This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

I’m currently maxing out my 401k, Roth IRA, and have roughly $45k in a taxable brokerage account. Via my company’s ESOP, my company’s stock has become 20% of my brokerage account even after selling a good chunk steadily over the past several years. A reader asks: I’m a 30 year old living in Brooklyn making $175/year.

On the other hand, the term "financial advice" often refers to much more than assetallocation and wealth management. This principle extends across many aspects of a firm's value proposition, from client newsletters to account log-in frequency to other common metrics of interest.

tonyisola.com) Age is just one factor when it comes to your assetallocation. mrmoneymustache.com) Why you need to account for your Treasury income on your state taxes. fastcompany.com) What to consider when rolling over a 401(k) account to an IRA. readthejointaccount.com) When a second home makes financial sense.

podcasts.apple.com) Assetallocation Small assetallocation shifts don't matter much in the long run. awealthofcommonsense.com) Why assetallocation matters. barrons.com) Why couples could benefit from separate and joint accounts. semafor.com) Retirement Cognitive decline is inevitable.

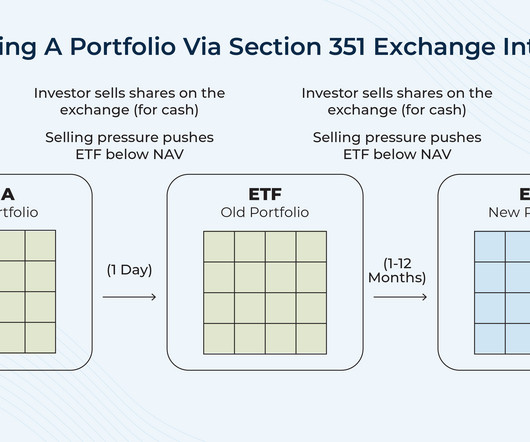

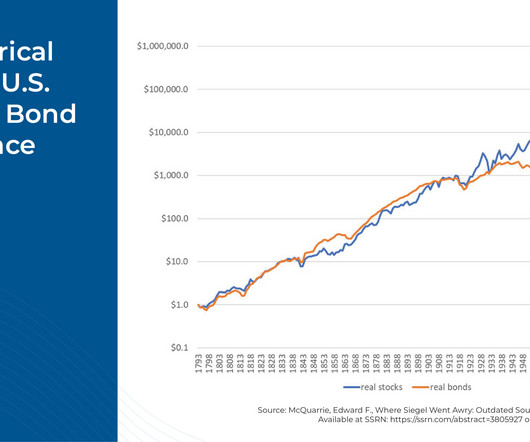

Following the long run-up in the US equity markets since the bottom of the 2008–2009 financial crisis, many investors with taxable investment accounts have likely found themselves with high embedded gains in their portfolios. While the gains signal portfolio growth, they also create challenges for ongoing management.

What is in your control : Your Portfolio : You want to create something robust enough to withstand drawdowns and recessions; not necessarily the best possible set of assets but the ones you can live with day in and day out. This includes a broad AssetAllocation including full Diversification of asset classes, geographies, etc.

(mrzepczynski.blogspot.com) There's not much to see in tactical assetallocation ETF performance. researchaffiliates.com) How does index fund ownership affect firm accounting quality? insights.factorresearch.com) Active share doesn't tell us anything about future performance. papers.ssrn.com).

peterlazaroff.com) Investing There's no magic rule for assetallocation. crr.bc.edu) Saving for college How much should you save in 529 accounts? (podcasts.apple.com) Peter Lazaroff talks with Manisha Thakor author of “MoneyZen: The Secret to Finding Your “Enough.”

Every document that considers the facts around any particular asset class will invariably include that disclaimer, but constructing a portfolio consisting of a mix of equities, fixed income, and other assets requires investors and advicers to make some fundamental assumptions around long-term expected returns and correlations between assets.

When investing in dividend stocks, bonds, or funds, a higher dividend yield may make an asset look more attractive, but this metric alone doesn’t make a worthwhile investment. In another words, if your assetallocation is 60% stocks and 40% bonds, the current weighted average yield is 2.19%.

