This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

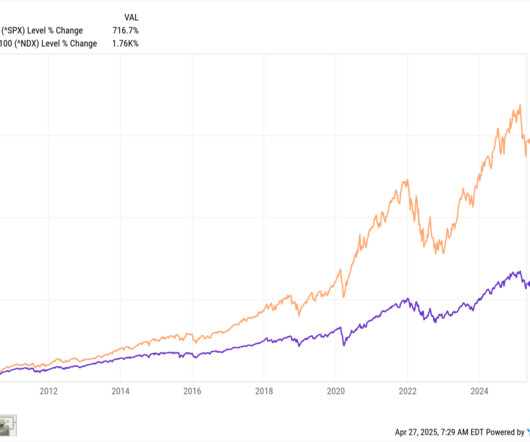

2022 down 18% for the year.4 What has developed over the entirety of the post-financial crisis era of rising equity markets and until 2022, falling or zero interest rates.The good news is that this is how you build wealth over the long haul. See also Lazy Portfolios rolling returns. Q1 2020 down 34% in the pandemic.

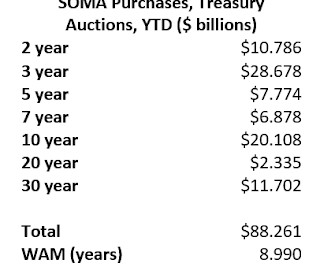

From housing economist Tom Lawler: From the beginning of 2020 to early June of 2022 the Federal Reserves balance sheet more than doubled to an almost inconceivable $8.9 Below is a comparable table for the end of 2022. trillion, with most of the decline reflecting decreases in Treasury and Agency MBS holdings.

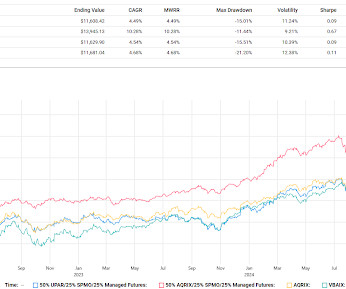

A fun rabbit hole over the years has been the 75/50 portfolio devised by John Serrapere which he wrote about several times at the old IndexUniverse site. For anyone new, the big idea is for the portfolio to capture 75% of the upside with only 50% of the downside. Portfolio 2 has a normal, even if not heavy, allocation to equities.

You're 81 and been taking income from your portfolio for 15 years, what matters to you more, that you can continue to take what you need from your portfolio or that four year run in your mid-50's when you beat (or lagged) the market? If you're 81 and can no longer meet your income need from your portfolio, that is what matters.

