This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

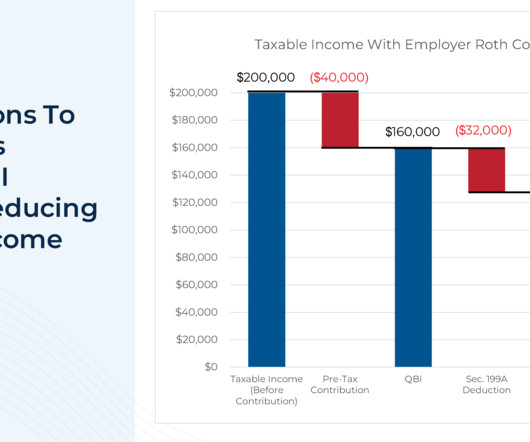

By maximizing both the employee employer contributions, solo 401(k) plan owners can often save significantly more than is possible with other types of retirementplans available to self-employed workers, like SEPs and standard IRAs. a nondeductible contribution that can be converted to Roth tax-free). 199A deductions.

One of the best tax deductions for a small business owner is funding a retirementplan. Beyond any tax deduction you are saving for your own retirement. You deserve a comfortable retirement. If you don’t plan for your own retirement who will? You need to start a retirementplan today.

Also in industry news this week: A recent study suggests that while a majority of financial advisory clients surveyed have only had 1 advisor, deteriorating client service is a key risk factor that could sway certain clients to leave for a different advisor RIA M&A activity in 2024 is poised to surpass the total number of deals seen in 2023, according (..)

Which means that financial advisors can play an important role in adoption planning – helping clients strategically plan for the costs involved in the process, including accessing tax credits that can significantly defray these expenses. Read More.

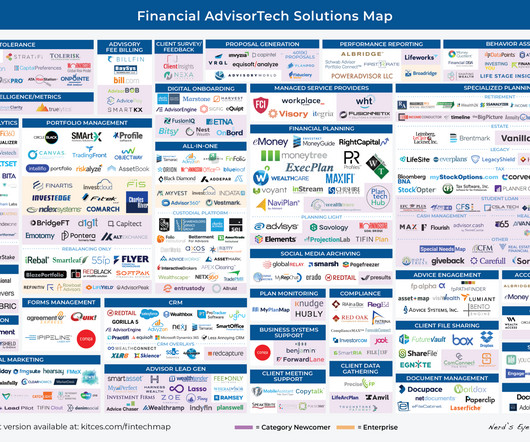

Welcome to the May 2023 issue of the Latest News in Financial #AdvisorTech – where we look at the big news, announcements, and underlying trends and developments that are emerging in the world of technology solutions for financial advisors!

Each week in Weekend Reading For Financial Planners, we seek to bring you synopses and commentaries on 12 articles covering news for financial advisors including topics covering technical planning, practice management, advisor marketing, career development, and more.

(citywire.com) Creative Planning is expanding its reach in the retirementplan space. papers.ssrn.com) Taxes A 2023 year-end taxplanning guide. citywire.com) Choreo is buying the wealth management business of BDO USA. investmentnews.com) M&A The RIA model continues to take share.

Unlike most types of retirementplans, the SEP IRA is funded by the employer. Here’s more on what a SEP IRA is, tax benefits, contribution limits, and important deadlines. The SEP IRA is a straightforward and cost-effective way for small business owners to save for retirement. What is a SEP IRA?

(morningstar.com) Banking Eight questions about the banking panic of 2023 including 'Is my money safe?' wsj.com) RetirementRetirementplanning is a moving target. humbledollar.com) Retirement is, in part, about declaring career victory. humbledollar.com) Retirement is, in part, about declaring career victory.

A new bill would make many parts of the Tax Cuts and Jobs Act of 2017 permanent, including its changes to tax brackets, the higher standard deduction, and the cap on state and local tax deductions. What advisory firms can do to make the most out of client testimonials and avoid negative reviews on third-party websites.

The IRS has released the 2023 contribution limits for retirementplans and other cost-of-living adjustments. The agency also released tax brackets for ordinary income and long-term capital gains. Contribution Limits for 401(k)s, IRAs and More in 2023. Income Tax Rates in 2023.

A recent study shows that while many consumers have expressed an interest in ESG investing, such funds within retirementplans have received limited allocations from investors. ” to pass by the end of the year, while passage of other proposed tax measures appears to be less likely.

