This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Modern Wealth’s fourth deal of 2025, and 17th since its founding in 2023, adds a firm in its home state and bolsters a workplace retirement plan division launched last year via acquisition.

Enjoy the current installment of "Weekend Reading For Financial Planners" – this week's edition kicks off with the news that a recent report finds that the number of SEC-registered RIAs, the assets that they manage, and the number of clients they serve all increased between 2023 and 2024 and suggests the industry is robust across the size spectrum, (..)

As a result, financial advisors should start honing the services Gen X members will likely benefit from the most, including retirement planning, estate and tax planning and mortgage refinancing. As of year-end 2023, Gen X made up a quarter of U.S. In comparison, only 9% of advisors’ clients in 2023 were millennials or Gen Z members.

Whether it’s savings, retirement funds, or net worth, understanding where you stand can provide valuable perspective on your financial progress. 401(k) account contribution: 8.0% In 2023, Capitalize found the average employee-only contribution was 8%; the average dollar amount of employee-only contributions of $5,993.

Also in industry news this week: A recent study suggests that while a majority of financial advisory clients surveyed have only had 1 advisor, deteriorating client service is a key risk factor that could sway certain clients to leave for a different advisor RIA M&A activity in 2024 is poised to surpass the total number of deals seen in 2023, according (..)

That means if your retirement plan underestimates medical costs, you risk serious shortfalls. For instance, a retired government employee receiving a fixed monthly pension of ₹40,000 ten years ago might find its value significantly reduced today if inflation averaged around 6% annually. on June 6, 2025 , and cut CRR by 100 bps.

Solo 401(k) plans are a popular retirement savings vehicle for self-employed business owners. By maximizing both the employee employer contributions, solo 401(k) plan owners can often save significantly more than is possible with other types of retirement plans available to self-employed workers, like SEPs and standard IRAs.

In 2023, he tweeted a list of overlooked facts. This was just before an 81% collapse that bottomed in December 2023. My buddy could pay off his mortgage and car loans, pre-pay the kids colleges, fully fund retirement accounts, and still have cash left over. The most devastating: 98% of all ARKK investors were underwater.

In 2023, he launched his own firm, Park Hill Financial Planning and Investment Management. “I I didn’t have $8 million that I could just write a check for,” said Brennan, who is 38 and has been advising for about 13 years after starting at Northern Trust in Chicago. “It " Brennan’s response?

Focus went public in 2018, and then private again in 2023 , when it sold to Clayton, Dubilier and Rice, and Stone Point Capital.) Dixon-James launched Resilient Wealth Management in 2020 and now manages about $250 million in advisory, brokerage and retirement plan assets. His team was previously with Osaic for 12 years.

Healthcare costs are rising at a pace that demands attention, particularly for individuals nearing retirement. In 2023, the United States’ National Health Expenditure (NHE) reached $4.9 Without proper planning, healthcare expenses can quickly consume a significant portion of retirement savings. increase from the previous year.

in 2023, according to a study by Ensemble Practice and BlackRock. July 9, 2025 23 Slides START SLIDESHOW hudiemm/iStock/Getty Images A big industry focus these days is on organic growth; many stress that if advisors can crack the code and grow their client base, they can gain a competitive edge. New client AUM grew on average 7.5%

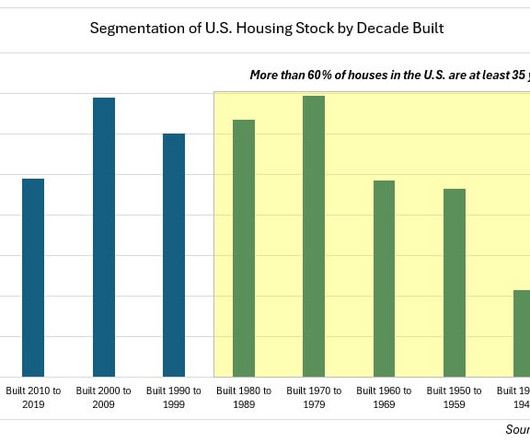

Remodeling / modernization : Many, if not most, of the homeowners electing to stay put are of the baby boom generation, now in their retirement years, and typically close to their peak wealth due to a long bull market in stocks, and with their houses most likely paid for.

It plays a crucial role in helping people achieve financial stability, prepare for retirement, and leave a lasting legacy for their families. A 2023 survey by Law Depot found that 73% of Americans didn’t have an estate plan. Mistake #5: Not accounting for tax implications on withdrawals Taxes don’t end when you retire.

Fully Utilize Tax-Advantaged Retirement and Savings Accounts There are multiple steps you can take using retirement accounts to reduce your taxable income. Contribute to Tax-Advantaged Retirement Accounts Do your best to fully contribute to one or multiple tax-advantaged retirement accounts, such as 401(k), 403(b), or IRAs.

