This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Between 2014 and 2024, Mason transferred client funds into his own accounts and those of the two entities without clients’ authorization, according to the SEC. Mason, who ran Rubicon Wealth Management, a registered investment advisor in Gladwyne, Pa., He pleaded guilty to all of the criminal charges.

Alex Ortolani , Senior Reporter , WealthManagement.com July 15, 2025 3 Min Read Cory Nakamura, chief investment strategist at Mosaic Pacific Creative Planning Adds $430M Hawaii-based RIA Creative Planning, the mega-registered investment advisor based in Overland Park, Kan. ,

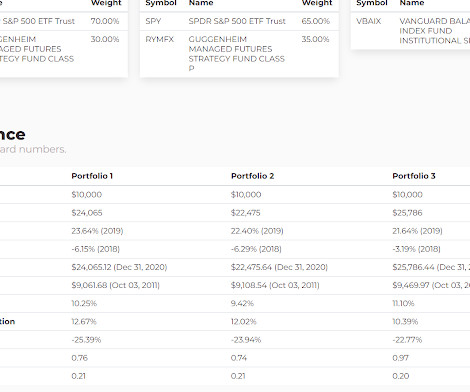

Plenty of other managed futures funds came onto the scene in 2013 and 2014 but I think RYMFX is the only one to test what was a terrible time for managed futures. To my knowledge, RYMFX was the first managed futures mutual fund and it had the space to itself for several years after in launched in 2007.

EBSIX' worst 12 month stretch was a decline of 13% from June 2013 to June 2014. There is no reason anyone trying to implement some variation of this needs to put such a huge weighting into just one fund, EBSIX in this case, for the macro component. While that is not a catastrophic number, it's a visible risk that seems easy to mitigate.

According to Fidelity an average couple both aged 65 will spend $300,000 on medical costs in retirement. This is up from $285,000 in 2019, from $275,000 in 2017 and from $220,000 in 2014. This is a significant amount even for retirees with a retirement nest egg in excess of $1 million. High deductible health insurance plans .

As we say all the time, whereas stocks are the thing that goes up the most, most of the time in the modern era I would want more than 25% in equities for anyone needing normal stock market growth for their retirementplan to work. ASFYX is a client and personal holding.

annualized return, and has been closed since 2014. And at larger fund companies, routes through advisory and retirement-plan pathways are usually left open, like the Fidelity Growth Company which has officially been closed since 2006 but allows new investors through those channels. return over the last 5 years.

ABLE accounts were created with the passage of the ABLE Act in 2014 and are intended to provide individuals with disabilities a way to save funds without jeopardizing their eligibility for government benefits such as Medicaid and Supplemental Security Income (SSI).

In 2014, an 87-year-old, retired specialty-glass importer faced more than $2 million in penalties for failing to disclose a $7 million Swiss account which dated back to the 1960s. military banking facilities; certain bank-to-bank settlements; accounts owned by certain retirementplans. In 2022, a professor with dual U.S.

He notes " after three strong returns in its first three years (2014-16) came a string of losses. It is an unusual exposure, I am not aware of any other funds that are just reinsurance but if you know otherwise please comment. SRRIX lost -11.35% in 2017, -6.14% in 2018 and -4.47% in 2019."

Since 2014, the S&P 500 has almost tripled so 50-100% for the equity portion of a diversified portfolio is not insanely unrealistic. But what retirementplan doesn't need some level of resilience in the face of some sort of adverse market sequence?

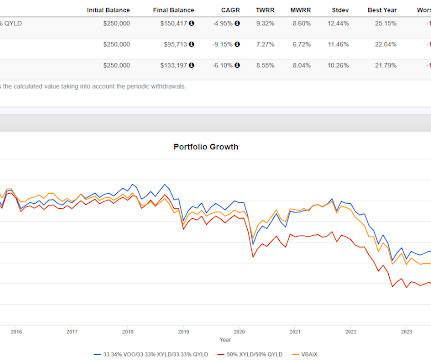

If they can put their previous mortgage payment, lets go with $1500/mo, into a 60/40 fund, they would end up with $415,000 including the $50,000 they started with based on June, 2014-June 2024 results for the Vanguard Balanced Index Fund (VBAIX) or they'd have $500,000 if they put 80% into stocks.

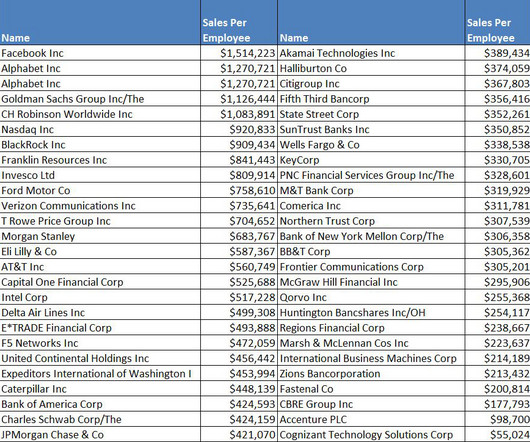

Steel had $3,340 in revenue per employee, which is $90,000 in 2014 dollars. With millions of Americans shoveling money into their retirementplans every month, there is a much greater demand for stocks than their was in the first half of the twentieth century. Today, 175 S&P 500 companies have more revenue than $15.1

It backtests to 2014. A lot of sophisticated and expensive funds that blend together for an interesting result, it's somewhat all weather but compounds better than many all weather-ish funds tend to do. I think the names are self explanatory, two of which I'd never heard of.

