This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

represents our current state of healthcare, in which genetic makeup and the environment play a major role in illness and disease, and where the focus of doctors lies primarily on the administration of treatments to cure and mitigate human ailments; and Medicine 3.0 In the context of the financial planning industry, whereas Financial Advice 1.0

The post Tax Strategies for High-Income Earners 2025 appeared first on Yardley Wealth Management, LLC. Tax Strategies for High-Income Earners in 2025. In this comprehensive guide, we’ll explore proven strategies to help you minimize tax liability while staying compliant with current regulations.

Mistake #2: Not having an estateplan in place Estateplanning is essential for protecting what you’ve worked hard to build. A good estateplan ensures your assets go where you want them to. It can also help reduce taxes and make life easier for your family during difficult times. The result?

As the year comes to a close, now is the time to review potential financial moves to help minimize your tax burden heading into 2025. Proactive year-end taxplanning can lead to significant savings and set you up for financial success in the new year. Find your next tax advisor at Harness today. Starting at $2,500.

Tax deductions can save you thousands annually by reducing your taxable income through legitimate business expenses. Understanding these deductions is more critical than ever as tax laws evolve, presenting new opportunities for savings. Understanding this distinction is crucial for maximizing your tax benefits effectively.

Start saving early by contributing to tax-advantaged accounts like 529 Plans or Coverdell Education Savings Accounts (ESAs). These accounts come with tax benefits that can alleviate future financial pressures when it’s time for your child to attend college.

And if they’re unprepared—or worse, if the family estateplanning strategies are less than buttoned up—how will that affect your practice down the line? To start the conversation with clients preparing to transfer wealth, you can simply say: “Tell me about who in the family was involved in the development of your estateplan.”

They develop comprehensive strategies addressing savings targets, retirement timing, Social Security optimization, healthcare costs, and estateplanning – crucial elements that might be overlooked when planning alone. Exploring the Benefits of Financial Planning appeared first on Yardley Wealth Management, LLC.

A financial advisor can help with maximizing your retirement income through taxplanning After retirement, your income sources may become limited to pensions, Social Security benefits, and investment income. A financial advisor can craft tax-efficient withdrawal strategies to minimize the tax burden on your retirement income.

Plan for out-of-pocket costs for fertility treatments and costs to deliver your baby. Once your new dependent arrives your monthly premiums for healthcare will increase. Plan for family leave from work. Take advantage of tax breaks. Be sure to take advantage of child and dependent care tax credits when filing your taxes.

Maintaining Physical and Mental Health This might not be an apparent point at first, but maintaining physical and mental health in retirement can help you reduce one of the largest expenses many people incur as they age: healthcare. 5] If you’re interested in creating and preserving generational wealth, you’ve found the right place.

At any given moment, people are working towards multiple goals like saving for retirement, managing taxes, buying a home, protecting their family through insurance, or planning for healthcare needs. For example, a clients investment choices should align closely with their tax strategy, too.

But that doesn’t mean the actual assets are just split down the middle, and some assets are much more favorable from a tax perspective than others. Once the divorce is finalized, a crucial (but often overlooked) part of the process is updating estate documents and beneficiary designations. Cash assets have no tax implications.

The post Part 3: Tax-Wise Financial Planning appeared first on Yardley Wealth Management, LLC. Part 3: Tax-Wise Financial Planning In our last two pieces, we covered some tools of the tax-planning trade, as well as how to deploy them for tax-efficient investing. Life happens. You buy a business.

The post Part 3: Tax-Wise Financial Planning appeared first on Yardley Wealth Management, LLC. Part 3: Tax-Wise Financial Planning. In our last two pieces, we covered some tools of the tax-planning trade, as well as how to deploy them for tax-efficient investing. . Tax-Planning Possibilities.

The post Part 2: Tax-Wise Investment Techniques appeared first on Yardley Wealth Management, LLC. Part 2: Tax-Wise Investment Techniques In our last piece, we introduced some of the tools of the tax-planning trade. In other words, your tax-planning techniques matter at least as much as the tools.

The post Part 2: Tax-Wise Investment Techniques appeared first on Yardley Wealth Management, LLC. Part 2: Tax-Wise Investment Techniques. In our last piece, we introduced some of the tools of the tax-planning trade. In other words, your tax-planning techniques matter at least as much as the tools.

Retirement planning can be a bit complex. There are multiple factors to weigh in, right from healthcare and inflation to estateplanning, business succession planning, taxplanning, and more. However, the main drawback to this can be the lack of foresight regarding what and how to plan.

The post Part 1: The Tools of the Tax-Planning Trade appeared first on Yardley Wealth Management, LLC. Part 1: The Tools of the Tax-Planning Trade Whether you’re saving, investing, spending, bequeathing, or receiving wealth, there’s scarcely a move you can make without considering how taxes might influence the outcome.

The post Part 1: The Tools of the Tax-Planning Trade appeared first on Yardley Wealth Management, LLC. Part 1: The Tools of the Tax-Planning Trade. Whether you’re saving, investing, spending, bequeathing, or receiving wealth, there’s scarcely a move you can make without considering how taxes might influence the outcome.

According to the Fidelity Retiree Health Care Cost Estimate, the financial burden of healthcare in retirement is substantial. As a couple aged 65 in 2023, you may need approximately $315,000 saved (after tax) to cover your healthcare expenses. The absence of a dedicated healthcare fund can lead to unexpected financial hardships.

Financial Planning Needs: Retirement planning Education and family planning Obtaining appropriate insurance coverage Business and taxplanning Significant asset purchases Strategies for Serving Clients in This Stage: Clients at this stage are experiencing life events — both large and small — that will impact their financial planning needs.