The SEC previously tried to sue Coinbase for allowing the trade of unregistered crypto tokens in 2023, but dropped its case after its senior crypto policy advisor was demoted in January. The lawsuit alleges the firm pocketed millions in fees as it operated an exchange that sold unregistered securities.

Many advisors experienced record years in 2023 and 2024, but now is the time to ask the difficult question: Am I growing because of my firm, or despite it? Evaluate Your Environment The third part of the gut check is environmental: Consider whether your firm provides enough value to justify your continued partnership.

Since 2023, the of RIAs who have acquired CPAs include Allworth Financial, Mariner, Nepsis, Savant Wealth Management and Sequioa Financial Group. Most importantly, for the client, we give them a holistic view of what they are doing in the investment landscape, and how that impacts their tax life.”

Between FY 2021–22 and FY 2023–24, LRS-based outward investments in equities and bonds doubled—indicating rising investor interest in international diversification. Remittance strategies should be phased to manage currency risk, especially for education and retirement planning.

While the S&P 500 has had three losing years during the past decade, the average return from 2013 to 2023 was a positive 12.39%. Knowing this and setting long-term goals for your money retirement, education, etc. And the average annual return since the stock indexs inception is 10.26%.

As of the end of 2023, there were some 12,000 advisors affiliated with RIA consolidators, up from 4,000 in 2018, according to a recent report from Cerulli Associates.

based on 2023 data: 2 In-home care: Home health aides typically charge around $27 to $30 per hour. The cost of long-term care can vary depending on the type of care needed, the location and the length of time care is required. Below are some average costs in the U.S., 1 CNN, “More than half of older Americans will need long-term care.

Are you thinking about cashing in on your Roth Individual Retirement Account (IRA) early? This article will help you understand the rules around a Roth IRA early withdrawal and walk you through what to consider before tapping into your retirement savings early. And over time, this affects how much you have for retirement.

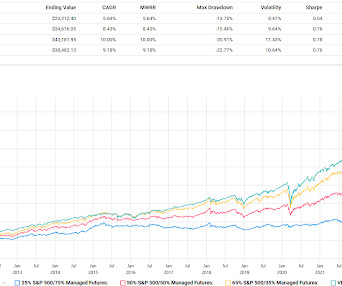

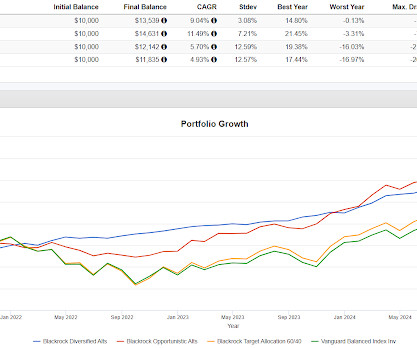

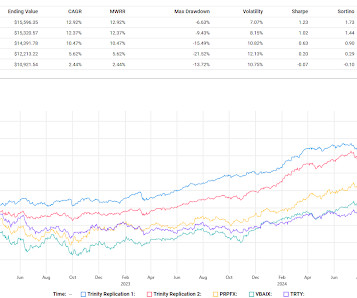

Certainly 2023 was tough for these funds but while managed futures didn't do very well in 2024, the funds generally kept up with VBAIX. Looking at the three I mentioned versus 60/40 proxy, VBAIX, you can see that the difficulty of holding managed futures during bull markets mostly disappears. And the year by year MBXIX is curious.

Here’s how it breaks down for 2023-2024: If a couple’s total retirement income is between $32,000 and $44,000, up to 50% of Social Security benefits could be taxable. This is why having a smart, well-rounded retirement plan that includes income planning and tax planning is so important! appeared first on Talon Wealth.

We talked at length in 2022 and into 2023 when managed futures was booming and people were coming out of the woodwork to suggest huge weightings to managed futures which I said was a bad idea back then and is a bad idea right now in terms of constructing a portfolio. In that light, 20% or 25% makes no sense to me.

So I, I love this quote from the book over the 20 years ending in mid 2023, investing in a broad based US total market equity fund produced net returns better than more than 90% of professionally managed stock funds that promised to beat the market. And then there’s several pages that are half blank.

The post How Do You Turn Retirement Savings into a Reliable Income Strategy? How Do You Turn Retirement Savings into a Reliable Income Strategy? You’ve likely spent years building your retirement nest egg—saving diligently, investing wisely, and contributing to retirement accounts along the way.

The performance going back to June, 2023 has the two Dalio portfolios outperforming by a mile along with higher standard deviation. It can be difficult to sit with things that go down for an extended period. I shortened the performance to last May to take out any huge gains from the crypto holdings.

Data from the Federal Reserves 2022 Survey of Consumer Finances (SCF) (released in late 2023) offers the most recent comprehensive snapshot of American household wealth. In contrast, the typical (median) household is far more concentrated in home equity and retirement savings, with limited exposure to stocks or private business ownership.

