This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

I have made some fortuitously timed buys, including Nasdaq 100 (QQQ) calls purchased during the October 2022 lows. My buddy could pay off his mortgage and car loans, pre-pay the kids colleges, fully fund retirement accounts, and still have cash left over. I was up so much on that trade that my trading demons were emboldened.

When you get it wrong, it crushes your retirement plans. My own track record at making big calls is pretty damned good, but none of our clients wants me slinging around their retirement monies based on my gut instinct. But when they get market timing wrong, they lose subscribers. I sure as hell don’t want to either.

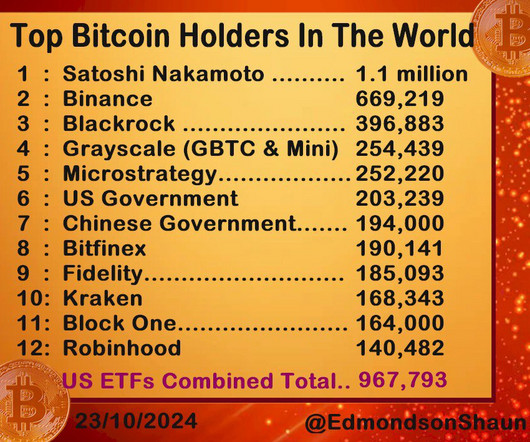

There were 127 million US households as of 2022. First, is the math right based on my numbers? That 40% could own Bitcoin makes no intuitive sense to me, I guess 20% is possible but that too seems a little high but who knows? So 25 million of them own a little Bitcoin worth a couple of hundred dollars?

For most, Social Security provides a solid foundation for retirement income. In fact, as of September 2022, over 70 million Americans were collecting benefits. [1] Let’s discuss how you can maximize your benefits and give yourself the best possible chance to live out the retirement of your dreams.

The fund owns a lot of puts and should go up a lot in the face of a crash but not necessarily a slow protracted decline like there was in 2022. According to Portfoliovisualizer, CYA dropped 46.10% in 2022. The fund in question is the Simplify Tail Risk Strategy ETF (CYA). Here's what caught my eye that it might have blown up.

The "endowment" result is very close to red line VBAIX every year except 2020 when it lagged by almost 600 basis point and 2022 when it outperformed by about 500 basis points. The portfolio did just fine, it captured most of the upside and avoided the full brunt in 2022's large decline.

And checking in on the GraniteShares YieldBoost SPY ETF (YSPY) that sells put spreads on a levered S&P 500 ETF; Yes, that is a rough start, clearly, but interestingly the math checks out. Then it made it back in 2022 when it was only down 1.1%. YSPY sells put spreads on a 3x fund.

So, if you owned $100 worth of bonds yielding 2% in 2022 you now own $90 worth of bonds yielding 5%. Since the Fed started raising rates in 2022 the annual interest burden on the national debt went from $635B to $1,025B. This is the basic math behind what’s happened to every consumer who owns these bonds.

And then just a little math, the "guarantee" based on the 50/50 allocation would be 2.5% Down less clearly worked in 2022 and YTD HEQT is lagging the S&P 500 by 400 basis points. Keep it to something broad like a total market fund or a market cap weighted large cap index.

The way Portfolios 1 and 2 are weighted, the math works for being a 60/40 portfolio and then from there we add portable alpha/capital efficiency/return stacking. It certainly had a relatively good 2022 when CPI jumped 8%. The idea here is to look to see if any value can be added. So does it work? Well yeah, maybe it does.

She has a really fascinating background, very eclectic, a combination of math and law. You, you get a, a BS in Mathematics and a JD from Boston University Math and Law. It is something, math has always come easy to me since a child. I didn’t get an advanced degree in math. Not the usual combination. What happened?

The math behind Universal Life Insurance Interest Rates is a twisted web and most consumers are deceived. Know how the math works so you can see the potential risks that may exist with your policy. Money market rates crashed to zero (0%) in 2022 due to Covid-19. Don’t be fooled! That is a mathematical impossibility.

A quick excerpt from a post a couple of weeks ago about retirement misconceptions. I would much rather withdraw 10% or more per year from my retirement accounts and do it without taking any principal. Part of the math that determines options premiums is the risk free rate of return from T-bills.

It has had a great 2022 but doesn't appear to have captured much upside coming into 2022. In terms of complexity, several of the funds blend together multiple complex strategies and the blend itself is complex in terms of the math applied and the outcomes sought, they are complex-complexity. It's multi-asset and multi-strategy.

