This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

(capitalspectator.com) The credit markets are very different than they were in 2009. institutionalinvestor.com) Putting a valuation on Instacart ($CART). semafor.com) A wide range of outcomes is always on the table. tonyisola.com) Leveraged loans have put corporate bonds to shame in 2023.

With the S&P 500 now close to 20% off its highs, I thought now might be a good time to look to our market valuation tool to see where things stand. But before I do that, I wanted to first cover two caveats I always put in articles about market valuation. With that all being said, let’s look at the current valuation data.

Bernstein explains the four drivers of their models: Profits, Liquidity, Sentiment, and Valuation. We discuss the challenges of launching a Quantitative Macro focused firm right into the teeth of the Great Financial Crisis in 2009. As frightening as that era was, it turned out to be a wonderful time to launch an asset management firm.

By using the PEG ratio, Lynch sought to identify stocks that were not only growing quickly but also trading at valuations that made sense relative to that growth. Top 3 Best-Performing Years: 2009 : +62.3% (vs. cumulative return , outperforming the S&P 500 by 667.4%. S&P 500 +23.5%) 2013 : +47.6% (vs. 29.6%) 2021 : +34.3% (vs.

In February 2009, I wrote “ 8 Reasons For A Bull Market. Psychology in markets is always fascinating. ” While in hindsight, it is easy to see that was the right call, overall, psychology was highly negative at the time.

Even with bear markets like 2000-2002 and 2008-2009, the portfolio had strong returns for a very long period. While some of that outperformance was due to improving fundamentals and earnings, most of it the returns came from the valuation investors assigned to these stocks. Source: [link].

Private Credit Outshines Many High-Valuation Stocks, Bonds. With interest rates at record lows and many publicly traded bonds and stocks approaching historically high valuations, private credit has become increasingly attractive to investors because of its total return prospects, steady income and role in diversification.

Based on the present combination of extreme valuations, unfavorable and deteriorating market internals, and a rare preponderance of warning syndromes in weekly and now daily data, my impression is that the speculative market advance since 2009 ended last week. I may as well just say it.

By Justin Carbonneau ( Twitter | LinkedIn | YouTube ) — Over the past few weeks, I’ve seen a number of charts highlighting the opportunity in small-cap stocks given their absolute and relative valuations. The chart below, also from our market valuation tool, compares small cap value to large cap growth stocks. Only 12.4%

We learned everything, you know, across from accounting to auditing to, to tax and valuation. I ended up in what was called the valuation services group, where we valued real estate and businesses either for transactions or for m and a activity. 00:14:50 [Speaker Changed] Yeah, it was about the middle of 2009.

The ten-year period between 2000 and 2009 is often called a “lost decade” for U.S. From January 2000 through December 2009, the S&P 500 lost 0.72 IBM’s return was fueled by growing earnings, growing dividends, and buying back stock at cheap valuations. percent per annum, including dividends.

at year-end can largely explain the compression in valuation, especially for higher multiple equities, primarily during the first half of the year. Great Financial Crisis October 2007 April 2009 -39.0% 3/9/2009 4/30/2009 69 29.0% at the beginning of the year to 16.6x by year-end. to nearly 3.9% 9/21/2001 12/31/2001 52 18.9%

Amid all the noise surrounding geopolitical issues, global valuations, and FII selloff, the Nifty bulls might be feeling a bit clueless about their next moves. The best month for Nifty50 returns was in May 2009, with an impressive 28.07%, and October 2007 was also remarkable, with a 17.51% gain. loss, due to the financial crisis.

One other factor at play are valuations. Did high valuations add fuel to sellers' fire? I tend to think that valuations don't matter during panic selling. Whatever the outcome, this period in time will be studied and dissected for as long as markets exist. It's impossible to say with any certainty, but I don't think so.

