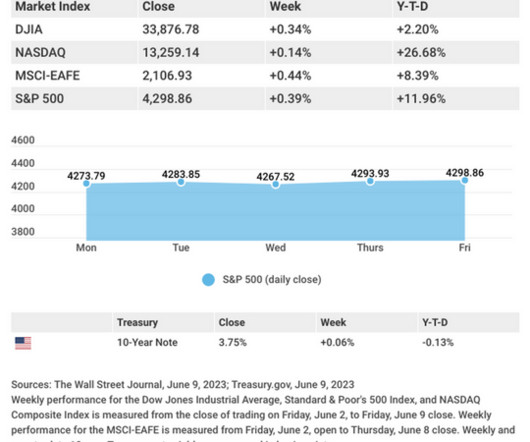

6 This Week: Key Economic Data Tuesday: Consumer Price Index (CPI). Source: Econoday, June 9, 2023 The Econoday economic calendar lists upcoming U.S. economic data releases (including key economic indicators), Federal Reserve policy meetings, and speaking engagements of Federal Reserve officials. FOMC Announcement.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content