Advisor-facing agents auto-populate account forms, flag missing items, and confirm custodian requirements on the fly—all without human intervention. What would normally require a lengthy back-and-forth of data entry, PDF uploads, manual reviews, and e-signature coordination becomes near-instant. This isn’t automation for automation’s sake.

Review your accounts and assess the extent of the damage that has been done. Investors who are well-diversified may be hurt but generally not to the extent of those who are highly allocated to stocks. Review your assetallocation . Step back, take a deep breath and relax. Take stock of where you are . Go shopping .

Reevaluate Your AssetAllocation If watching your investment portfolio fluctuate causes anxiety, your current allocation might be too aggressive. You can reduce your stock exposure and increase investments in fixed income options, such as cash or bonds, within tax-advantaged accounts (like a 401(k), IRA, or Roth IRA).

When investors create an investment portfolio, they consider several factors, like risk, asset class, inflation, etc., However, what is equally critical when it comes to creating a portfolio is assetallocation and selection. If not allocated efficiently, you may become subject to a slew of taxes and other charges.

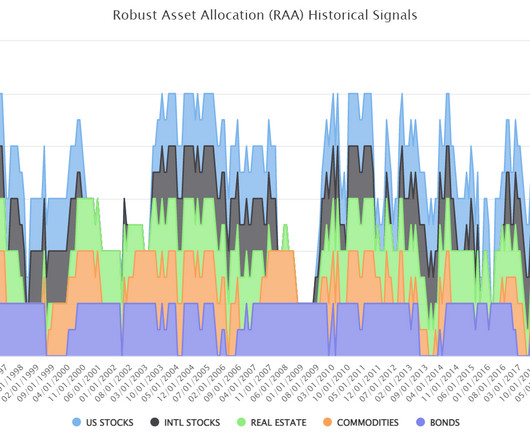

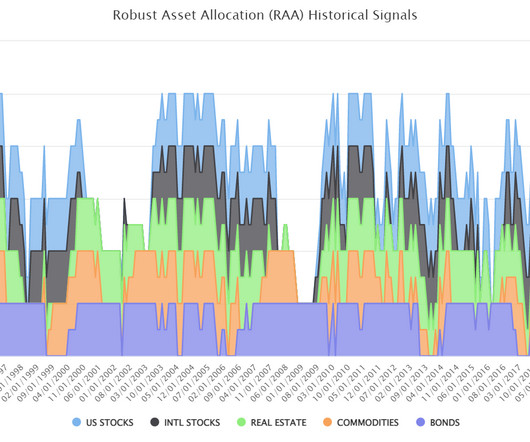

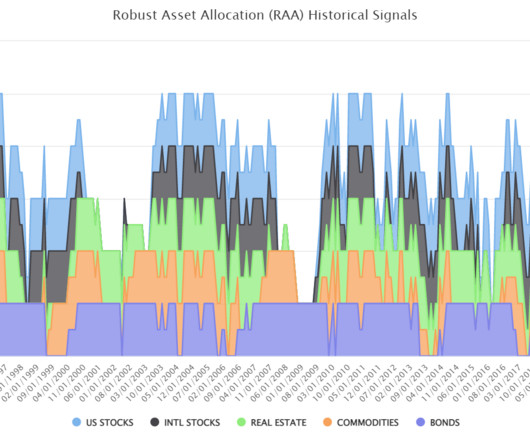

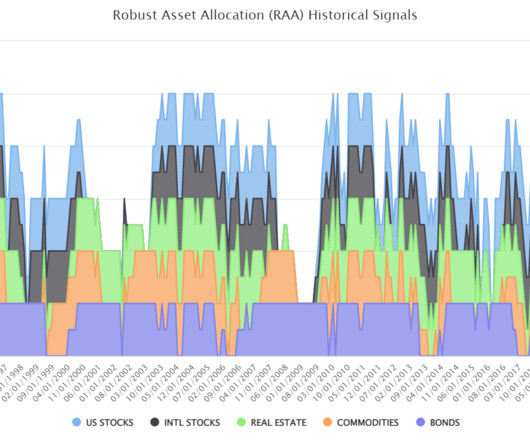

Do-It-Yourself trend-following assetallocation weights for the Robust AssetAllocation Index are posted here. Note: free registration required) Request a free account here if you want to access the site directly. If you are an advisor and want help implementing our models, please get in touch with Ryan Kirlin.

