This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

For many financial advisors, a core part of the retirementplanning process involves simulating whether the client's assets will last through retirement. That emotional connection supports confidence and increases the likelihood that the client will stick with their plan and stay committed through both good markets and bad.

riabiz.com) Creative Planning is exploring its custody options. investmentnews.com) Research The problematic math of passing down generational wealth. blogs.cfainstitute.org) How life events affect retirementplanning. investmentecosystem.com) Reflections on eight years of running a financial planning practice.

(youtube.com) Christine Benz and Amy Arnott talk with Peter Mallouk, President and CEO of Creative Planning, about the 'messy' business of financial advice. podcasts.apple.com) Jordan Haynes talks with Justin Castelli about the important role of life planning. thinkadvisor.com) Not everyone is happier in retirement.

When planning for retirement, it’s effectively impossible to precisely forecast the performance and timing of future investment returns, which in turn makes it challenging to accurately predict a plan’s success or failure.

Start planning early. The essence of retirement lies in reclaiming your time, on your terms and with confidence. Yet far too many professionals delay the planning process. To show you what’s possible and what’s necessary, if early retirement is something you want to pursue seriously. Retiring at 55? Doing it right?

When you get it wrong, it crushes your retirementplans. My own track record at making big calls is pretty damned good, but none of our clients wants me slinging around their retirement monies based on my gut instinct. The less it matters, the easier it is to be bold and outside of the mainstream.4 More on this later.

This approach typically provides greater benefits to those who have significant assets and high taxable income in retirement. Inheritance and estate planning There are a couple ways a Roth IRA conversion can assist with estate and legacy planning. A spouse may also elect to defer RMDs if they inherit the account.

New statements may make it easier to see what you have, but what should you focus on when making a retirement income plan? Having an income plan is key for your retirementplanning. Having an income plan is key for your retirementplanning. Look at the math to understand and believe it.

I understand the difficulty of that one but if you're 50, overweight and taking a half dozen medications, you should plan on health stuff being very expensive. I've said many times that I plan to wait until 70 and that I think my wife should take hers at the same time which would be 64 and 2 months. number for her.

First, is the math right based on my numbers? I think I can stick to my plan of not selling until it grows into a life changing piece of money but we'll see. If we guess just 2 billion people, and that is just a guess, and divide that into the 15.2 How can it solve anyone's problem?

3] So, it’s easy math: the less you work, the less you’ll earn. Next, try to hold off on filing for Social Security benefits until you reach full retirement age. Lastly, it is crucial that individuals planning to earn Social Security monitor their earnings and check for mistakes once enrolled.

This article will explore how to navigate complex tax situations arising from multiple income sources, examining various income types, reporting requirements, self-employment obligations, and strategic approaches to record-keeping and tax planning that can help protect your financial interests. rate is comprised of two components: 12.4%

Optimizing your 401(k) is a mix of planning, saving for the future and self-awareness, but it’s simpler than you think. Let’s look at a few 401(k) planning basics to get you started. 1. Understand Your Plan The best kind of money isn’t old, new or even tax-advantaged – it’s free money! Not an Afterthought Life gets busy.

Financial planning services 12. If you’re good with math, then turning to financial planning or accounting or opening up a similar company could be one of the best recession proof businesses to start! Financial planning services Financial advisors and planners are essential, especially during times of economic uncertainty.

James and Pamela’s Big Dream Excerpt from The Smart Person’s Guide to Financial Planning & Investments: A Simple and Straightforward Approach to Understanding Your Personal Finances By Michael J. Their retirementplan is strong, their kids are independent, and they are debt-free. So—problem solved, right? Well, actually, no.

It's been a while since this sort of thing was relevant for my day job so something could have changed, weeklies didn't exist for example, but if my math is correct then it was way over exposed which would account for last week's decline in the fund price. Please leave a comment if I did the work incorrectly.

There was an article on LinkedIn (via Abnormal Returns) by Victor Haghani that dug into the math working against leveraged ETFs. Eric Balchunas from Bloomberg was baffled because the 1x version only has $60 million in AUM and trades about $1 million per day.