Even though retirees have contributed throughout their careers, a portion of those benefits could still be taxed, depending on your total income. Here’s how it breaks down for 2023-2024: If a couple’s total retirement income is between $32,000 and $44,000, up to 50% of Social Security benefits could be taxable.

”, a series of measures that will have significant impacts on the world of retirementplanning. While RIA M&A activity has been red hot during the past couple of years, a survey suggests that advisors are expecting lower valuations in 2023.

There are many important birthdays when it comes to retirementplanning. So, as you approach your retirement, it’s crucial to have a few of these in mind as key milestones. 1] But you can begin to claim at 62 if that fits into your financial plan. 1] But you can begin to claim at 62 if that fits into your financial plan.

As April 15th approaches, taxpayers across the country are gearing up to fulfill their annual obligation – filing taxes. Whether you’ve already submitted your returns or are yet to tackle the paperwork, now is the perfect time for a tax check-up. Other Resources Should I do my own taxes?

It is March…that means you have just about 5 weeks left to get organized and submit your tax return. The tax deadline is April 18, 2023 (some taxpayers in disaster areas in California, Georgia and Alabama have an extended deadline). Gathering all your documents is crucial to complete a tax return free of mistakes.

How you handle taxes and when you are taxed are two of the most important factors when it comes to retirementplanning. There are also Roth 401(k)s that have a similar tax treatment but are subject to some different rules.

That must mean it’s time to roll up my sleeves and get to work on year-end financial planning – with an emphasis on 2023 income tax. One consideration this year is that we’re two years from the expiration of the Tax Cuts and Jobs Act of 2017 (TJCA). AGI impacts multiple other tax considerations.

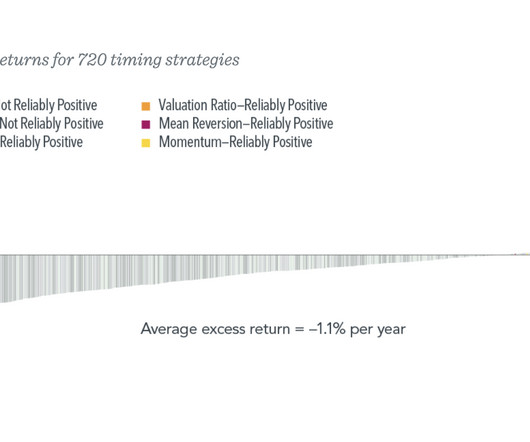

This is before we get to the issue of capital gains taxes, which create a hurdle of (minimum) 20% on those pesky profits just to get to breakeven. When you get it wrong, it crushes your retirementplans. Let’s add some color to the discussion on timing itself and add a little nuance.1 By Jeff Sommer New York Times, Nov.

In November 2022, proponents of the Massachusetts ‘millionaires’ tax (question 1) won their bid to nearly double the income tax rate on individuals with taxable income over $1M a year. Starting in 2023, a 4% surtax will be applied to taxable income and capital gains over $1M. They paid $300,000 for the house.

As you plan for retirement, it’s important to consider tax optimization strategies to minimize your tax liabilities. Here are three key ways to optimize taxes in retirement, based on information from sources published between 2022 and 2023.

Key Takeaways: 2023 could be a really good year to fund a Roth account because of low tax rates and changes to how the standard deduction, tax brackets, and retirement account contribution limits are adjusted for inflation. Plus, you’ll be increasing your tax diversification for retirement.

To be eligible for financial aid (grants & student loans) for college your child will need to submit your tax return as part of their FAFSA application when applying to colleges in their senior year. So…if your child is a sophomore in high school right now…2024 is the tax year that will be used for financial aid eligibility.

And how does it compare to the 401k and other retirementplans that exist? A Simple IRA, or Savings Incentive Match Plan for Employees, is a type of employer-sponsored retirement savings plan that is designed to be easy to set up and maintain for small business owners. What is a Simple IRA?

A major decision in retirementplanning is whether to make pre-tax or Roth (after-tax) 401k contributions. Pre-tax contributions go into your retirement account with money that has not been taxed, and then taxes will be paid when the funds are withdrawn in retirement.

While they do share some similarities, there are enough distinct differences between the two where they can just as easily qualify as completely separate and distinct retirementplans. Either plan is an excellent choice, particularly if you’re not covered by an employer-sponsored retirementplan. Not exactly.

