This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Also in industry news this week: NASAA has proposed an amendment to its broker-dealer conduct model rule that would restrict the use of the terms “advisor” and “adviser” for broker-dealers and their registered representatives who are not also investment advisers or investment adviser representatives A recent study suggests that (..)

Nonetheless, given the scale and brand awareness of the wirehouses, and as their own use of fee-based models increases (as opposed to primarily relying on commissions from selling products), competition for clients (and advisors) will likely remain stiff going forward, even amidst the favorable trends for RIAs Also in industry news this week: A recent (..)

So historically, every $1 million invested would yield annual dividend income of $19,800 on average… before tax. If you own 10,000 shares, you receive $40,000 in dividend income (before taxes) and have a portfolio currently worth $2M. Over the last 30 years, the S&P 500’s average dividend yield was 1.98%.

Tax-loss harvesting is a powerful strategy that investors can use to reduce their taxable income. As effective as tax-loss harvesting can be, there are a number of important details that investors need to be aware of in order to implement the strategy successfully while following regulations. How does tax-loss harvesting work?

As the year comes to a close, now is the time to review potential financial moves to help minimize your tax burden heading into 2025. Proactive year-end tax planning can lead to significant savings and set you up for financial success in the new year. Find your next tax advisor at Harness today. Starting at $2,500.

Because of these differences, stocks and bonds accomplish different things in an assetallocation. Note: Since most investors are more familiar with stocks, a comparison of risk and return within the equity market has been intentionally omitted from this article). Taxes, fees, expenses, trading costs, etc.

If one stock makes up more than 10% of your overall assetallocation, it’s probably too much. Charitable Contributions: Donating appreciated stock to charity while reducing capital gains tax. This includes the stock itself, its sector, industry, and other highly correlated assets.

In this article, we’ll break down the concept of waterfall wealth distribution, its benefits, and how it compares to traditional investment strategies. Key benefits include: Ensuring essential financial obligations are met first – Taxes, estate planning, and retirement savings take precedence.

A portfolio review can help you: Assess your investment objectives and confirm they align with your financial plan Evaluate your time horizon and risk tolerance Ensure proper diversification and assetallocation Review tax management strategies, including capital gains and the Net Investment Income Tax (NIIT) Monitor performance beyond just returns, (..)

If youre searching for a fiduciary financial planner, flat-fee financial planning, or the best alternative to AUM-based advisors, this article will help you decide which model is right for you. Unlike AUM advisors, they dont have an incentive to keep assets under management, so their recommendations are truly objective.

I found their assetallocation and wanted to see from the top down if there's a way to mimic them to some extent and get decent results. Yahoo Finance had a cleverly titled article; Generation X is gloomy, but their retirement reality may not bite. A few different things today. Here's how I built the portfolio. No kidding.

The process of diversifying among asset classes is known as assetallocation, and the exact composition should be based on your financial goals and risk profile. You can also further diversify within an asset class. You should be re-evaluating your assetallocation at regular intervals to keep your portfolio on track.

The starting point today is the that Rational ReSolve Adaptive AssetAllocation Fund (RDMIX) has gone through a strategy change, renaming as the ReturnStacked Balanced Allocation & Systematic Macro Fund and keeping the same symbol. " balanced allocation and $1 of exposure to a systematic macro strategy."

Barron's had an interesting article about a BofA study showing that over a period of many decades an assetallocation of 60% equities/40% commodities outperformed an allocation of 60% equities/40% fixed income by 0.80% per year. I haven't looked in awhile I guess but yowza, a lot of option-centric funds.

Identify what areas you could cut back or reallocate funds to align with your financial goals for the new year If you don’t yet have a budget – here is a great article from Vida about a good place to start Consider using a budgeting app to help you track your spending – here are a few good options of apps we would recommend.

This article will explore how often to rebalance your 401(k). Rebalancing a 401(k) refers to adjusting the assetallocation of your investment portfolio back to its original target percentages. As a result, your portfolio’s allocation changes from its original, and it now consists of 60% stocks, 25% bonds, and 15% cash.

Tax Time April is fast approaching, which means it’s that time of the year when Uncle Sam will come knocking on your door with your tax bill. Perhaps your taxes have already been prepaid and a refund is coming your way. Subscribe Here to view all monthly articles. The same concept holds true for investing.

