This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Inflation is vanquished, the economy makes a soft landing, rainbows and sprinkles and unicorns! Parts of the economy suffer – notably residential real estate, new job creation, and consumer spending. Not So Fast (April 3, 2020). My take on these probabilities looks something like this: 1. The Fed gets it precisely right : Yay!

After a monstrous 68% recovery from the March 2020 pandemic low, and another nearly 30% gain in 2021, markets decided to have one of their all-too-regular spasms. are fast-growing, highly profitable key players in the modern economy. Blame whatever you want – Too far, too fast? End of ZIRP? Too rapid rate increases? –

.’s expansion, its potential future growth, and its sustainability, and whether the valuations are justified. The sector is rapidly emerging as a driving force in the country’s economy. Financial Overview Of Trent Financial Year Mar 2020 Mar 2021 Mar 2022 Mar 2023 Mar 2024 Revenue (Crores) 3,485.00

Markets How major asset classes performed in October 2020. capitalspectator.com) Don't be surprised to see the stock market rally before the economy bottoms out. every.to) Q3 saw big drops in startup valuations. klementoninvesting.substack.com) Economy The Fed is most hurting the middle class through rising rates.

Markets Market valuations are a lot more attractive than they were a year ago. interest rates since 2020. finance.yahoo.com) Economy Auto loan delinquencies are on the rise. blog.validea.com) Visualizing U.S. visualcapitalist.com) Strategy The hardest part of investing is holding through tough times.

The 2020 and 2021 inflation was the tsunami. And the earthquake was the irrational boom that occurred in 2020/21. As irrational exuberance took hold of the markets we saw a huge surge in the valuations of private equity firms. You don’t have to pick just one. And that’s what makes the boom so interesting.

It all added up to the third most volatile market in 25 years. And while the economy isn’t going to just turn on a dime and recover overnight, there is hope for a better second half of the year. Valuations Could Move to a More Normal Range . The first half of the year proved challenging for even the most hardened of investors.

The Chinese market has struggled since 2020 due to COVID-19, real estate issues, and tech company crackdowns. Additionally, foreign investors are shifting funds from India to China, attracted by lower valuations. These valuations reflect different economic conditions and investor sentiments in each country.

million, the lowest level since May 2020 [Figure 1]. The National Association of Home Builders (NAHB) index, another important housing metric, fell in August to below 50 for the first time since May 2020. Traffic of prospective buyers, a leading indicator of future sales, also fell to its lowest since May 2020. Conclusion.

economy continues to look solid, with markets rallying Friday after a stronger-than-expected jobs report. Pockets of attractive valuations exist despite above-average valuations in some high-profile areas of the market. economy, and the job market is leading the way. Payroll growth picked up in recent months.

We believe the odds of a recession remain low, with continued income growth, a recovery in rate-sensitive cyclical areas of the economy, and untapped potential for productivity gains helping to support the expansion. Market participants, strategists, policymakers, and the economy rarely saw eye to eye. We continue to favor the U.S.,

Financial Highlights Of NSE IPO Financial Year Mar 2020 Mar 2021 Mar 2022 Mar 2023 Mar 2024 Revenue (Crores) 3,508 5,625 8,929 11,856 14,780 Net Profit (Crores) 1885 3573 5198 7356 8306 EBITDA(Crores) 2,706 4690.98 Its revenue surged from ₹3,508 crore in March 2020 to ₹14,780 crore in March 2024. in March 2020 to ₹167.79

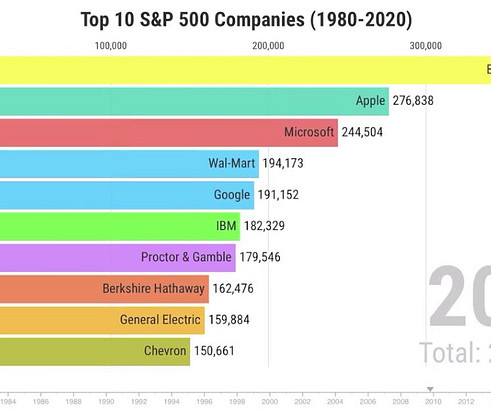

These recurring shifts in the composition of the benchmark stock Index can offer insight into how different factors, such as cyclicality, long-term growth potential, and valuation, may impact stock performance in the future. The outsized influence of tech company earnings on the S&P 500 is important to understand.

