This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In this episode, we talk in-depth about how Griffin leverages his own experience as a firm founder to support his business-owner clients navigate financial planning decisions (in particular, tax planning opportunities), how Griffin encourages his business-owner clients to invest a portion of their profits outside of the business to diversify their (..)

The people who undergo an audit have been selected due to a number of red flags that the IRSs computer-based system has detected. In this article, well examine the nature of IRS audits, the common audit red flags that result in IRS scrutiny, and how professional tax advisors can help reduce the risk of you being audited.

The recently released Bank of America Global Fund Manager Survey showed a record number of participants who intend to cut US exposure, as shown in the chart below. The survey also showed the largest two-month jump in cash since April 2020 and the 4 th highest recession expectations ever.

Lagging the market cap weighted SPY doesn't have to be a bad thing but the max drawdown numbers are not compelling and neither is the volatility. Yes the dividend funds did better than SPY in 2022 but not 2020 and in the financial crisis, I believe DVY was the only one that was around and being heaviest in financials, it did very badly.

Emotional Drivers and the Stories We Tell Ourselves The urge to build a large cash cushion isn’t just about numbers; it’s deeply emotional. There’s also recency bias at play: The market downturns of 2022 and the COVID-19 shock in 2020 linger in memory, making us forget the equally compelling history of market recoveries and long-term growth.

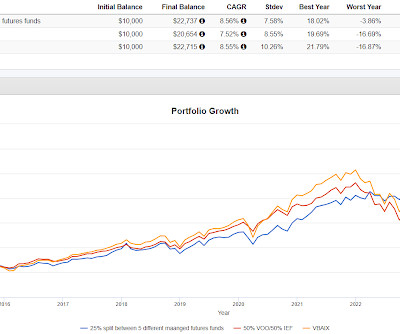

Portfolio 1 does not keep up with portfolios that have close to a normal allocation to equities but that portfolio was less volatile, did have an adequate real return and had much smaller drawdowns except in the 2020 Pandemic Crash. Another important observation is that Portfolio 1 is truly differentiated from 60/40.

We pulled together some information and interesting facts about some of the major indexes that can help you put the numbers you hear in context. In time, the DJIA itself would evolve, and the concept of stock indexes would grow in number, size, and importance. It’s not the number of points that matters—it’s the percentage change.

Along the lines of the 75/50 portfolio that captures 75% of the upside with only 50% of the downside (run the numbers, they work), the result of Portfolio 1 is in the same neighborhood. In the partial year of 2020, Portfolio 1 was down 83 basis points while the S&P was up 18%. In 2021 it lagged the index by 12%.

Many noted how the 2022 midterms came in much closer to expectations and that maybe this time so would the presidential election, but this is yet another election involving President Trump that saw his eventual numbers come in better than expected, similar to 2016 and 2020. when President Biden won in 2020.

It's growth rate since inception is 3.58% going back to September, 2018 but a lot of that comes from a 15% lift in 2021 (numbers per testfol.io). It had a big drawdown in the 2020 Pandemic Crash which, ok, something like that sure but it had a surprisingly big drawdown in 2022 as you can see at 13%.

Investors of course love dividends but share buybacks and debt reduction are more tax efficient than dividends which are taxed at ordinary income rates. It offered no crisis alpha though in the 2020 Pandemic Crash and in 2018 it was down 13.5% I threw in the Schwab US Dividend for context. versus 4.5% Now as a diversifier.

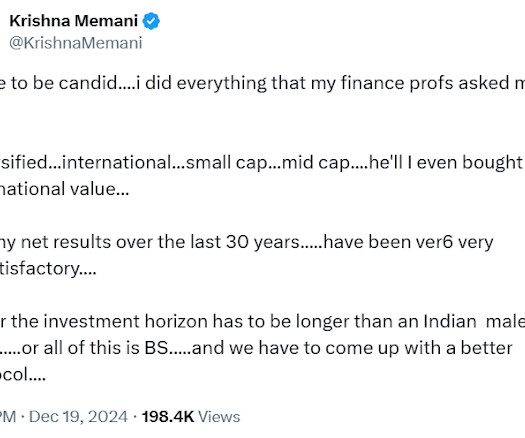

That leads to a Tweet from Krishna Memani who worked at Oppenheimer for a long time and who has been running the Endowment at Lafayette College since 2020. The min vol version is valid longer term but 2020 would have been a challenging time to hold. Adding some asymmetry would add one or two more to that number.

trillion in change and we think that number is gonna get to six by the end of the decade for the industry. 00:15:23 [Speaker Changed] Yeah, it, and it’s a number of things and, and we’ve talked about these trends. Not quite sure where, why that focus shifted to ETFs, but it was ETFs and probably a number of other things.