And checking in on the GraniteShares YieldBoost SPY ETF (YSPY) that sells put spreads on a levered S&P 500 ETF; Yes, that is a rough start, clearly, but interestingly the math checks out. YSPY sells put spreads on a 3x fund. Oddly, the fund page no longer mentioned targeting a 2x outcome, it appears to now say 3x.

Some of these relationships are with people who want to retire or who are already retired. Math has no emotion, but people do. Mindsets People who are comfortable in their own skin seem to adapt best to retirement. Most of us can figure the rate of return on money. But the higher up a person has gone, the harder it is.

One advisor noted that these events draw not only current clients but also curious prospects who are actively exploring retirementplanning options. Tax Strategy Workshops Workshops like “Creating Tax Efficient Retirement Strategies” attract attendees who are serious about their financial future.

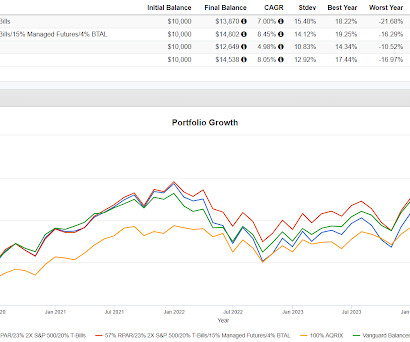

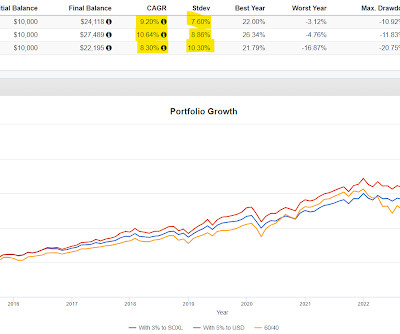

Do the math, it would be a fantastic long term result but very difficult to pull off. Maybe the model providers don't really want their models to differentiate. Something like a 75/50 portfolio might fit in the discussion of endowment style. 75/50 seeks to capture 75% of the market's upside with only half the downside.

Social Security RetirementPlanning . While there always seems to be a future funding shortfall for Social Security, it’s a political problem, not a math problem. Please contact us if you’d like to discuss your financial plan. Our law firm is Yardley Estate Planning, LLC , and is in the same place.

Generally they all plan to work to 70 or beyond out of necessity. There was an odd and I believe inaccurate emphasis on workplace retirementplans pivoting from defined benefit plans (pensions) to defined contribution plans (401k) starting around the turn of the century. That is Rooster. Rooster loves duck toys.

The way Portfolios 1 and 2 are weighted, the math works for being a 60/40 portfolio and then from there we add portable alpha/capital efficiency/return stacking. As I read the FT article, I had a thought about how to try to make the fund work as part of diversified portfolio, not the entire portfolio.

Yahoo warned of potential problems retirees may face if their plan is to rely solely on Social Security. Simple math is that this person needs to save $23/yr to come up with that additional $350,000. But simple math tells you that adding $5000/yr likely won't cut it. 5000 per for 15 years is $75,000.

And then just a little math, the "guarantee" based on the 50/50 allocation would be 2.5% If you're trying to do something as simple as 50% in T-bills now yielding 5% and one equity proxy, don't make that one equity proxy a narrow bet like tech stocks. SSO is 2X S&P 500 and SPHB is the Invesco S&P 500 High Beta ETF.

That is difficult to pull off but if you do the math on that it shows long term outperformance. A 25% allocation to equities for someone who needs equity market growth for their plan to work won't get it done. 75/50 seeks to capture 75% of the upside with only 50% of the downside.

Simple math, it looks like the carry index has compounded at less than 3%. This next chart from Bloomberg compares just the carry component of the FOXY fund to the S&P 500 and T-Bills. The black line for carry looks like it is somewhat uncorrelated which is different than negatively correlated. The red line for T-bills is price only.