In the case of real estate a 2.29% weighting and for "private equity" companies it's about 17 basis points (looked at XLF holdings and then did a little math), that's just not going to move the needle. You may agree with Jack about not needing those things, that's valid, my point is that owning an index fund isn't a proxy for them.

Here's how QYLD has done for the last 5 years coming into 2022, so before the market was underway, versus the NASDAQ. And here is 2022, the bear market. Similar to PUTW, it didn't offer protection during the pandemic crash of 2020 but only dropping half of what the S&P 500 index has dropped in 2022 is impressive and surprises me.

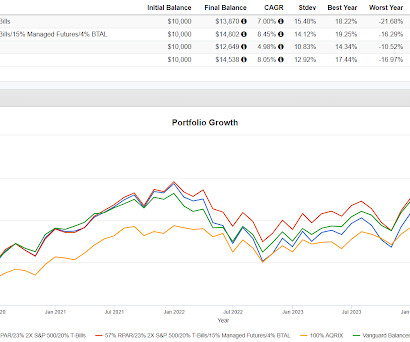

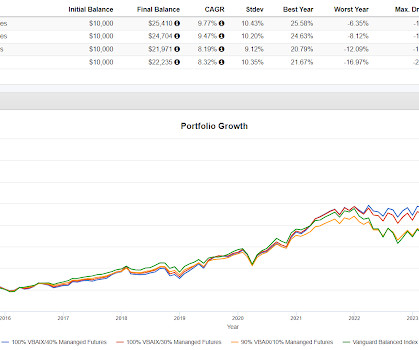

The way the math works, a 67% allocation to NTSX (Portfolio 2 with 33% in the T-bill ETF) equals 100% in Vanguard Balanced Index Fund (VBAIX) which is a proxy for 60/40 and Portfolio 3. Portfolio 1 is 100% in NTSX which in 2022 was down 25.84% versus down 16.85% for Portfolio 2 and 16.87% for Portfolio 3.

The authors noted that risk parity did very well for a long time but that "bond based risk-parity failed miserably in 2022." In fund form, it started doing badly long before 2022 which is corroborated by AQR's change to AQRIX in 2019. Both 2 and 3 were up in 2022 while the RPAR replication was down 11%.

Those of us called upon professionally to write about market performance in 2022 as the year ends are necessarily struggling for the right verbiage. That’s because, in language as plain as I can make it, pretty much every market and sector has had a very bad 2022. percent and 6-month T-bills are yielding almost 4.75

Despite the leveraged semiconductor ETFs, when blended with USMV, the portfolio is underweight technology versus the S&P 500 using simple math, it works out to about 26% versus closer to 40% for the S&P 500. They even did much better than 60/40 in 2022 dropping only low to mid single digits.

One, one is true and I’ve always said is that I wanted people to stop, ask if I could doing math. And no one asked me if I can do math anymore with a degree from Booth, particularly in econometrics and statistics. So people really ask you, you take French and can you do math. So I applied to Maryland State retirement.

From the company’s website, as of May 16th, 2022: Single people. From the company’s ADV Part 2 brochure, as of May 16th, 2022: Fees are set as a fixed annual fee, paid quarterly, and based approximately on the total time required to service an account yearly. Retirement Portfolio Partners. 375 start up. $89

Even Mr. Money Mustache, as a person who retired 17 years ago, is still in this boat for the simple reason that my retirement income from dividends and hobby businesses is still greater than my annual living expenses (which still hover around $20,000 per year). 3) Okay, but I really am retired and trying to live off my investments now.

Imagine the Intel scenario of down 59% on top of VBAIX dropping 16% in 2022. Most of the improved return can be attributed to 2022. A 20% drop in managed futures that is leveraged to a 40% weight would have added another 800 basis points to the decline (simple math). In 2008, VBAIX was down 23%.

I’d say management consulting is any of the other thing that least at that time was the other career trajectory, just my personality, more of a math oriented introvert. And that a bit of that cult, Dick and Ike are both retired now. And I very much get the sense he has no interest in retiring. Quality strategies in 2022.

However, by doing a little math, you can easily determine your hourly wage from your annual salary. The amount of taxes you pay will depend on several factors, including your filing status, job status, the state you live in, retirement contributions, and your income. State By State $55,000 a Year Salary After Taxes in 2022.

I — I loved math, but really, I was going to go down that literature route more than anything else and — and study Spanish literature. BITTERLY MICHELL: … difficult situations for those who were retiring, right, and those …. So heading into 2022, there surely were pockets of froth. I was econ and kind of geeky.