Do-It-Yourself trend-following assetallocation weights for the Robust AssetAllocation Index are posted here. Note: free registration required) Request a free account here if you want to access the site directly. If you are an advisor and want help implementing our models, please get in touch with Ryan Kirlin.

We also answered questions about 2025 retirement account limits, Coast FIRE strategies, when to take money off the table from the stock market, how to account for pension and Social Security income during retirement and how other economies impact the U.S.

Just a collection of the holdings in our various accounts along with some simple calculations — net worth, annual retirement contributions, assetallocation, how much we’re saving each year, etc. Guess I’m old school and, yes, kind of a personal finance dork. I can’t help it. It’s nothing fancy.

alphaarchitect.com) Performance The performance of tactical assetallocation mutual funds has been no great shakes. evidenceinvestor.com) Research The accounting treatment of intangible investments is too conservative. Inflation Hedging inflation is harder than it looks.

CIO Perspectives Webinar, 2022 AssetAllocation Outlook mhannan Fri, 03/18/2022 - 06:42 Markets have been unsteady at the start of 2022, driven by geopolitical tensions, inflation, and concerns about equity valuations. The war in Ukraine is causing even more uncertainty. Brown Advisory does not render legal or tax advice.

CIO Perspectives Webinar, 2022 AssetAllocation Outlook. CIO Perspectives Webinar, 2022 AssetAllocation Outlook . The themes and topics discussed include: The performance of various markets and asset classes over recent years and since the onset of the Ukraine conflict. Fri, 03/18/2022 - 06:42. Watch the Video.

This is Masters in business with Barry Ritholtz on Bloomberg Radio 00:00:17 [Speaker Changed] This week on the podcast, Jeff Becker, chairman and CEO of Jenison Associates, they’re part of the PG Im family of Asset Managements. Jenison manages over $200 billion in assets. It was a, a great company.

One of the pre-market Bloomberg emails gave a positive mention to the Cambria Global AssetAllocation ETF (GAA) because it is up in what of course has been a tough tape for equities this year. It is an interesting assetallocation that targets 40% in equities, 40% in fixed income and 20% in alternatives.

What to Do Instead: Stick to fundamentals: Learn about assetallocation, risk management, and diversification before investing. Keep it separate: Use a high-interest savings account or liquid mutual fundsbut not your main spending account. Use it only for real emergencies: If you have to ask, Is this an emergency? ,

Benefits of Waterfall Wealth Management Managing significant assets can be complex. Wealth preservation – Protects assets while allowing for strategic investments and philanthropy. Tier 2: Allocates funds to retirement accounts and family support. Peace of mind – Offers clarity and confidence in financial decision-making.

A reader asks: If Bill Sweet’s favorite topic is Roth IRA’s/401K’s, I’d bet his second favorite is tax gain harvesting (in a taxable account). For 2024, individuals with taxable income below $47,025 ($94,050 for married couples) pay 0% tax for long-term capital gains (LTCG).

Your assetallocation is the percentage of your portfolio that you distribute between different asset classes, like stocks and bonds. To rebalance your portfolio, you’ll buy and sell certain investments to realign to your accounts with your desired assetallocation.

Most investors pay close attention to their assetallocation. And that makes sense since research has shown that the asset classes a portfolio is allocated to drive the majority of its return over time. But assetallocation isn’t the whole story.

Did you know what account you place your investments in can make a meaningful difference in taxes over your investing lifetime? This is called asset location, and Vanguard has found that it can save you up to 0.60% annually in … Continued The post Asset Location appeared first on Financial Symmetry, Inc.

Perhaps it’s time to rebalance and to rethink your ongoing assetallocation. View all accounts as part of a total portfolio. This means IRAs, your 401(k) , taxable accounts, mutual funds , individual stocks and bonds, etc. Costs matter. Low cost index mutual funds and ETFs can be great core holdings.

We also discussed questions about Roth vs. traditional retirement accounts, the pros and cons of targetdate funds, retiring in your mid-30s and what to do about big gains in Mag 7 stocks. Further Reading: What’s the Investment Case For Gold?