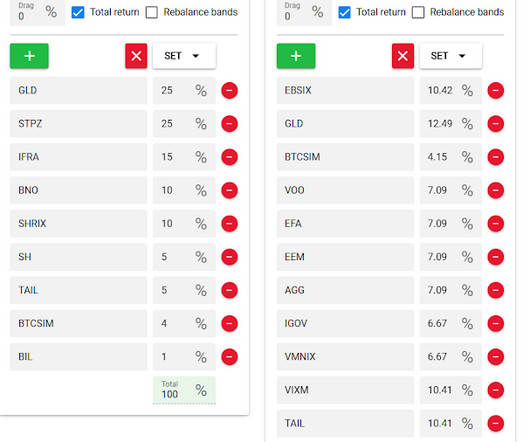

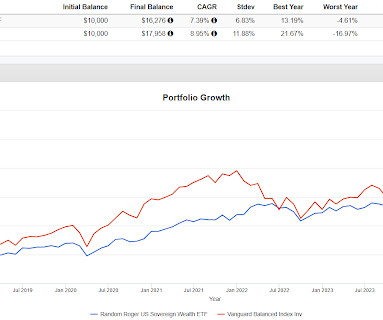

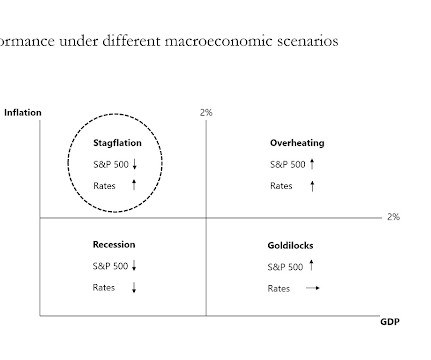

Let's dig in some more on Permanent Portfolio quadrant style. Next is the allocation for the United States Sovereign Wealth Fund ETF that I made up a few days ago and next to that is my most recent attempt from November to recreate the Cockroach Portfolio which is managed by Mutiny Funds. That is a very specialized type of result.

And on today’s edition of at the money, we’re going to discuss how Wall Street has been using personal health to gain a competitive advantage to help us understand all of this and its implications for your portfolio. How does that show up in our portfolios? Not only does that show up in our portfolios.

All costs impact your returns, but high or excessive fees have an enormous impact as they compound or, more accurately, lessen your portfolios compounding over time. I have made some fortuitously timed buys, including Nasdaq 100 (QQQ) calls purchased during the October 2022 lows.

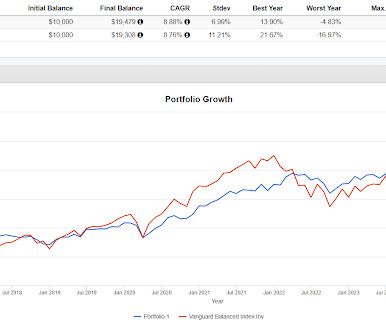

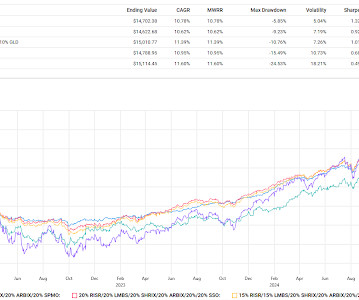

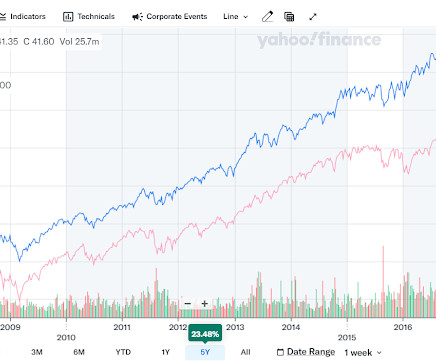

Which portfolio result would you rather have? Portfolio 1 is the only choice. The Portfolio 1 has the same longer term result at the S&P 500 but with only 58% of the volatility. You can see just by looking that Portfolio 1 has actually taken a very different path to a similar result as the S&P 500. A little quiz.

CREDIT: Joey Corsica & SpotMyPhotos Founded in 2022, Fynancial is already used by some big RIA firms, like Sanctuary Wealth and is integrated with many top technology providers, including eMoney Advisor, Orion and Wealthbox. The audience was impressed by Mili's presentation and their vision of where AI notetaking is headed.

Active investing involves a hands-on approach to managing your portfolio. If you are a skilled investor and well-versed in market fluctuations, you may be able to capitalize on quick opportunities, or sell off a security before your portfolio takes a hit. It also means that when the market is down, your portfolio may be down with it.

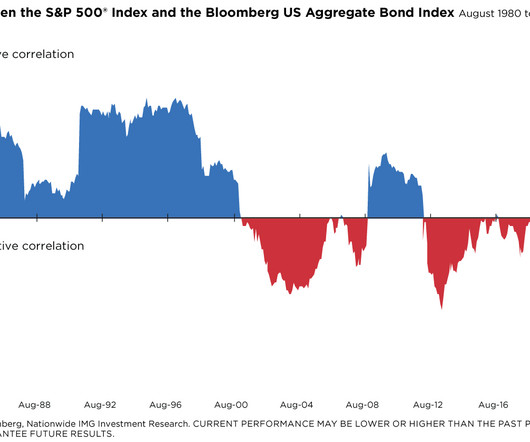

The positive correlation between stocks and bonds, especially in 2022, hurt investors in balanced portfolios such as the traditional 60/40 stock/bond blended models. If so, that would be a welcome development for investors counting on their balanced and diversified portfolios to keep them on track to their investment goals.