You can watch how those changes occur, from 1980-2020, below. IBM’s return was fueled by growing earnings, growing dividends, and buying back stock at cheap valuations. The 2020 top ten list is very tech heavy. The broader economy matters. I started driving in 1972. Gasoline was $0.36 per gallon. Often a lot.

No matter what metric you looked at, the peak valuations for growth stocks in mid-2021 were extreme. This is a chart of the valuation of the most expensive decile of our investable universe using the Price/Sales ratio. But even after that decline, the overall valuation remains about 30% above its average for the full period.

Successful businesses and the economy both rely on the movement of people. In light of the COVID lockdown and resulting slowdown in the economy, we have begun to observe a recovery in business, and this growth is reflected in the price of its shares. 2020-21 1,988.19 -123.54 2020-21 0.35 -5.23 Financial Year Revenue (Cr.)

at year-end can largely explain the compression in valuation, especially for higher multiple equities, primarily during the first half of the year. COVID-19 January 2020 May 2020 -20.3% 3/23/2020 5/31/2020 101 36.1% at the beginning of the year to 16.6x by year-end. The rise in the 10-year Treasury yield from 1.5%

Perhaps the market’s biggest fear has been that the Fed may overdo its tightening to fight inflation and send the economy into a painful recession, break something, or both. He acknowledged that the economy is slowing (which is what the Fed wants) and that the full effect of the rate hikes had not yet been felt. Of course, the U.S.

Strong Job Numbers Are Good News for the Economy and Markets There’s been valid concern that employment conditions are deteriorating, ever so slowly. If you combine wage growth with employment growth and hours worked, we get a sense of aggregate income growth across all workers in the economy. in April 2023 to 4.3% in 2019, 5.9%

Stock prices have been dropping recently because of lower valuations driven by rising rates and Wall Street is still forecasting solid profit growth in 2023. But the divergence could also be the result of “recession prep,” where the risk to future growth is causing lower valuations, the article posits.

It’s the same with a nation’s economy! This not only benefits the businesses themselves but also ripples through the entire economy, fostering progress and development. Years Amount (in crores) 2020 170260.39 The primary valuation concern was that Indian stocks run ahead of fundamentals, leading to high valuations.

We learned everything, you know, across from accounting to auditing to, to tax and valuation. I ended up in what was called the valuation services group, where we valued real estate and businesses either for transactions or for m and a activity. You know, in those days these companies hired, you know, crops of undergrads.

Particulars/ Financial Year 2019 2020 2021 2022 2023 CAGR (4 Years) KPIT Technologies - Revenue (Cr) 641.26 Elxsi has an upper hand in NPM as well and in comparison with KPIT, the margins of both companies can tend to slow down due to a slowdown in the global economy. KPIT and Elxsi have Net Profit Margins (NPM) of 11.5%

For a broad view of our expectations for the economy, stocks, and bonds in 2024, download our 2024 Market Outlook. That bear eventually ended in October 2022, and since then stocks have defied many experts, who continually (and incorrectly) touted a weakening economy, tapped-out consumer, and many other reasons to doubt the new bull market.

Articles If private equity suffers, the blow will reverberate throughout the entire economy By Bethany McLean No one runs a business on the assumption that that business won’t be there tomorrow By Tim Duy The government made more than $13 billion from its bailout of Citigroup, $5 billion on its stake in AIG, $4.5

The size of the global solar EPC market exceeded USD 215 billion in 2022, and it is anticipated to grow at a rate of 6.9%+ CAGR from 2023 to 2032, prompted by the increasingly stringent sustainable development goals across many major economies. 2020 ₹83.48 ₹2.20 But what is not so good about the Company are its valuations.

That was a 125% gain in a matter of 19 months following the Covid-led pandemic crash of 2020. Market pundits are fearing macroeconomic disasters with fears of the US economy going into recession. Russia invaded Ukraine in February throwing the global economy into commodity and energy crises. High Valuations.

in Q4 ), generationally low unemployment (3.5%), and relatively stable earnings (see chart below) all point to a stable economy with the ability to navigate a soft landing. China’s new reopening of the economy and Europe’s seeming ability of dodging a recession provide additional evidence for a soft landing scenario.