Fully Utilize Tax-Advantaged Retirement and Savings Accounts There are multiple steps you can take using retirement accounts to reduce your taxable income. Contribute to Tax-Advantaged Retirement Accounts Do your best to fully contribute to one or multiple tax-advantaged retirement accounts, such as 401(k), 403(b), or IRAs.

Review risk tolerance and current assetallocation strategy It’s important to ensure your clients’ portfolios align with their risk tolerance because taking too much risk can negatively impact their ability to navigate market fluctuations. You can help them start the year right by conducting a retirement checkup.

This strategy gives individuals the opportunity to reinvest in comparable but not “substantially identical” assets (as defined by the IRS), and maintain a similar portfolio exposure. The tax treatment of this loss will depend on how long the asset has been held. All of this adds up to a total tax saving of $5,550.

Take advantage of tax-advantaged retirement accounts such as 401(k)s, IRAs, and Roth IRAs to maximize your contributions and benefit from tax-deferred or tax-free growth. Aim to contribute as much as you can afford to these accounts each year to accelerate your retirement savings. Learn more about retirement plan options here.

Depending on your financial situation and the type of asset you inherit, your options may differ. Inherited cash, stocks, or a brokerage account. Inheriting money or taxable investment accounts has some big benefits. Further, many beneficiaries are eligible for a step-up in basis on eligible assets. What not to do?

Do-It-Yourself trend-following assetallocation weights for the Robust AssetAllocation Index are posted here. Note: free registration required) Request a free account here if you want to access the site directly. If you are an advisor and want help implementing our models, please get in touch with Ryan Kirlin.

Their role extends beyond investment managementthey can help with: Retirement Planning : Structuring your assets to support your desired lifestyle. Risk Management : Protecting assets from unforeseen events. Provide insights on assetallocation and risk management. Guide decision-making during uncertain times.

In today’s economic climate, I recommend maintaining 6-9 months of living expenses in easily accessible accounts. If your employer offers a Roth 401(k) option, evaluate whether splitting your contributions between traditional and Roth accounts might benefit your long-term tax strategy.

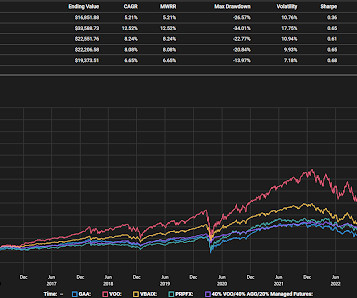

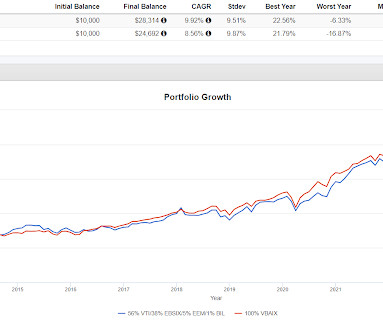

which accounts for about half of it's total outperformance since inception. Circling back to model ETF portfolio mentioned at the top of this post, the assetallocation was as follows. Right out of the starting block for GHTA, VBAIX fell off a small cliff and GHTA managed to avoid that decline.

I created this list of financial advisors for small accounts (less than $300,000 in assets) because there are alot of schmucks out there hawking crap products to people with portfolio of this size, and I don’t think it’s fair. Transform Retirement www.transformretirement.com Avg account size: Approx.

Do-It-Yourself trend-following assetallocation weights for the Robust AssetAllocation Index are posted here. Note: free registration required) Request a free account here if you want to access the site directly. If you are an advisor and want help implementing our models, please get in touch with Ryan Kirlin.

Do-It-Yourself trend-following assetallocation weights for the Robust AssetAllocation Index are posted here. Note: free registration required) Request a free account here if you want to access the site directly. Our Advisor portal is available [.]

Many people invest in their company-sponsored 401(k)s but only sometimes take the time to review the investments within the account. Rebalancing involves adjusting the mix of assets in your 401(k) portfolio to maintain a desired level of risk and return. Click to compare vetted advisors now. What is 401(k) rebalancing?

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content