This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

After a strong finish in 2020 and very solid returns in 2021, we’ve seen a lot of market volatility so far in 2022. Ideally you’ve been rebalancing your portfolio along the way and your assetallocation is largely in line with your plan and your risk tolerance. The S&P 500 index was down about 17.6%

If one stock makes up more than 10% of your overall assetallocation, it’s probably too much. A diversified portfolio is the cornerstone of a risk-adjusted investment strategy. Diversifying Around It: Balancing the portfolio by investing in assets that offset the concentrated position’s risk.

It has been my experience when reviewing portfolios that diversification is typically expressed simply as a number of various stocks owned, or owning a handful of asset classes, usually stocks of various sizes and geographies, and bonds of varying maturities.

Kansas City won the 2020 game and the market had an up year in spite of the impact of COVID-19. What impact have the solid stock market gains of the past three years had on your portfolio? Perhaps it’s time to rebalance and to rethink your ongoing assetallocation. View all accounts as part of a total portfolio.

Their focus is on generating alpha with high conviction concentrated portfolios. As you, as you may recall, the insurance companies had huge commercial loan portfolios in those days that they were using to backstop long dated life insurance liabilities. Jenison launched way back in 1969 as a growth equity shop.

My back-to-work morning train WFH reads: • Big Investors Are Giving Up on Crypto Markets Going Mainstream : Bitcoin as a portfolio diversifier hasn’t worked for investors Crypto won’t ‘find a home in institutional assetallocation’. Bloomberg ). Wall Street Journal ). • Morningstar ). Institutional Investor ). USA Today ).

After a significant drop in March of 2020 in the wake of the pandemic, the S&P 500 has staged an amazing recovery. The index finished 2020 with a gain in excess of 18%. However, some of the folks who experienced losses well in excess of the market averages were victims of their own over-allocation to stocks. Click To Tweet.

Torsten Slok blogged about how ineffective bonds have been in terms of providing any return or diversification benefits lately in the context of a 60/40 portfolio. Based on the following excerpt; I built out the following leveraged allocation, taking some liberty with shortening the duration quite a bit.

The more exciting your portfolio, the worse your performance is in this bear market. This is in stark contrast to the FOMO days of 2020 and 2021 when it felt like the only place to put your money was the. Boring is better this year in the markets.

1 Consider this : from 1980 to 2020, the S&P 500 experienced average annual drops of approximately 13.7 Even during more severe events like the 2020 COVID crash, the market dropped over 30 percent, only to recover within six months and reach new highs. A diversified portfolio is designed to help manage risk during market cycles.

There's no fact sheet yet and while the holdings are available, the assetallocation is vague without calculating the spreadsheet yourself which I did (hopefully correctly). It did decline about 5% in the 2020 Pandemic Crash and in 2022 it was up 1.36%. The backtest runs from the start of 2011 to the end of 2020.

The starting point today is the that Rational ReSolve Adaptive AssetAllocation Fund (RDMIX) has gone through a strategy change, renaming as the ReturnStacked Balanced Allocation & Systematic Macro Fund and keeping the same symbol. " balanced allocation and $1 of exposure to a systematic macro strategy."

MDCEX is in Morningstar's Tactical AssetAllocation (TAA) category and the Fidelity info page for the fund offers the following comparison to other funds. Looking at how it has actually traded though, yes more volatility and you can see in the chart it got pasted in the 2020 Pandemic Crash (poor first responder?)

GAA stands for Global AssetAllocation and it has been lagging for 15 years. That leads to a Tweet from Krishna Memani who worked at Oppenheimer for a long time and who has been running the Endowment at Lafayette College since 2020. Referencing the weightings above, all of the portfolios have 65% in equity beta.

MCW also did great in 2021, 2020 and 2019. A portfolio with an enormous weighting to one or two broad based factors is not really what I do but it clearly can work but just like any other strategy you can find, it won't always be optimal. Speaking of AI, Grok seems to like the portfolio. Occasionally of course, MCW gets pasted.

Considering Climate within Portfolios ajackson Mon, 10/04/2021 - 11:00 An increasing number of investors are seeking to incorporate climate change in their investment calculus. For investors with a portfolio covering multiple asset classes, the tasks of excising climate risk and finding new climate-related opportunities can be daunting.

Considering Climate within Portfolios. For investors with a portfolio covering multiple asset classes, the tasks of excising climate risk and finding new climate-related opportunities can be daunting. Mon, 10/04/2021 - 11:00. A 360-Degree Climate Evaluation.

The idea of building an All-Weather portfolio of course has its appeal. The basic idea is to be much less volatile than the broad market or the typical 60/40 portfolio. It raises the question though of how much performance should an investor expect or be willing give up for the potential emotional comfort of an All-Weather portfolio.

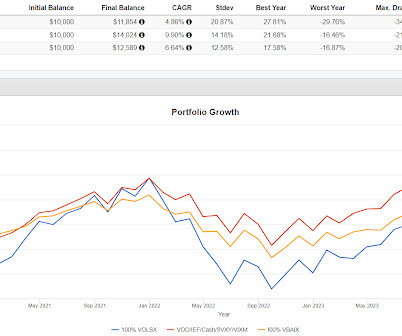

Some other alternatives do their own thing in such a way that they complement equity exposure to reduce volatility and drawdowns without lowering the long term growth of the portfolio. It offers this pie chart to show its current assetallocation. The time frame is so short because VOLSX only goes back to 2020.