Given this survey looks at managers who manage actual portfolios, this is a very solid potential contrarian indicator. The language is very similar to what Powell used to say back in 2022 and 2023, when they were raising rates. A diversified portfolio does not assure a profit or protect against loss in a declining market.

We talk about this some but when you try to understand how well a holding has done or how well a portfolio has done, it is important to understand the track record. The Invenomic Fund (BIVIX) that we've looked at a few times is seriously skewed by two phenomenal years in 2021 and 2022 when it was up 61% and then 50%.

Let's play around with a couple of quadrant inspired portfolios. ARBIX was down 54 basis points in 2022 so it was not crushed like duration products. I included a little gold in the third portfolio because how can we have a discussion about quadrant-inspired portfolios and not include gold in there somewhere?

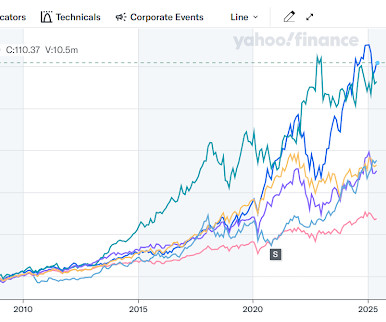

In 2022, it was up 104 basis points (total return). It is not intended to be a surrogate for a 60/40 portfolio, although it was close in 2024, and it clearly will not and is not intended to look like the US equity market. The correlation of the portfolio to the S&P 500 isn't that low at 0.64 The results were fascinating.

Heres why these six stocks are the portfolios biggest winners or losers for the quarter. 30, 2022, and April 8, 2025. Corporate earnings are likely to recover for three reasons. Instability in the Middle East will continue, and heres how it affects our investing. I sometimes use mapping when editing complex client documents.

I wish I’d owned a lot more given that it’s up 84% since 2022 while the global stock market is up 15% and aggregate bonds are down -3.5%. So, when the Dollar ripped 28% in 2021 and 2022 I figured it might be beneficial to hedge that exposure since I consume everything in Dollars. It’s down 22% from its 2022 highs.

A concentrated portfolio of deeply undervalued, high-quality companies that could be attractive to strategic buyers, private equity firms, or activist investors. After a tough stretch in 2022–2024, it is the top-performing Validea portfolio in 2025 YTD , up 25.7% The result? Notably: It soared in 2009 , returning 153.9%

The S&P 500 peaked on February 19, 2020 before the Covid bear market and then we had another bear market in 2022. Well, the word of the day in 2025 is diversify, as portfolios that have been diversified have held up quite well. A diversified portfolio does not assure a profit or protect against loss in a declining market.

There are a lot of opportunities to diversify portfolios so they arent as concentrated as the S&P 500. It was strong even in 2022 and 2023, which was another clue that a recession wasnt imminent. A diversified portfolio does not assure a profit or protect against loss in a declining market. Compliance Case # 7521978.1._011325_C

Investors looking for a diversified portfolio that performs well in all market conditions have long been drawn to the All Weather Portfolio, a strategy pioneered by Ray Dalio of Bridgewater Associates. The portfolio allocates across U.S. 2022 -19.5% -16.2% 2022 -19.5% -16.2% GLD SPDR Gold Shares 7.5% +380.3%

To help us unpack this and what it means for your portfolio, let’s bring in Matt Hougan. I think many of the skeptics don’t evaluate where the data is today because they’re taking a 2022 or 2018 or 2014 view of Bitcoin and crypto. I’m Barry Ritholtz. The firm runs over 10 billion in crypto assets.