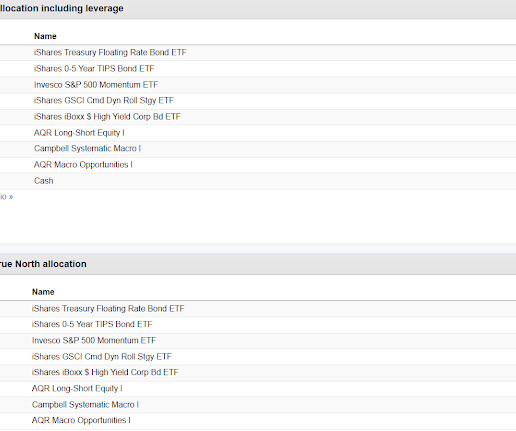

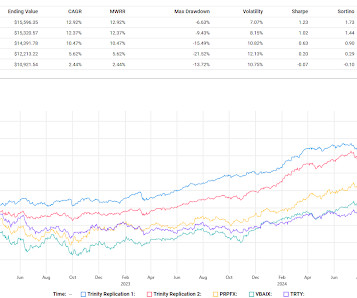

Both True North portfolios also held up relatively well in the 2020 Pandemic Crash which are the max drawdown numbers in the chart. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. It's only down year was 2018 with a decline of 7.91%.

Have some number of month's worth of expected expenses in cash or cash proxies and have some of the portfolio allocated to first responder defensive holdings, like BTAL for me, and some of the portfolio in second responder defensives like managed futures. It's very simple.

Barry Ritholtz : The the funny thing is, the behavioral aspect of mutual funds seems to have been when people finally learn about a manager who’s put up great numbers, by the time it makes to make makes it to Forbes, hey, most of that run is probably over and a little mean reversion is about to kick in. I did it in 2000, 2002.

In 2022 it was only down 3.32% which is really good of course but in the 2020 Pandemic Crash it fell 20%. That might not be a useful way to look at though as the fund currently owns a lot of ETFs that weren't around in 2020. The trend following number appears to include a 7.94% weighting in Cambria Value and Momentum ETF (VAMO).

He pegged that number at 25% or 33% but conceded even 5-10% could help. All five funds really struggled from 2015-2020 but there was variation among the five. Kurtosis captures susceptibility to adverse outlier events and lower is better with this number. We looked at a similar chart the other day. and and VBAIX is 0.69.

If youre planning a move, keep these three priorities in mind: Taxes Does your new home state have an estate/inheritance tax? Could other state tax laws affect your strategy? The biggest shift in estate planning in decades came from the 2017 Tax Cuts and Jobs Act, signed by President Trump during his first term.

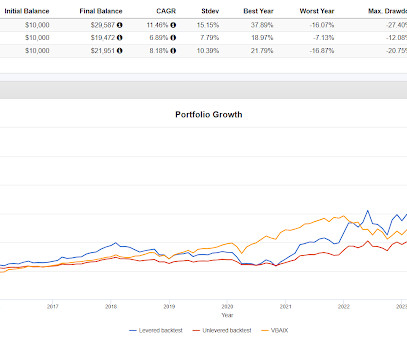

There's very little difference in the Calmar Ratios between the leveraged and unleveraged versions but both were much better than VBAIX while the kurtosis numbers were far inferior to VBAIX. None of them helped though in the 2020 Pandemic Crash. Going the leveraged route has better returns but more volatility.

But the heart of the firm was still on the private client side for any number of strategic reasons. And later on, we had a number of the discount brokers had come out in places like Schwab and Muriel Seabert, but I always felt they had followed Meryl’s lead to Absolutely. And the number came out and it was a blowout good number.