As we delve into the intricate details of Azad Engineering Limited, we’ll investigate whether this seemingly high valuation aligns with the company’s underlying business prospects. million units between Fiscal 2009 to Fiscal 2023 at an overall level. It has also manufactured and delivered 3.09

Between 2000 – 2009, the cumulative total return for the S&P 500 was negative 9.1% From 2000 to the end of 2009, the global allocation would have outperformed by nearly 8.8% Valuations. Valuations outside of the United States have been much cheaper to the long-run averages for quite some time. vs positive 30.7%

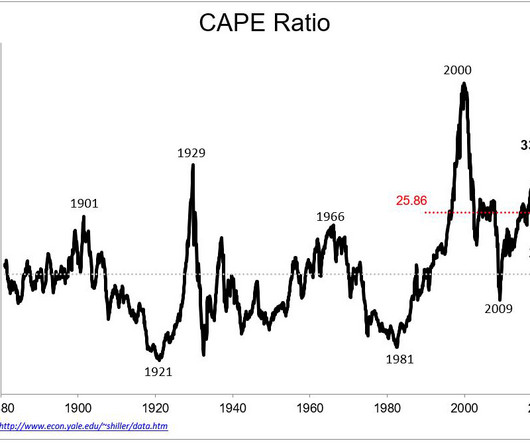

The two other markets that saw such lofty valuations were 1929 and 2000. To be very clear, at that time, I was in the "lower your return expectations camp" due to a combination of recent performance and high valuations. Over the last 30 years, 1990 and 2009 were the only times the CAPE was below it.

Over the next 12 months, the S&P 500 dropped 45%, the Fed slashed rates down to next-to-nothing, and valuations evened out while bond yields plunged. After stocks bottomed, their premium climbed to 7 points above Treasurys by March 2009, ushering in a new bull market. near the current level. Now, some measures peg U.S.

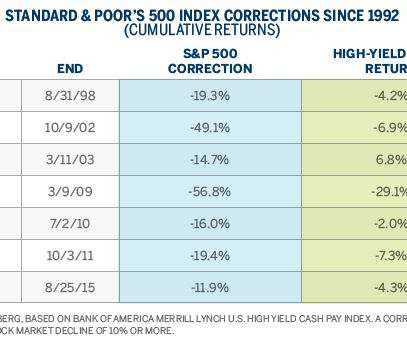

The S&P 500 has only posted one year of negative returns greater than 1% since 2009. This helps to illustrate the fact that market corrections are common over most periods of time and should be viewed as the market resetting stock valuations back to a more fundamental level.

The yield on the ten year Treasury note briefly passed 5% recently, the highest yield on the ten year note since before the financial crisis of 2007 – 2009. if you use a forward earnings yield, or ~5% if you use a trailing earnings yield.

The funds did well in the Financial Crisis and they did well in 2022 but from 2009 onward, one of his two long standing funds has a negative annual growth rate and the one with a positive growth rate was less than 1/3 of a plain vanilla 60/40 portfolio.

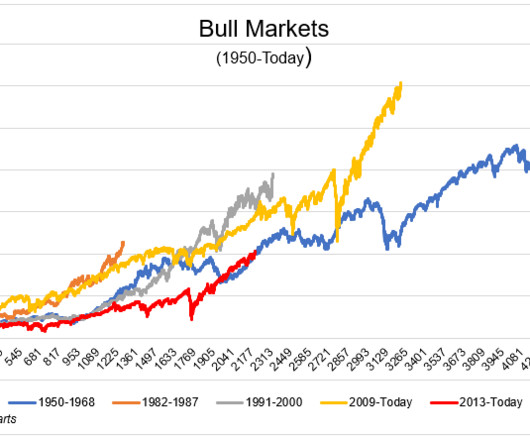

Whether you measure it from the low in 2009 or when new highs were made in 2013, isn't this just semantics? Bull markets are in the eye of the beholder, and when we mark the beginning is of little importance, unlike things like earnings and valuation and interest rates. The Netflix of fitness has a $4 billion valuation.

