This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

One of the best tax deductions for a small business owner is funding a retirementplan. Beyond any tax deduction you are saving for your own retirement. You deserve a comfortable retirement. If you don’t plan for your own retirement who will? Note the Solo 401(k) is also referred to as an Individual 401(k).

Advisor Today Guest Column January of 2025 is the 50th anniversary to one of the most important pieces of legislation in the retirementplanning arena ever put into law by Congress. What Im referring to is the enactment of ERISA, the Employee Retirement Income Security Act.

Many of us are covered by one or more types of defined contribution retirementplans, such as a 401(k), 403(b), 457, or any of a number of other plans. What many of these plans have in common is that they are referred to as Cash Or Deferred Arrangements (CODA), as designated by the IRS. Don’t Take A Loan.

a ski chalet), assessing whether it will lead to greater overall wellbeing, or, alternatively, more stress, is more challenging Enjoy the 'light' reading! a ski chalet), assessing whether it will lead to greater overall wellbeing, or, alternatively, more stress, is more challenging Enjoy the 'light' reading!

Also in industry news this week: The latest update on the status of the Department of Labor's proposed regulation related to fiduciary advice on retirement accounts and why the agency is referring to it as a "retirement security rule" rather than a "fiduciary rule" A report suggests that RIA M&A surged in the 3rd quarter, as large acquirers resumed (..)

Your retirement income plan may be sending up bubbles, too, whether around Social Security, retirement account distributions, taxes or somewhere else – and these holes need to be patched up right away. So, to help your retirementplan be more airtight, let’s look at a few of the common leaks.

AI engines also analyze context ensure your website content clearly defines your services, location, and specializations (e.g., “retirementplanning for small business owners” or “estate planning in New York”). Use niche-specific keywords like retirementplanning for physicians.

While grappling with various aspects of retirementplanning, it is imperative to acknowledge a critical factor that often does not receive its due attention – longevity risk. Longevity risk refers to the risk that people are living longer lifespans than previous generations.

Instead, your general practitioner may have referred you to that cardiologist to diagnose a specific heart problem. We want our clients, our prospects and those who refer us to understand what we’re great at and that we’re specialists in that field, much like cardiologists are specialists in their field.

The concept of retirementplanning is simple. Despite changes in the economy or in life itself, the concept of planning your retirement has remained unchanged. We work, save, retire, and repeat for generations over. However, it goes without saying that your retirementplan and spending habits need to be flexible.

Vesting refers to the ability of a participant to take all money in their 401(k) plan with them when leaving an employer. The Microsoft 401(k) retirementplan offers many excellent choices among actively managed and index funds. The Plan is subject to change by Microsoft.

The IRS website has this helpful Tax Withholding Estimator you can use as a reference if you are unsure how much to withhold. Explore Tax-Advantaged Accounts: One way to lower your tax burden is to take advantage of your employer’s retirementplan if they have one by contributing pre-tax dollars into your 401(k) or 403(b).

For reference, a correlation of 1.0 Retirementplanning, like any type of robust financial planning, should include stress testing your investment strategy and financial plan. means the assets are perfectly correlated and will move in tandem. After all, volatility is a when , not an if.

Now, when “work” is mentioned, it doesn’t refer to your 9-to-5; it refers to dedicating yourself to projects and endeavors that challenge you and pose an opportunity to achieve something. In other words, you’re not working for money anymore—you have that covered with a comprehensive retirementplan.

Add keywords your audience might use, like Financial Advisor | RetirementPlanning or “Wealth Management | Tax Planning.” Include Keywords for Discoverability People search Instagram like they do Google, so include keywords like retirementplanning, wealth advisor, or student loan help to boost discoverability.

While they do share some similarities, there are enough distinct differences between the two where they can just as easily qualify as completely separate and distinct retirementplans. Either plan is an excellent choice, particularly if you’re not covered by an employer-sponsored retirementplan. Not exactly.

Take advantage of tax-advantaged retirement accounts such as 401(k)s, IRAs, and Roth IRAs to maximize your contributions and benefit from tax-deferred or tax-free growth. Learn more about retirementplan options here. Aim to contribute as much as you can afford to these accounts each year to accelerate your retirement savings.

These five key components will help simplify the bucket strategy so you can understand it and apply it to your retirement strategy. The retirement bucket strategy refers to the idea that your retirement savings can be separated into three buckets, one of them being the Risk Bucket. The Risk Bucket. The Safe Bucket.

However, they also frequently work with clients whose businesses sponsor employer retirementplans that must adjust their systems and raise workers’ awareness to enable them to fully tap into their benefits. Financial advisors often focus on high net worth clients whose wealth stretches far beyond that eligibility.

The fundamentals of Roth and traditional IRAs Traditional IRAs have long served as a cornerstone of retirementplanning, offering immediate tax benefits through deductible contributions while deferring taxes until withdrawal. Ready to explore whether a Roth conversion aligns with your retirement strategy?

This data can serve as a baseline for tailoring your retirementplan, taking into account factors such as inflation, your current age, and your desired retirement age. These figures can serve as a valuable reference point for individuals planning their retirement.

Both the Mega Backdoor Roth IRA and Mega Backdoor Roth 401(k) allow the additional contribution of funds to retirementplans after pre-tax and Roth contribution limits have been reached. Roth IRAs are also not subject to Required Minimum Distributions (RMDs), allowing more flexibility in retirementplanning.