We learned everything, you know, across from accounting to auditing to, to tax and valuation. 00:05:36 [Speaker Changed] And I just wanna emphasize, we’re not talking the beginning of the pandemic in 2020. So that, that number ultimately is about 40 billion of our 150 billion of equity. They, they trained them together.

The 2022 numbers are of course favorable but they did get hit hard in the 2020 Pandemic Crash. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. This isn't radically different from a lot of ideas we look at.

Number 8860726. 2025-47, a Tax Court denied the estate of a Kentucky decedent a marital deduction for a bequest, finding that it wasn’t qualified terminable interest property (QTIP) because a QTIP election wasn’t made. 1, 2020, Martin’s executor filed an estate tax return, Form 706. Registered in England and Wales.

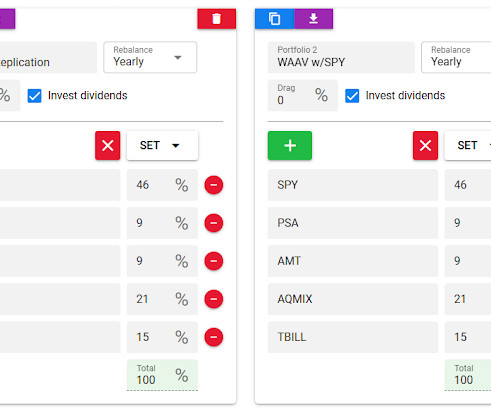

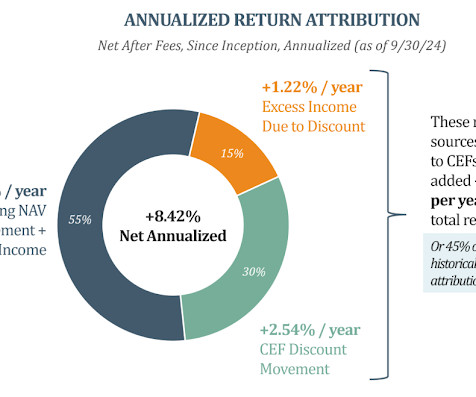

Closed end funds (CEF) have a fixed* number of shares. They have a net asset value (NAV) per share but because the number of shares is fixed, the market price that closed end funds trade at can vary significantly from the NAV. Matisse has a couple of funds of closed end funds that we've looked at before. in 2022 is a solid result.

From the MBA: Share of Mortgage Loans in Forbearance Decreases Slightly to 0.38% in February The Mortgage Bankers Associations (MBA) monthly Loan Monitoring Survey revealed that the total number of loans now in forbearance decreased by 2 basis points from 0.40% of servicers portfolio volume in the prior month to 0.38% as of February 28, 2025.

You sit in a room all day doing tax returns or something, it’s just not, you know, that it seemed antisocial. The book comes out in June, 2020, instant acclaim, New York Times bestseller list. So number one on the New York Times list? So the book publishes June, 2020. And I thought, what do you do?

There are a number of people who have said, and I’ve been swayed in this direction, Hey, when you’re 20, 25 years old and you don’t need this money for 30, 40, 50 years, do you really need bonds to offset the volatility of equities? Some crazy number writing a monthly column for them. You can’t execute.

The way we've talked about that here is to think about setting aside an amount of cash to correspond to some number of months of expenses you feel comfortable with. If we stop the back test at the end of 2020, Portfolio 3 compounded at 9.64%, 50 basis points better than VBAIX but the standard deviation was only eight basis points lower.

Dates like the lows in 1982, 2009, and 2020 show up this time, which always catches our attention. Those numbers could have bulls smiling later in 2025. Early 1987, March 2009, August 2011 (after the US debt downgrade), and the COVID lows in March 2020. Two Huge Days The S&P 500 soared 9.5%

When we do these exercises, I'm not really trying to find something that will compound miles ahead of plain vanilla, the objective is more about smoothing out the ride and trying to build a portfolio that will have a robust result in the face of a market event like in 2022 or maybe even a fast decline like the 2020 Pandemic Crash.

In that post, I noted that the next recession would likely be caused by one of the following: " An exogenous event such as a pandemic , significant military conflict, disruption of energy supplies for any reason, a major natural disaster (meteor strike, super volcano, etc), and a number of other low probability reasons.