The first one was writing for TheStreet.com from 2005 to early 2014. A few months ago I tried to submit something to them to see what the process would be like and the feed back was essentially to make it more actionable which I took as what stocks should people buy. I did not try to resubmit it after that.

The Isolas are currently on a crusade to fix the atrocities that take place in teacher's retirementplans. They did such a good job for their clients that by 2014, the business had grown too big and Tony would no longer be able to work in the school. Tony taught U.S.

Would you be ok in a year like 2014 when ANNPX was only up about half of what the S&P 500 was up or 2021 where the disparity was much greater? If you think of this as an alt, then anything you might ever do in this space needs to be sized properly.

We bought our current cabin in 2012 and sold the first one in 2014. In 2001 I got laid off from Schwab, sold our house in Scottsdale while I went to work at Fisher Investments for most of 2002, keeping our cabin in Walker which we moved into full time late that year and have been living in Walker ever since.

QLACs came about in 2014. The comments have plenty of naysayers on QLACs, they are worth reading. I'll stipulate every negative point about annuities. I've long said that many people I've known who have had annuities love them, warts and all. Basically, you can take the lesser of either 25% or $200,000 from an IRA account to buy a QLAC.

The Global X S&P 500 Covered Call ETF (XYLD) has been around since 2014 and while it has lagged the plain vanilla S&P 500 badly, its annualized total return is still 5.78%. Where ISPY is selling covered calls, then a blowup seems unlikely, lagging by a lot seems like the bigger risk.

The partial year of 2014, only quality, the green bar, was close to market cap weighted. While the there is differentiation in performance, less so with quality, there doesn't appear to be reliable crisis alpha with these. That is important for setting expectations.

In 2014, an 87-year-old, retired specialty-glass importer faced more than $2 million in penalties for failing to disclose a $7 million Swiss account which dated back to the 1960s. military banking facilities; certain bank-to-bank settlements; accounts owned by certain retirementplans. In 2022, a professor with dual U.S.

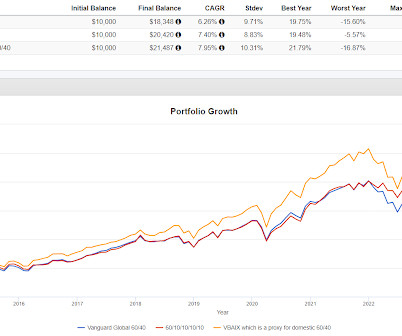

Back in July 2014, when our backtest started, the ten year US Treasury yield was hovering between 2.40% and 2.60%. Additionally, foreign equities have lagged domestic for many years and 60/10/10/10/10 obviously had much less exposure to domestic than VBAIX. What 60/10/10/10/10 did was avoid obvious interest rate risk.

The highest federal marginal tax bracket in 2015 is 39.6% (as it was in 2014). To reduce your AGI, you might consider looking into postponing income from retirementplan distributions, capital gains and even employer bonuses-from one year to another in order to manage the amount of AGI realized in any given year.

But the Bureau of Labor data shows that something else has also occurred over the last four decades: People lost their pensions (defined benefit plans) and were forced into defined contribution plans, usually in the form of 401(k)s. Conversely, workers who only have 401(k)s or defined contribution plans, rose from 9 to 34%.

It has to be such a different set, the retirementplanning is different, the safety net is different. RITHOLTZ: So you joined Global X in 2014. I joined Global X in 2014, and we have, if I remember correctly, approximately $1.5 So a phenomenal learning experience with both Jefferies and Morgan Stanley. BERRUGA: Yeah.

A white paper entitled " Active Alpha ," published by Brown Advisory in 2014, highlights several factors, including: Independent thinking: Studies have shown that managers whose portfolios differ significantly from their benchmarks are more likely to outperform.

A white paper entitled " Active Alpha ," published by Brown Advisory in 2014, highlights several factors, including: Independent thinking: Studies have shown that managers whose portfolios differ significantly from their benchmarks are more likely to outperform.

A good example of this is Warren Buffet, who still lives in the home he bought in 1958 and drives a 2014 Cadillac XTS. Ad Make your retirementplan work for you by investing in a Roth IRA. Roth IRAs allow you to save money for retirement, while providing the flexibility that traditional retirementplans lack.

according to Siegel (2014). And they’re the things that can blow up a retirementplan if you don’t make conservative estimates that properly account for them. The worst narrative in finance is this idea that stocks generate 10%+. The reality is that stocks have averaged about 4.4% according to Dimson (2020) or 6.6%

Wetzel moved into the Glen Saint Andrew Living Community, a senior residential facility in Niles, Illinois, in 2014 after her partner of 30 years died of cancer. One recent example of the type of discrimination that LGBTQ+ seniors fear as they age is the story of Marsha Wetzel.

So for example, researchers look at the median income of the middle quintile in 1975 and compare that to the median income of the median quintile in 2014, say. Instead, they rely on a snapshot at two points in time. When they find little or no change, they conclude that the average American is making no progress.

I did sorted weekly tweets from 2012 to 2014, then I stopped tweeting as much for a while, and so discontinued them. Part of Spending Bill, Changes RetirementPlanning [link] Marginal ideas at best Dec 27, 2022 Going Boldly: The Retirement Savings for Americans Act 2022 [link] This will do less good than most imagine.

Ed Slott Reason to Follow: Americas IRA expert with unparalleled expertise With almost 50 years in the industry, Ed Slott is widely regarded as the leading expert on IRAs and retirementplanning. His workshops, PBS specials, and books help financial professionals master tax-efficient strategies for their clients. Find him on LinkedIn.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content