It's October 2009. The source of stock returns can be broken down simply into three main buckets: Dividends, earnings growth, and the change in valuations. You've been putting money into your 401(k) for almost ten years. 118 months to be exact. The amount of money in your account is less than the contributions you've made.

With the length of this current run (however you measure it), and more importantly, with rich valuations, it's hard to go a few hours without seeing a headline that a "rug pull" is imminent. Remember all the black swan funds that were launched in 2009? On the early side, for example, are those who have argued that U.S.

We're in uncharted territory if we started the bull run from the bottom in March 2009. I mean, given recent returns and where valuations and interest rates are, things can't possibly get any better, can they? And what if we measured from the bottom in 2009? Fair enough, as I said, this is subjective. But my blog, my charts*.

Two weeks ago, I wrote an article where I looked at the valuation of the median stock and how it has changed over time. 12/31/2009 4.9% 12/31/2009 29.6% By Jack Forehand, CFA, CFP® ( @practicalquant ) —. Year End Date Negative Earner Percentage 12/30/2005 1.1% 12/29/2006 1.2% 12/31/2007 1.0% 12/31/2008 2.1% 12/31/2010 1.4%

Almost exactly five years ago, we wrote a piece entitled Bubbles, which discussed the sharp rally in stocks from the lows of early 2009 and the risks of the growing federal deficit that resulted from government bail-outs and fiscal stimulus during the financial crisis. Investment Perspectives | Bubbles II. Wed, 04/01/2015 - 16:48.

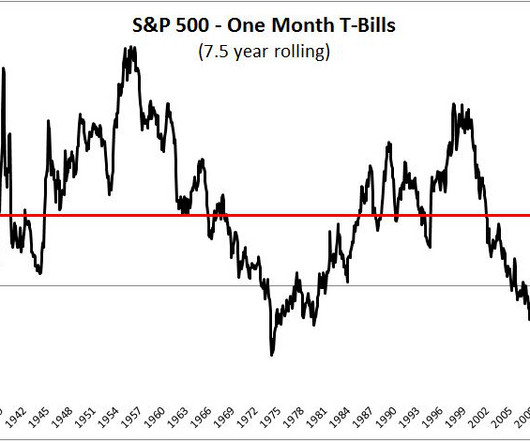

This range is determined by a number of factors, including but not limited to the business cycle, valuations, interest rates, inflation, and the collective mood of millions of investors. They're not wrong, since the bottom in 2009, stocks have outperformed risk free bills by 17.5% a year, the largest spread over a 7.5

I could maybe flip that around a little bit since I think particularly post 2008, 2009, the quality style of investing has become a lot more popular. You really like the long time where you have to hold to make up that valuation whole is so long that you just really shouldn’t be involved. 00:18:41 [Speaker Changed] Yep.

Smart investors are very careful about market valuations (prices) and investor behaviour. The chart below illustrates that the smart money enters when valuations are low and the majority of the investors aren’t looking at that asset class or security. For common investors, arriving at a fair value of any stock could be very tricky.

So far, this year hasn’t seen a full-blown crisis like 2008–2009 or 2020, but the ride has been very bumpy. Lower inflation tends to bring higher valuations (Fig.1). can eke out some economic growth in the second half as inflation falls and recession fears subside, we would expect valuations to get a nice lift by year-end.

ILMANEN: It’s always good to think of starting yields and valuation sort of two sides of the same coin. But in conclusions, I did put there that it just seems that stars are aligning for some fast pain and it wasn’t just high valuations but there was a catalyst. Explain that. Bonds are the most expensive. Stocks are pricey.

Investor enthusiasm, coupled with high valuations, has preceded all major market bubbles. stocks are based on traditional valuation metrics, via Michael Cembalest. In the decade since 2009, there have been regular claims that we were back in a bubble, but the FCF yield suggested valuation was not stretched.