The way the math works, a 67% allocation to NTSX replicates 100% into a 60/40 portfolio which leaves 33% left over to do something. In 2022, VBAIX was down 16.87% while Portfolio 2 was only down 10.77%. In the 13 years between 2008 and 2022, VBAIX outperformed Portfolio 2 in six of those years with one year being a tie.

Markets have pretty much done nothing but roll over and head south in 2022. And I think that story still has some legs but sort of the key culprit then became demographics and retirement savers and the latest story now is in the sort of the one percent. Are we running the risk that they’re getting ahead of themselves in 2022?

And since 2022 is becoming a year of interesting financial changes, it’s time to spark things up again, go back to our roots, and start covering some of the many subjects that are cropping up in this latest incarnation of our economic world. I am a retired, married Navy veteran living in beautiful (but expensive) San Diego.

We dove in on the math at my old URL (sad story, no longer exists) and the math checks out. The benefit comes in a year like 2022, both managed futures funds are up 17% versus down 20% for the S&P 500. A long time ago I wrote about a portfolio concept derived by John Serrapere called 75/50.

It has to be such a different set, the retirement planning is different, the safety net is different. People in Spain when I was growing up in the ‘80s and ‘90s, they expect to just retire and have the government give them like a paycheck every month. How do you manage through volatility like we’ve seen in 2022?

With more money at our disposal, we maxed out our retirement accounts and invest in real estate, while we travel 12 weeks annually.” – Holly Johnson, Freelance Writer and Blogger at ClubThrifty.com Holly has become so successful as a freelance writer that she now offers a course helping others succeed on the same path.

Yahoo Finance had kind of a long read recapping an update from Morningstar about safe retirement withdrawal rates. I was little concern during 2022 with high inflation with the market downturn. I would much rather withdraw 10% or more per year from my retirement accounts and do it without taking any principal.

But the numbers you can’t argue with, I mean, we all know that the brutal math of investing before costs investors collectively will earn the market return after costs. I did it during the coronavirus collapse in 2020, and I did it again in 2022. I realized I had enough to retire if I wanted to. I did it in 2000, 2002.

We've talked just a couple of times about the market becoming increasingly concentrated which just in terms of math means that a diversified strategy will lag for as long as the big names do well. Despite outperforming for 15 years, PSLDX was down 43% in 2022 which speaks to what diversification is about. In 2022 they didn't work.

Let Mr. Market do his thing and we’ll find out how we did when we get ready to retire. So as much as I’m personally still a pretty strong skeptic of active management, I mean, I understand the math, and the odds are not in your favor. I read all those academic papers, I understand where the math comes from.

Unfortunately, we’re not quite there yet as a society, since as of 2022, the Bureau of Labor Statistics reports only a third of financial advisors are women. In 2022, nearly 42% of the externships participants were women. women tend to live longer, making it much more important to plan for a longer retirement) or a subjective one (e.g.

It is of course not dead but bonds became a far less effective diversifier years ago, long before 2022 when interest rates started going up. The risk was there for years, 2022 when when there was a consequence to investors who took that risk. I would say that is a very big bet but the math in their backtest supports it.

I got to imagine a year like 2022 wasn’t horrible for Vanguard’s asset growth. And when you saw the US Ag down 13% last year, for folks, again, who are investing for retirement and in their 529 plans, they’re not concerned about it. Go to the decade before 2022, the equity side was something like 13%.

There was a lot of content from various places over the weekend about whether it is time to go back into bonds, what retired investors should do for yield and even whether retirees are better off going 100% into equities. As a matter of math, it cannot repeat the run from 8.5% Barron's also noted that 60/40 was up 9.6% in November.

2022 was certainly a challenging year for a lot of the hedge fund industry and it really separates the winners from the also-ran. I’ll have to be when I retire and publish under Anonymous. The Financial Times did an article at the beginning of this year and it talked about aggregate losses for 2022 in the industry.

6:23 PM ∙ Jun 7, 2022 316 Likes 87 Retweets As if. I couldn’t make that math work at all plausibly. percent annualized since 1927 (1928-2022), including dividends, and 9.69 percent over the past 30 years (1993-2022), that is a very bold claim. percent from 1965 through 2022, compared with 9.9

So I took it upon myself to go off and took a course in bond math, took another course in derivatives and realized the underlying fundamental concepts were barely, I mean, it wasn’t even high school math in most cases. RITHOLTZ: So you mentioned earlier 2022 was so unusual. SALISBURY: Sure. SALISBURY: Yes. SALISBURY: Yes.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content