When your portfolio leans too heavily in one direction, even a small downturn can lead to large losses. Take the year 2022, for example. Investors who concentrated their portfolios in tech saw their savings take a painful hit. Also, rebalance your portfolio regularly. The Dow Jones U.S. NASDAQ fell over 33%.

For purposes of this post, forget tracking SPY, think about equity plus volatility, realizing that at times the volatility will help the portfolios and that at times it will hurt the portfolio. The levered portfolio did slightly worse in 2022 but not catastrophically worse despite UPRO falling 56% and TYD falling 43%.

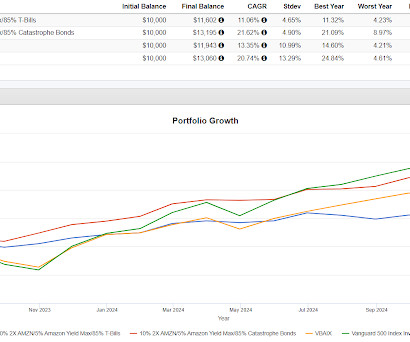

I would describe the paper as seeking how to use low volatility equities in various ways to replace some or all of a traditional 60% equities/40% bonds portfolio. All three portfolios outperform VBAIX which is a proxy for a 60/40 portfolio and they do so with lower volatility and better Sharpe Ratios.

Data from 12/31/2022 12/31/2024. 3 So, as investors, what can we do about it within our portfolios? At the end of 2024, these were the largest seven companies in the U.S. MSCI EAFE Index : Designed to measure non-U.S. developed market equity performance, excluding Canada. Source: Bloomberg, Avantis Investors.

This current bull market is nearly 26 months old and is now up more than 70% from the mid-October 2022 lows. It was strong even in 2022 and 2023, which was another clue that a recession wasnt imminent. A diversified portfolio does not assure a profit or protect against loss in a declining market.

Velina Peneva : I think that the, the clients understand that when you’re thinking about portfolio construction, you can have only so much allocation to a given geography redundancy to a different industry sector. And we need to have a portfolio that can cover liability. And if you look at our portfolio, we are 85% fixed income.

As Will points out, studies have shown that people feel losses in their portfolio twice as much as they feel the gain. There’s also recency bias at play: The market downturns of 2022 and the COVID-19 shock in 2020 linger in memory, making us forget the equally compelling history of market recoveries and long-term growth.

The idea is that you get the full beta (stocks and bonds) return with just a portion of the portfolio often with futures or some other form of leverage, leaving dollars left over to add alternatives all in pursuit of better nominal returns or better risk adjusted returns. The fourth portfolio more closely aligns with what we do here.

Bonds with duration are now more volatile than they used to be and that volatility is less reliable than it used to be making them a less effective diversifier for the equity portion of a diversified portfolio. Where Portfolio 3 should zero out, it's pretty close to doing just that.

That's an important question and issue for any holding in your portfolio. The first grouping of funds were intended replacements for 60/40 due to the "limitations" that the current environment poses for the basic portfolio. QAISX outperformed VBAIX by a good bit in every year except 2022. The fund is the same age as BLNDX.

This is why having a globally diversified portfolio can benefit US-centric investors, as the US won’t always lead. Current levels are similar to what we saw in mid-2022, when recession risks were elevated but the economy never plunged into an actual recession.

We spend a lot of time here on how to diversify to try to smooth out the ride and how to hold up better when markets have a year like 2022 or 2008. This brings us to the heart of today's post about trying to build a set but don't completely forget portfolio. For us, that includes alternatives.

at the start of 2022, given an average inflation rate of 7.5% at the start of 2022, given an average inflation rate of 7.5% To stay ahead, you need: A well-diversified portfolio including equities, linkers, real assets, gold. Banks may lower FD rates; even T-bills and sovereign bonds will yield less. over that period.