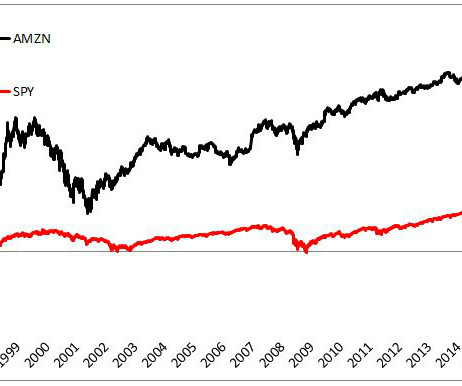

Amazon's stock has received a lot of attention over the years because its performance has been off the charts while maintaining a nosebleed valuation that has been the envy of their competition. Even if Bezos were to capture 100% of the total retail revenue, its price-to-earnings ratio would still be 63!

The yield on the ten year Treasury note briefly passed 5% recently, the highest yield on the ten year note since before the financial crisis of 2007 – 2009. if you use a forward earnings yield, or ~5% if you use a trailing earnings yield.

During the worst of the Financial Crisis (Q3 2008 through Q1 2009), more than 50% of S&P 500 companies hit their earnings targets each quarter. But overall, we would expect modest estimate cuts to be received positively by markets, supported by lower valuations and depressed investor sentiment. Quincy Krosby , Ph.D.

1 Also, from fiscal year 2009 until fiscal year 2016, federal agencies cut annual grants to private and public organizations by 3.4% For example, we found opportunity in small-cap stocks during their 2016 rally because of their relatively low valuations and limited vulnerability to flagging global economic growth.

as featured in the book, “Valuation: Measuring and Managing the Value of Companies, University Edition." Beyond that indicator, the managers look for companies with three other qualities: solid fundamentals, strong leadership and reasonable valuations. In our view, this decline presented a great valuation opportunity.

as featured in the book, “Valuation: Measuring and Managing the Value of Companies, University Edition." Beyond that indicator, the managers look for companies with three other qualities: solid fundamentals, strong leadership and reasonable valuations. In our view, this decline presented a great valuation opportunity. .

Over the last 25 years, we have seen four bear markets (1999-2002, 2008-2009, 2020, 2022) and numerous market corrections (10% losses). Valuation Concerns: Some technology stocks have high valuations, which means you could be buying at a high price, increasing the risk of a correction.

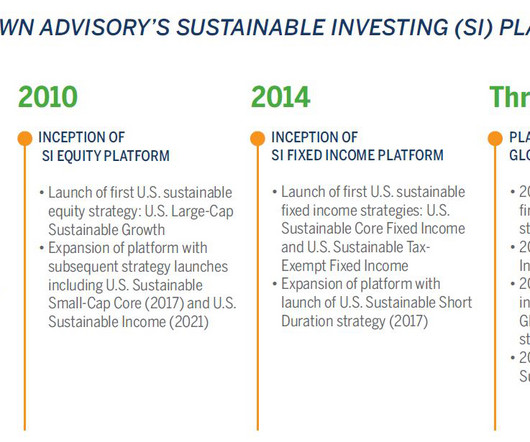

Despite the changing expectations and regulations in this investing arena, we have not altered our sustainable investing (SI) process since our strategy’s inception, and we remain committed to the same investment principles that have guided us since 2009.

Despite the changing expectations and regulations in this investing arena, we have not altered our sustainable investing (SI) process since our strategy’s inception, and we remain committed to the same investment principles that have guided us since 2009.

In 2015, though, three trends began to weigh on stock prices: equity valuations rose above their historical average, record central-bank stimulus failed to fuel faster growth, and corporations, having already wrung out significant inefficiencies, made fewer gains in streamlining and improving profit margins, especially in the U.S.

In fact, over the last 13 years, since the bottom of the 2008-2009 financial crisis, the stock market has increased about six-fold (even after this year’s -21% correction) in the face of some horrendously scary headlines (also see chart below): · Ukraine-Russia. PRICES: Valuations have come down significantly – Price/Earnings ratio of 15.9

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content