They count the bond vigilantes, hard money advocates, Milton Friedmanites, Fed haters, goldbugs and crypto bros amongst their numbers. A three-year production shortage of new cars means today we have a shortage of used cars – at least the vintages that would have been normally produced in 2020, ’21, and ’22.

Of 12 fast corrections since 1970, only COVID 2020 led to a full bear market. 1st quarter GDP numbers. Nothing in these materials is intended to serve as personalized tax and/or investment advice since the availability and effectiveness of any strategy is dependent upon your individual facts and circumstances.

From the MBA: Share of Mortgage Loans in Forbearance Decreases Slightly to 0.36% in March The Mortgage Bankers Associations (MBA) monthly Loan Monitoring Survey revealed that the total number of loans now in forbearance decreased by 2 basis points from 0.38% of servicers portfolio volume in the prior month to 0.36% as of March 31, 2025.

He was like the guy, like number one in ii right. So you can pretty much tell right away whether the number was good or bad or whatever else, right? You think about like the, the biggest names in research sales over the last number of decades. And you have ongoing increases in like the number of discouraged workers, right?

The FIRS number may not be accurate because the last trade was right before the Powell presser. In the 2020 Pandemic Crash, PUTW went down in lockstep with the S&P 500 but in 2022 it was only down 10% versus 18%. The first group are permanent-ish portfolio funds. I am including HFND here but thought of it after the fact.

Number 8860726. Resonant Capital Merges with Tax, Accounting Firm QBCo $2.2B Resonant Capital Merges with Tax, Accounting Firm QBCo $2.2B Over 57 million individuals are currently over age 65, and that number will climb to an estimated 88 million by 2060. Registered in England and Wales. Since 2007, the U.S.

I grew up there, but in a, in a number of other countries as well. Not just a recession, but a depression was very conventional wisdom in 2020 that this would take many years to recover. Is this, have we been through more than the usual number of shocks or does it just seem that way recently? I’m not American.

At the Money: How to Pay Less Capital Gains Taxes (January 24, 2024) We’re coming up on tax season, after a banner year for stocks. Successful investors could be looking at a big tax bill from the US government. On this episode of At the Money, we look at direct indexing as a way to manage capital gains taxes.

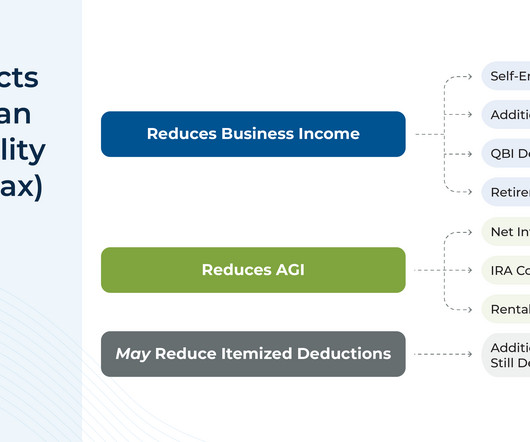

The 2017 Tax Cuts & Jobs Act introduced a $10,000 limit on the State And Local Tax (SALT) deduction that was previously available for taxpayers who itemized their deductions. Another set of considerations involves owners of businesses that operate in multiple states, which can compound the complexity of electing a PTET.

The four largest drops occurred during distinct periods of economic distress: 1990 (recession), 2006-09 (GFC), 2020 (pandemic/recession), and today (FOMC 300 bp rate hike). The current collapse is to a measure of 25, from a November 2020 peak of 77; the pandemic saw a fall to 13 from 58, and the GFC saw a collapse from 55 to 7.

The number of delinquent properties, but not in foreclosure, is down 209,000 properties year-over-year, and the number of properties in the foreclosure process is up 31,000 properties year-over-year. in Washington to 21.5% in Washington to 21.5% in Washington to 21.5%

At least one person1 has noticed the risks to young consumers of social media: Since August 2020, @TikTokInvestors has been curating the most outrageous money-losing and dangerous videos culled from the “financial experts” at TikTok. Not if you spend tax season on a boat! The advice ranges from wrong to risky to criminal: -401ks?

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content