In 2023, healthcare spending in the U.S. With medical inflation outpacing general inflation, ignoring healthcare in your retirementplan is a risk no one can afford. Factoring in retirement healthcare costs is a smart move. Below are 5 things you can do for retirement healthcare financial planning: 1.

Congress is once again poised to make sweeping changes to the retirement and tax rules in the last two weeks of the year. retirement changes. In the new bill, the age when retirees must begin drawing from non-Roth tax-deferred retirement accounts would increase to 73 in 2023 and 75 in 2033. The Secure Act 2.0

Last year’s considerable losses and market fluctuations underscore the need for clients to assess their retirementplans to ensure it aligns with their objectives, financial situations, timelines, and attitudes toward market volatility. You can help them start the year right by conducting a retirement checkup.

Your 401(k) is a valuable part of your retirementplan, but it’s only one piece of the puzzle. . There are many benefits that come along with a 401(k,) including pretax or Roth 401(k) salary contributions (or both,) company matching, and tax-deferred accruals. The limit for 2023 is $6,500.

FINANCIAL PLANNINGTax and Financial Planning Ideas For 2023 Schedule a Complimentary Financial Review CLICK HERE TO SCHEDULE. Additionally, the government has made changes to tax rules, further prompting Americans to reevaluate their tax and financial strategies. Retirement Savings Accounts .

As we look forward to 2023, the IRS recently announced that the contribution limits for employer-sponsored retirementplans are going up. You may want to review your contribution amounts and adjust for January payrolls if your goal is to maximize funding your retirementplan contributions. . Tax Loss Harvesting.

Here are some things to consider as you weigh potential tax moves between now and the end of the year. Defer income to next year Consider opportunities to defer income to 2024, particularly if you think you may be in a lower tax bracket then. Doing so may enable you to postpone payment of tax on the income until next year.

If you think retirementplanning moves stop at retirement, think again. Although it won’t make sense in every situation, retirement can be a unique opportunity for Roth conversions for some investors. For high earners, converting an IRA to a Roth IRA while you’re still working could be the worst time of all.

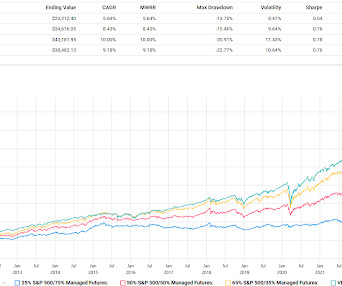

Every now and then we talk about expat living as part of a retirementplan, usually the context is an underfunded retirementplan. Morningstar had an article about how well 60/40 did in 2023. Look at this table of how some diversifiers did in 2023. One popular country in expat living circles is Ecuador.

The stock market has returned an average of between 9% and 11% over the past 90 years and that’s the kind of growth that you’ll need to tap into if you want to retire at 50. Your retirementplan shouldn’t be. Get in touch with an Independent Financial Professional to see if you're on track to meet your retirement goals.

We talked at length in 2022 and into 2023 when managed futures was booming and people were coming out of the woodwork to suggest huge weightings to managed futures which I said was a bad idea back then and is a bad idea right now in terms of constructing a portfolio. In that light, 20% or 25% makes no sense to me.

In this guide, we explore the strategic and financial considerations of building a team for your tax firm, from understanding the hiring process to outlining the unique solutions that Harness Wealth can provide. Deciding Between an Accountant and a Tax Assistant The first hire you might consider adding to your team is another accountant.

That will give you a combined contribution of $13,000, which will also be fully tax-deductible. There's no time like the present to begin preparing for your retirement. When you turn age 72, you’re required to begin receiving distributions from the plan. Ads by Money. We may be compensated if you click this ad.

The investment service includes access to dedicated financial advisors and assistance with managing your employer-sponsored retirementplan. Advanced tax optimization strategies. Investment advice for employer-sponsored retirementplans. Investment advice for employer-sponsored retirementplans.

Tax-Advantaged Savings : Contributions to ABLE accounts are made with after-tax dollars, but the earnings on the account grow tax-free. Withdrawals are also tax-free if they are used for qualified disability expenses.

Portfolio 1 was way ahead in 2022, way behind in 2023 and 2024 but it was up nicely those years and this year it is way ahead. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. In 2021 it lagged the index by 12%.

This data can serve as a baseline for tailoring your retirementplan, taking into account factors such as inflation, your current age, and your desired retirement age. In the unfortunate event of your passing, the funds held in a 401(k) can be passed on to your heirs, offering them a tax-advantaged account.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content