GAA stands for Global AssetAllocation and it has been lagging for 15 years. Barron's had an article about alternatives sought by the "super rich. Included in the article were aging whiskey which I don't what that is, like maybe something to do with leasing the barrels? Here's a great chart to illustrate the point.

Several talked about tax issues, it is important to keep tabs on how taxes might change going forward and then when they actually do change. Yes on the taxes but without earned income and living on long term capital gains from an investment portfolio, there might be no income tax.

Barron's had an article about Bill Ackman's closed end fund that trades in Amsterdam but is on the US pink sheets with symbol PSHZF. MDCEX is in Morningstar's Tactical AssetAllocation (TAA) category and the Fidelity info page for the fund offers the following comparison to other funds. This post is not about that fund.

Articles related to saving for retirement Start saving for your retirement today! Make funding tax-advantaged accounts a priority Tax-advantaged accounts are specifically designed to help savers build their retirement nest egg. Once in the account, your contributions will grow tax-free.

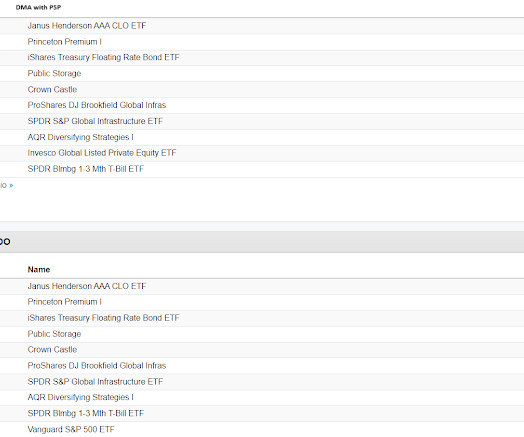

Here's the latest about Harvard from Bloomberg that included this chart of the assetallocation. It's not that someone could not copy the asset class exposure, just that the return streams would not look the same and often, various forms of sophistication replication does not really work in fund form. Black is 2023.

You can also get information on your performance and assetallocation. This will help you to create an assetallocation that will get you where you need to go with your investments. It can be used to help you with your assetallocation, at least based on the investment options that your plan includes.

In the vast majority of cases this ends up creating lower returns by creating unnecessary taxes and fees. You stay rich by allocating your saved income prudently. We often hear the mainstream media refer to nominal pre-tax and pre-fee returns of 10% or more for the stock market. 2) Set realistic savings return goals.

First up, the Harvard Endowment which posted the following assetallocation. Here's an article at theStreet.com from 2007 where I bagged on PSP. Arguably neither one is very close in terms of how it replicates but borrowing the assetallocation from the top down yields what I would call a valid result. I used PSP.

This article explores different ways in which financial advisors can help you with wealth accumulation for retirement. By helping you lower your tax The impact of proper tax planning on your eventual retirement balance cannot be overstated. All withdrawals from HSAs can be used for qualified health expenses entirely tax-free.

On A Shoestring ajackson Thu, 03/28/2019 - 08:20 In this article, we offer a robust analytical framework that can help endowments and foundations think about spend-rate planning, in terms of key risks they face such as short-term drawdown risk and long-term erosion of capital. Note that the 5% rule was intended to be a high hurdle.

In this article, we offer a robust analytical framework that can help endowments and foundations think about spend-rate planning, in terms of key risks they face such as short-term drawdown risk and long-term erosion of capital. On A Shoestring. Thu, 03/28/2019 - 08:20. Note that the 5% rule was intended to be a high hurdle.

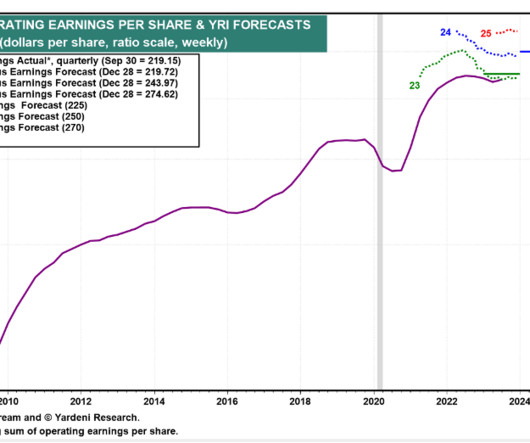

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (January 2, 2024). Subscribe Here to view all monthly articles. Time will tell if 2024 will make this baby cry, but whatever the market faces, declining inflation and interest rates should act as a pacifier. Slome, CFA, CFP® Plan.