Overall, the economy is well-positioned to continue recovering from pandemic lockdowns, but inflation risks, as well as labor challenges and production capacity, are eating into productivity. Equity markets were positive this week as investors continue to assess the state of the global economy. Chart of the Week. Market Update.

As I pointed out last month, we are coming off a heroic advance over the last three years (2019/2020/2021) with the S&P 500 soaring +90%. The Fed’s goal is to increase the cost of borrowing, thereby slowing down the economy and reducing inflation. over the next couple of years. If Things Are So Bad, Why Are Prices Going Up?

With valuations still high, the threat of a recession still looms over the economy, ushering in a prolonged period of low returns across the market, from stocks and real estate to corporate profits, as well as elevated inflation and unemployment rates. government debt which now has a solid return thanks to the inverted yield curve.

economy is in or about to enter recession, so we thought a piece on what a recession might mean for the stock market would be of interest. economy is not currently in recession, odds are still perhaps a coin flip or better that one may come in the next year. While Friday’s strong jobs report provides more evidence that the U.S.

Remember that global pandemic back in 2020 called COVID-19 that killed over 350,000 people in the U.S.? most recently) and the economy went into recession with GDP (Gross Domestic Product) declining by -2.2%. What did the stock market actually do in 2020? On the flip side, during 2022, the economy was firing on all cylinders.

The S&P 500 Index enjoyed its best month since November 2020 and its best July in over 80 years. economy contracted for the second straight quarter. With a strong, even if slowing, job market and resilient consumer spending, we believe not enough sectors of the economy are contracting to qualify as an official recession.

The S&P 500 Index enjoyed its best month since November 2020 and its best July in over 80 years. economy contracted for the second straight quarter. With a strong, even if slowing, job market and resilient consumer spending, we believe not enough sectors of the economy are contracting to qualify as an official recession.

But in reality the economy doesn’t look so much like a “cycle” It looks more like a line from the bottom left to the top right with occasional shocks that create the illusion of a regular cycle. In other words, the persistent price boom of the 2020/21 period is slowly morphing into a more persistent price bust.

million in 2020, and it is expected to reach & 12,700.8 2020 0 6,555.40 appears to be a fundamentally strong company with consistent revenue and growth, healthy profitability, and a reasonable valuation. The tractor industry in India has grown at a compound annual growth rate (CAGR) of 10% during the last four decades.

After the subprime crisis in 2008, many developed countries’ Central Banks started printing money and flooding the global economies with cheap liquidity. The liquidity support since 2008 and massive stimulus post March 2020 has inflated all the asset prices be it equity, debt, or real estate. trillion to ~$8-8.5

Uncertainties in different parts of the world have caused the global economy to slow down. 2020-21 152.46 2020-21 0 32.21 Revenues and profits are increasing at the growth stage, and the high P/E commanding the current valuations will be justified by the company’s growth rate. 2021-22 200.44 2019-20 148.63

The Middle-Class section is the driving force behind the economy and politics, and it is influential in understanding consumer patterns. crore in FY22 on account of the higher fair valuation gain on investments in debt mutual funds. 2020-21 ₹ 70,372 ₹ 4,389.1 Other income has increased to Rs. crore in FY23 from Rs. 2019-20 0 53.04

stock market has been winning by a large margin (2019: +29%, 2020: +16%, 2021: +27%) and a significant contributor to the team’s win streak has been the Federal Reserve, or the designated hitter (DH). The majority of economists, strategists, and talking heads on television are forecasting a recession in our economy, either this year or next.

Two weeks ago, I wrote an article where I looked at the valuation of the median stock and how it has changed over time. 12/31/2020 12.4% 12/31/2020 58.7% And with intangible assets rising in the economy, standard earnings calculations are becoming less and less accurate. By Jack Forehand, CFA, CFP® ( @practicalquant ) —.

So far, this year hasn’t seen a full-blown crisis like 2008–2009 or 2020, but the ride has been very bumpy. Lower inflation tends to bring higher valuations (Fig.1). can eke out some economic growth in the second half as inflation falls and recession fears subside, we would expect valuations to get a nice lift by year-end.

For both companies and governments, this provides incredible economic and infrastructure opportunities, but also exposes massive risks to security and privacy.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content