Healthcare Open enrollment is an excellent time to reassess your healthcare needs for the upcoming year. Here are a few items to review for your healthcare benefits: Consider if you need to change the type of healthcareplan you will have for the upcoming year.

As a company founder, early startup employee, or small business owner, you may find yourself in a higher tax bracket as your business grows or you realize gains from equity compensation. But that doesn’t mean you simply have to accept a higher tax bill. Here are 20 tax-efficient actions to consider when filing your taxes in 2024.

Contributions to your 401(k) are pre-tax, meaning that for every dollar you contribute, you actively lower your taxable income. If you’re covered by a workplace retirement plan, you likely won’t be eligible to make deductible (pre-tax) contributions to your traditional IRA, but investing in it still provides valuable benefits in retirement.

Create or revise your estateplan 9. Plan for emergency expenses 11. Create or revise your estateplan While it’s not the most cheerful topic, having an estateplan is crucial when you’re preparing for a baby. If you already have an estateplan, make sure to update it to include your new baby.

Whether it’s supporting education, healthcare, environmental conservation, or cultural initiatives, contributing to meaningful causes can enhance one’s sense of fulfillment and happiness. Financial and Tax Benefits of Charitable Giving From a financial perspective, charitable giving offers significant tax benefits.

Contributions to your 401(k) are pre-tax, meaning that for every dollar you contribute, you actively lower your taxable income. If you’re covered by a workplace retirement plan, you likely won’t be eligible to make deductible (pre-tax) contributions to your traditional IRA, but investing in it still provides valuable benefits in retirement.

Accessibility – Nearby restaurants, shopping, entertainment, library, classes; Walkability Access to care – Proximity to caregivers, availability to high-quality healthcare Cost of Living – Food, transportation, housing, entertainment, taxes Proximity – Close to family or support systems Examples of Housing in Retirement There are (..)

This approach may include a mix of equities, bonds, mutual funds, and real estate, tailored to provide long-term returns that outpace inflation and contribute to a stable financial foundation in retirement. Tax efficiency A savvy retirement strategy also involves optimizing tax implications.

While it may seem like a luxury that is only available to the wealthy, anyone is capable of building an effective financial plan and putting it into action. Without effective personal financial management, you risk losing money to poor budgeting, poor taxplanning, or even just to inflation.

Or are you focusing on older people who are concerned about estateplanning for retirement or retirement income planning? Pain Points: These are issues like market ups and downs, tax problems, and money planning being hard. Explain how to manage your retirement funds and pay for healthcare.

List your essential needs—housing, groceries, utilities, and healthcare. Look for: car repairs and maintenance, medical expenses, home maintenance, membership renewal, seasonal utility increases, vehicle registration renewal, back to school supplies and field trips, tax preparation fees. These goals are all about securing your future.

Planning for retirement is one of the biggest financial challenges you will ever face, and a financial advisor can help you adopt a strategy that can take you to your goals, mitigate risk, and adapt to the changes that will inevitably come your way. Retirement planning can be a long-term journey, and a lot can change along the way.

It can require a deep understanding of personal finance, investment strategies, tax implications, and more. A financial advisor can help you understand the intricacies of financial planning for physicians. Not creating a comprehensive financial plan Financial planning for physicians and healthcare professionals is essential.

Furthermore, ChatGPT may have limitations in reflecting recent policy changes or potential mathematical fallacies that can impact retirement and taxplanning strategies. This blog explores the strengths and limitations of employing ChatGPT vs. a financial advisor when planning for retirement.

This percentage accounts for the likelihood that some pre-retirement expenses, such as commuting to the office and socializing, may decrease while others, such as travel and additional healthcare costs, may increase. Applying the 80% rule, you should plan on having at least $72,000 annually during your retirement years.

BITTERLY MICHELL: Meaning custodians, of course, like in terms of — of counterparty, but also thinking of like your wealth planning and the structure of your assets, the trusts that are available to you, how you want to think about trust and estateplanning. It’s different wealth regimes, it’s different tax regimes.

As a Christian, your estateplan should represent your dedication to financial stewardship according to Scripture. W hat important factors should Christians consider when estateplanning? W hat important factors should Christians consider when estateplanning?

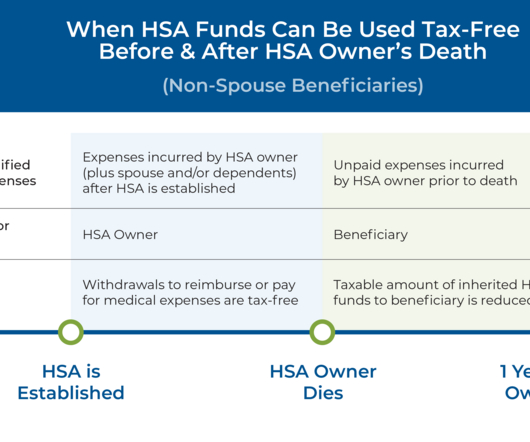

Health Savings Accounts (HSAs) feature useful tax advantages that make them a popular savings vehicle. One possible outcome of ‘superfunding’ an HSA, however, is that the account owner may not actually use up all of their HSA funds over their lifetime, which can have significant tax consequences. Read More.

Estateplanning is not just for the wealthy; it is essential for anyone who wants to ensure their assets are managed and distributed according to their wishes. Whether you own an elaborate portfolio or a single family home, having a comprehensive plan in place can protect your legacy and provide peace of mind for your loved ones.

This may include topics such as retirement income planning, asset allocation strategies, healthcare costs, long-term care costs, withdrawal strategies, tax minimization, and estateplanning considerations.

Investment planning also plays a crucial role in tax optimization, enabling you to minimize tax liabilities and maximize after-tax returns. Additionally, tax-loss harvesting, and other tax-optimization strategies can further improve the tax efficiency of your investment portfolio, thereby enhancing overall returns.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content