And I think even, you know, in 2024 I saw a significant uptick in issuance versus 2023. And has just, you know, over time she’s retired now from JP Morgan, but sort of, you know, become a friend. 00:30:17 [Speaker Changed] So we are definitely optimistic on the IPO market this year.

Portfolio 1 was way ahead in 2022, way behind in 2023 and 2024 but it was up nicely those years and this year it is way ahead. In the partial year of 2020, Portfolio 1 was down 83 basis points while the S&P was up 18%. In 2021 it lagged the index by 12%. It has throw in the towel at the wrong time written all over it.

The outperformance isn't solely because of 2022, VOO/BALT outperformed in partial year, 2021, 2023 and 2024. Using BALT instead of AGG has given a higher compounded return with less volatility. This year it is trailing a little bit.

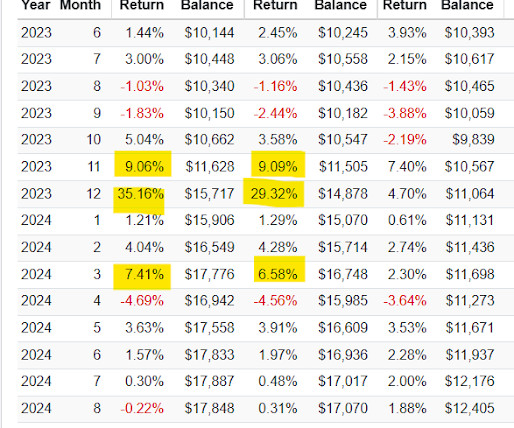

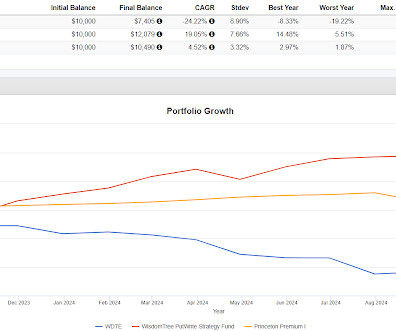

Portfoliovisualizer missed $9 worth of dividends from 2023 and the payout for this year isn't completely missing but does seem a little short. WDTE hasn't done as poorly as it appears. There was a name/symbol change and it switched to paying weekly instead of monthly.

in October 2023, bottoming out at 3.6% At the start of the year, there were a lot of calls to buy further out the curve because with all of these Fed cuts coming, rates were going down they said. There turned out to not be that many Fed cuts and bond yields have churned around quite a bit with the 10 year treasury peaking at 4.9%

Keefe, who joined CoastalOne in June 2023 and led the firm through the rebranding, recently resurfaced at Independent Financial Group , a privately held independent broker/dealer in San Diego, as president and chief operating officer. Legacy is currently listed as a director and chief compliance officer at TradePMR, public filings show.

The Bloomberg article included a couple of quotes about dialing down the equity exposure in retirement which has been the default approach but that chart shows why dialing down is a bad idea. The simplest example would be the person to retired at the end of 2007 and then 12 months later, the stock market was 39% lower.

Inventories were the reason why prices rose in 2023–2024 despite falling home affordability. Some of this has gone to offset the fact that defined benefit pension plans have greatly declined, with business focusing more on defined contributions to retirement accounts instead. Inventories were low, and that drove prices higher.

Here are some examples of the impact: 1 In 2023, Americans donated $557.16 We sometimes see this when families are in their peak income-earning years with retirement on the horizon. It provides us the opportunity to support causes we believe in and make a positive impact. Keep in mind, giving isn’t always about donating money.

The next time equities take off, I don't think they would keep up but Opportunistic Alts was way ahead of 60/40 in 2023 and slightly ahead in 2024. Diversified Alts and Opportunistic Alts are intended to differentiate from 60/40 and I'd say they do that.

So by 2023, when we finally get back to normal production, you have three, almost four years of new car production down substantially worldwide. My dad was in the military, so we lived all over the place. You know how quickly an energy price increase can bleed through into, you know, broader consumer good categories.

Advisors can also adjust their offerings to meet client needs, such as adding tax or retirement planning tailored to each clientâs circumstances. Many human advisors leverage the same technological resources, but they add a layer of human emotion and understanding to deliver personalized recommendations.

All three lagged by a lot in partial year 2021, lagged somewhat in 2023, lagged by kind of a lot in 2024 and this year has been slightly favorable. The results are of course compelling but as we've talked about a couple of times, what is the flaw or the thing to look for? I think the great results in 2022 are skewing the entire backtest.

Shortening the study where I am getting this data to the start of 2023 still shows the fund being relatively volatile for something with more of an absolute return type of result. That might not be a useful way to look at though as the fund currently owns a lot of ETFs that weren't around in 2020.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content