Lingering pandemic fatigue and inflation spiking to its highest level in over 40 years in mid-2022 significantly dampened economic sentiment. According to United Nations data, the old-age to working-age dependency ration in the US in 2022 was 29.4 For comparison, the dependency ratio in 2022 was 38.0 in Germany and 55.4

Many noted how the 2022 midterms came in much closer to expectations and that maybe this time so would the presidential election, but this is yet another election involving President Trump that saw his eventual numbers come in better than expected, similar to 2016 and 2020.

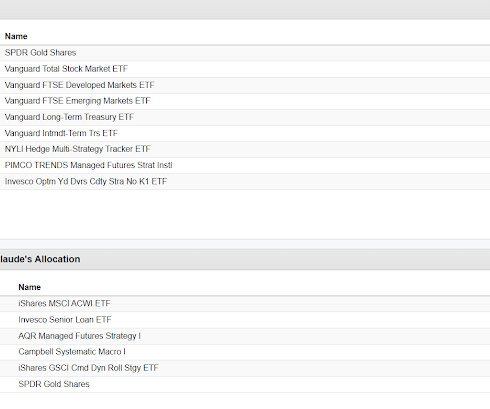

The article was thin but there was a reference to his "holy grail" of 10-15 uncorrelated assets in portfolio construction. We've looked at this a couple of times, it is interesting of course and actually having 10-15 uncorrelated assets in a portfolio would hit the mark for diversifying your diversifiers.

Interest rates going up doesn't worry me from a portfolio perspective, I pretty much don't have any interest rate risk in the portfolio. My first thought is to think about the all-weather attributes of Permanent Portfolio-inspired, quadrant investing. Portfolio 3 is sort of close to what we blog about regularly.

Consumer discretionary is another one that pretty reliably outperforms for ten year periods, not the last couple though after getting whacked pretty hard in 2022 though. As you might expect, staples went down much less in the Financial Crisis as well as in 2022. Tech is a very good bet to regularly outperform the S&P 500.

First I asked it to suggest an all-weather portfolio that included managed futures. As we often see, a decent portfolio strategy this time from AI that can be improved upon. Both exchange portfolios held up much better in 2022. I played around a little bit with Claude AI from Anthropic. What about NZX Limited?

The purple line went through a nasty drop in 2022. There are countless, valid approaches to portfolio management but if you pick the right stock or niche, the fundamentals don't unravel and it continues to do what you'd expect it to do, why would you get out of the position? That can serve as a great stabilizer in a portfolio.

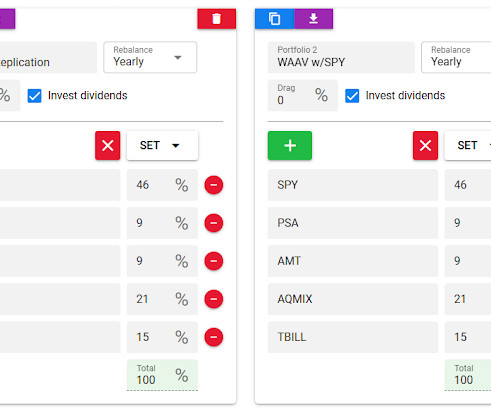

WAAV seems Permanent Portfolio inspired which is why I threw in AQRIX and PRPFX along with VBAIX as a proxy for a 60/40 portfolio makes sense as a benchmark. Both the ACWI and SPY versions outperformed AQRIX which is sort of a risk parity fund and PRPFX which is the Permanent Portfolio. The results are a mixed bag.

I would say, and I think he was on a similar page, that in a diversified portfolio that goes narrower than a very broad based index fund will probably have a couple of "good" dividend stocks in it. Going from memory, Amazon dropped 90% in the tech bubble, 75 or 80% in the Financial Crisis and in 2022 it dropped 49%.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content