A few things from the last couple of days all with the theme of retirementplanning mistakes to avoid. The 4% rule of course refers to the percentage that can be safely withdrawn from portfolio assets for a sustainable retirement (not running out of money).

Price Action Lab had a blog post that amusingly referred to managed futures as being a long term commitment. That led to an older post that tried to figure out the optimal allocation to managed futures.

There was also a reference to the term on an episode of The Simpsons. Increasing the RMD age to 75 will change quite a few aspects of this part of retirementplanning. I referred to it as both complex complexity and multivariable complexity. As I've blogged about it, I reiterated my concern about it being overly complex.

Introduction to GIFT City and Its Legal-Economic Status The Gujarat International Finance Tech-City, commonly referred to as GIFT City, is a landmark initiative by the Government of India aimed at creating a world-class financial centre within the country.

Some states also offer tax exemptions for Social Security benefits and other retirement income sources. Assessing the tax structure of your state and constructing your retirementplan and financial strategy around your state’s tax system can help you stay a step ahead in retirement.

Today, Meb Tweeted out a reference to the Atlas Lifted report from Robeco which references a similar idea, the Global Market Portfolio which is allocated as follows. This is a little bit of a follow up to yesterday where I mentioned the Global Asset Allocation as mentioned in a paper by Meb Faber.

Leveraging retirementplans for tax advantages Tech entrepreneurs can create substantial tax advantages through Solo 401(k) plans, which allow contributions up to $69,000 in January 1, 2024 for those under 50. For growing tech startups, establishing company retirementplans serves multiple purposes beyond tax benefits.

They are not really proxies for their reference equities, the are products that sell volatility on their reference equities. That's not clear to me but for anyone really wanting Tesla with some income, the 90/10 combo turns it into a 4% yielder based on 2024's payout thus far.

600,000-$800,000 are workable numbers for long term retirementplanning. That range might not equal anyone's retirement number but a couple of lifestyle tweaks or changes and I think it's a range people could adapt to. Barron's referred to the $439,000 shortfall as a gap. million) on top of Social Security.

However, within our current conversation, I can refer back to what we've talked about earlier in this same chat session. I also don't use our conversation to update my training or improve my responses for future users. This means I can't build on things we've discussed in past conversations or remember your preferences over time.

The Bloomberg note might have been referring to the type of funds that go for alpha no matter what and that can be a difficult way to make a living. Of course it would have been better for it to have been up a little but that sort of decline is far from a failure compared to expecting up a little and it dropping 25%.

Then Anderson, referring to a different colleague said "he was even more frustrated than I am that public-market investors havent adopted the view that outperformance is reliant on extreme winners." range, those same funds might be very hard pressed to get back to today's prices.

I've heard managed futures and carry referred to as being cousins. The variation of carry that RSSY uses goes long markets in backwardation and short markets in contango. Those are different things (repeated for emphasis) and so they can be differentiated return streams from each other. Similar but different.

When you turn age 72, you’re required to begin receiving distributions from the plan. This is always true when neither you nor your spouse are covered by an employer-sponsored retirementplan. The numbers are different if you’re not covered by an employer-sponsored retirementplan, but your spouse is.

Like YieldMax, I'd say these don't track their reference securities, they are products that sell the volatility of their reference securities. Here are two examples. And There's differentiation there but they don't really look like the common. The assets are pretty low in these.

Do you specialize in retirementplanning for small business owners? This program can encourage your clients to refer others. You can think about offering rewards for people who refer others to you. It is nice to show gratitude to clients who refer others. Make it simple for clients to refer people to you.

He referred to the non-managed futures alts at "diversified alpha" but never specified what strategies to include with managed futures. This has sort of been my positioning. A 50 year old with $10 million happily living a $150,000 lifestyle might not need more than 25% in equities but that's not most people.

The name of the fund refers to the tendency of tail risk strategies to lose a lot of money waiting for the next disaster. Matthew Tuttle talked about this a couple of weeks ago but his firm just filed for the Tuttle Capital No Bleed Tail Risk ETF. There aren't too many tail risk funds out there.

The Wall Street Journal took what might be a sympathetic approach to 401k investors who might be feeling disillusioned by generally poor performance with the focus being on target date funds which have of course become a major staple of 401k plans. First, it's your retirement, how do you not care enough to engage just a little?

Employee Stock Ownership Plans (ESOPs) An ESOP allows owners to gradually sell their shares to employees through a qualified retirementplan. Buyers, however, may inherit more risk, which can affect the sale price or deal structure. This approach can create win-win outcomes for both you and your staff.

4 Reasons you should A 401k is one of the most common types of employer-sponsored retirementplans. Maxing out your 401k further helps you build these hard-to-access retirement savings. A 401k match means your employer will put money into your retirement account based on what you’re contributing on your own.

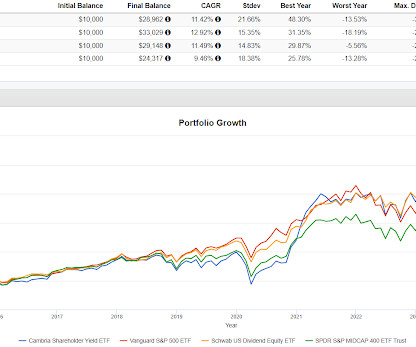

Shareholder yield refers to " companies that are returning their cash to investors through three attributes - dividends, buybacks and debt paydown. Barron's interviewed Meb Faber of Cambria Investments. The main focus was the Cambria Shareholder Yield ETF (SYLD).

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content