This article will help you understand the benefits of working with a financial advisor to secure your financial future. A financial advisor can devise an assetallocation strategy by gaining a thorough assessment of your financial landscape. Assetallocation is the foundation of diversification and prudent investment management.

In this article, we guide you through the list of top personal finance courses designed for beginner to intermediate-level learners. The course covers an introduction to personal finance, credit cards, life insurance, health insurance, investment instruments, loans, income tax and planning, budgeting and building a strong portfolio.

AssetAllocation. Building on diversification, assetallocation is an investment strategy that builds your portfolio by weighing an adequate amount of risk for your goals. Assetallocation evaluates how your portfolio is created and the specific securities you are investing in. Dollar-Cost Averaging.

They can help you analyze your current investments, optimize your assetallocation, and make necessary adjustments to ensure your retirement nest egg grows steadily. Which investments should I withdraw from, considering market conditions and tax implications? It pays to have a good wealth planner in your corner.

This article can help you understand what a financial advisor can help you with so you can go ahead and hire one as soon as possible. For instance, inflation can affect the purchasing power of your savings, tax laws can shift over time, and investment opportunities that seem promising today may not be as attractive in the future.

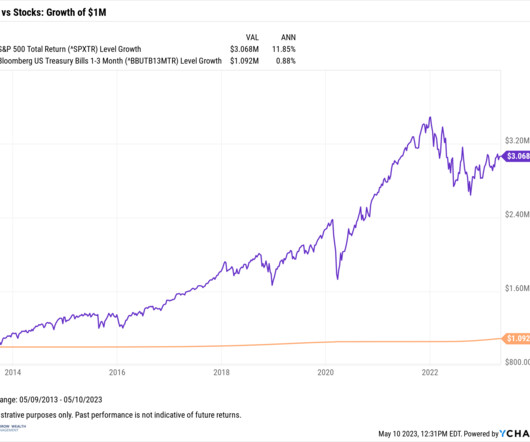

Cash isn’t an investment strategy For individuals with upcoming cash needs, perhaps for a renovation, taxes, or college, staying liquid in a high yield money market or locking in returns with a Treasury ladder can make a lot of sense. As illustrated in the chart below, short-term rates (in T-bills, savings accounts, money markets, etc.)

This article explores various strategies for diversifying an investment portfolio to ensure you have enough funds to live comfortably in retirement. Spread your investments across different asset classes Assetallocation involves distributing investments across different asset classes to balance risk and return.

Are you overly concentrated in one asset class, sector, or individual security? Risk Tolerance: What is your assetallocation? Tax Planning: Are you maximizing your tax-deferred investment accounts? Subscribe Here to view all monthly articles. Fees: What are you paying in advisor fees and/or product fees?

This article will discuss the key features of the Microsoft 401(k) plan, and after reading it, you should leave with a clear game plan of how to: Maximize the match (free money! ) Lower Taxes : Reduce taxes today via pre-tax contributions that reduce your taxable income. What Company Does Microsoft Use For Their 401k?

And gold, which is supposed to be an inflation hedge and safe haven, has been under pressure as investors have been offloading the yellow metal, putting pressure on prices, as this article summarizes. Multi-Asset Portfolios. Social | Podcast | Interviews | Articles about Justin all in one place. Consider Conservative Stocks.

Over the years, we've made some fun of CalPERS for seeming to change their assetallocation strategy every couple of years such that they end up chasing heat, that is chasing the thing that worked last year. It started with this article from The Athletic. Apparently, he was a great teammate.

In this article, we dive into the nitty-gritty of why saving for retirement should top your financial priorities list, the optimal time to start, and the best ways to save for retirement, ensuring you’re well-equipped to turn those retirement dreams into reality.

These items are not static, and can change over time, therefore it’s important to revisit your assetallocation periodically as financial circumstances and life events change your objectives. This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (June 3, 2024).

If the sell off was "exacerbated" by 0dte's as mentioned in the Bloomberg article, ok but down 1.5% They build out a few different types with various allocation percentages for each type. I was curious of course so I looked at the 60/40 blend under Strategic AssetAllocation. world is a good first impression.

There are three fundamental variables to monitor in portfolio management: market performance, changes in tax policy and a portfolio’s rate of drawdown (expenses and spending). Create a portfolio structure buffered against taxes. Therefore, it is essential that we structure client portfolios to be tax efficient.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content