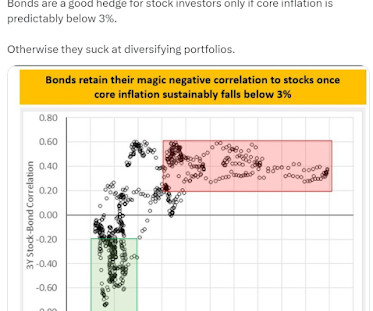

The simple 40 year trade for bonds of "number go up" is finished and as a matter of math, can't be repeated. The diversification benefits of intermediate and longer term bonds is not what it used to be. Taking volatility out of a fixed income portfolio is fairly simple.

The course covers an introduction to personal finance, credit cards, life insurance, health insurance, investment instruments, loans, income tax and planning, budgeting and building a strong portfolio. Also, you will learn how to plan your taxes, credit score importance and how to budget your income to create a portfolio.

I haven't seen too many scenarios where Roth conversions were optimal as most people don't earn more after they retire. Do the math on your particulars like what your various sources of earned income will likely be, how much your RMDs will likely be and so on. I'm paraphrasing Slott.

The article devoted a good amount of space to bond market math, focusing on the pain of owning the iShares 20+ Year Treasury ETF (TLT) and bond funds in general. I've been like a broken record for years on the need to avoid bonds that have any sort of duration or at least be extremely underweight duration versus the typical benchmarks.

Generally speaking, pensions are less viable than they used to be, the math doesn't work as well. About 40 years ago employers started to pivot away from pensions to 401k, they started to pivot away from defined benefit plans to defined contribution plans. Problems have been long in the making and seem to have gotten worse.

However, if the goal is to pay off a mortgage before retirement to spend would-be mortgage payments on other things during retirement, the math may not work out. For one, any savings from retiring home debt is a one-time savings (the interest expense).

As a financial advisor or other investment professional, you’re no doubt already well aware that the “math” side of the conversation is a large part of what your clients need help with every day. Investment Planning. RetirementPlanning. Self Employed Plan Contribution. Beneficiary RMD Calculator.

A harsh reality is that $50,000 is not a retirement fund but it is a pretty robust emergency fund. We've gone over the math before that starting as late as 55 can catch a lot of the way up if they can afford to save a very high percentage of their income.

Despite the leveraged semiconductor ETFs, when blended with USMV, the portfolio is underweight technology versus the S&P 500 using simple math, it works out to about 26% versus closer to 40% for the S&P 500. If someone were going to actually do this, I'd hope that they would plan out ahead of time how they'd handle a serious decline.

There's other math about outperformance but also the observation that momentum is prone to crashes. They said they were impressed by the backtest and the thought process underlying the strategy and shared this link to a short paper by Larry Swedroe posted on the Alpha Architect website.

If you do the math, that yields a better long term result in nominal terms and also in risk adjusted terms. He popped up ten or so years later writing occasionally at the old Index Universe website which later became ETF.com. 75/50 targets 75% of the upside and 50% of the downside.

If you’ve attempted to make a budget in the past and “failed” due to budget challenges , maybe it’s time to rethink your plan. If you’d like an even more streamlined budget plan, you could check out the 80/20 budget and apply it to your budget instead.) With this budget, you plan to save 20% of your total income. That’s it. (If

In the case of real estate a 2.29% weighting and for "private equity" companies it's about 17 basis points (looked at XLF holdings and then did a little math), that's just not going to move the needle. You may agree with Jack about not needing those things, that's valid, my point is that owning an index fund isn't a proxy for them.

In terms of complexity, several of the funds blend together multiple complex strategies and the blend itself is complex in terms of the math applied and the outcomes sought, they are complex-complexity. I do not know if his life circumstance is such where a game over approach is appropriate.

The way the math works, a 67% allocation to NTSX (Portfolio 2 with 33% in the T-bill ETF) equals 100% in Vanguard Balanced Index Fund (VBAIX) which is a proxy for 60/40 and Portfolio 3. It's not that leverage on its face must be bad but at the heart of many capital market calamities has been the misuse of leverage.

The math is only off by a shade using leverage via UST and a little bit of SSO, remember RPAR is leveraged. I find this to be interesting but anyone needing normal stock market growth in order for their retirementplan to work, probably isn't going to get it from any of these portfolios.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content