AssetAllocation The Discipline Index is our core benchmark index and has an average duration, as measured in the Defined Duration strategy , of 10 years. This created an unusual distortion in the weighting of US tech stocks so our global market cap target resulted in adding more value to the portfolio.

It is in some ways a welcome reminder that prudent portfolio construction is a delicate balancing act that should strive to be as agnostic about the future as possible since it seems that the risks we too often discount are those that present the gravest dangers.

Indian households traditionally invested most savings in physical assets. However, financial assetallocation increased recently. Its revenue surged from ₹3,508 crore in March 2020 to ₹14,780 crore in March 2024. It increased from ₹1,885 crore in March 2020 to ₹8,306 crore in March 2024. in March 2020 to ₹167.79

In this piece, we are trying to understand what the future holds and how we can prepare our investment portfolio to deal with future outcomes. The liquidity support since 2008 and massive stimulus post March 2020 has inflated all the asset prices be it equity, debt, or real estate. But first a quick recap. trillion to ~$8-8.5

Rodrigo and Mike manage the Rational/Resolve Adaptive AssetAllocation Fund (RDMIX). The fund is a mix of risk parity (there's more to it which we'll get to) as a base, the primary portion of the portfolio. It is certainly multi asset, not sure that it is true risk parity versus having been influenced by risk parity.

Equities and traditional fixed income with nothing else can absolutely get the job done provided the savings rate is adequate, the assetallocation is suitable and succumbing to emotion is avoided. Here's how VIXM and RYMFX did during the 2018 Christmas Crash; And here's the Covid crash in 2020.

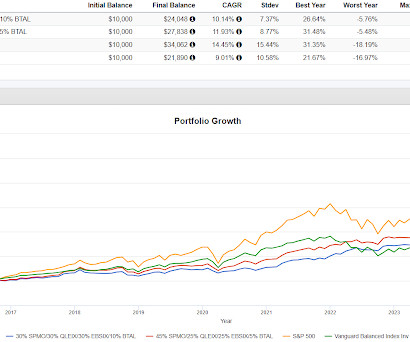

That reality can change some of the calculus between endowments and individual investor accounts but there are things we can learn from their assetallocations all the same. If bonds were already in a positive trend like they were in the 2020 Pandemic Crash then managed futures will do well. BTAL went up of course.

When surveyed in 2020 after the onset of the COVID-19 pandemic, advisors indicated that 85 percent of their clients who had a financial plan felt more prepared to weather market volatility than those who did not. When portfolio values fall, that loss can cause intense feelings that could lead to irrational decisions.

As with many things in life, the truth is somewhere between the extremes: While both simulated and real-world data suggest momentum may not be suitable as a driver of long-term assetallocations, we believe momentum considerations can be integrated in a cost-effective way to help inform daily portfolio management decisions.

The key to weathering the storm is having a diversified assetallocation that’s truly aligned with your risk tolerance and appetite before there’s a personal financial problem or other negative event. Assetallocation. Having a diversified portfolio can increase the odds of staying the course.

A little less dramatic but more interesting is the idea we broached yesterday about extreme portfolio simplification becoming an appropriate assetallocation for an older retiree who is not cognitively impaired but wants to spend less time on their investments without hiring someone to help them.

The most recent doubling took just four years from the week of April 5th, 2020 to where we are now which again is very short. Since we cannot know the path, this really spotlights a couple of important portfolio management concepts. There's no prediction being made here. That doesn't have to mean cash.

We have seen strong, strong demand pretty consistently for building out alternatives, portfolios, particularly when it comes to opportunities with great financial sponsors on the private equity side, looking at these long-term secular trends, right? RITHOLTZ: Let’s talk a little bit about inflation. You mentioned 8.5 percent inflation rate.

Over the last few days I've fished around looking at multi-asset ETFs that I perceive are intended to be either one fund, portfolio solutions or the major core holding with a little room left for maybe alternatives or thematic exposures or whatever. By my count it has not quite 60% in equities, 21.5% in cash, almost 6.5%

I specifically refer to people’s “investment” portfolios as their “savings” portfolios because the financial markets are not where we make real investments. 1 The financial markets are where we allocate our savings. 1 – See “The Total Portfolio” perspective.

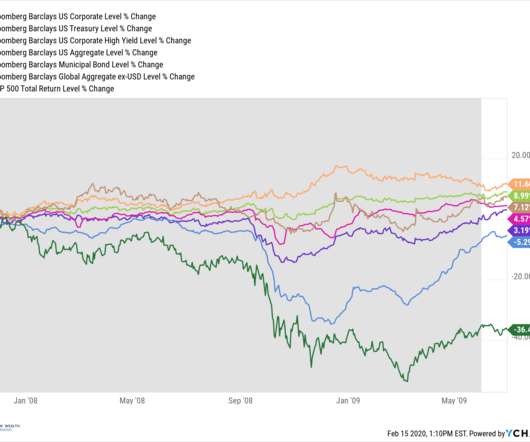

The LPL Research Strategic and Tactical AssetAllocation Committee is increasing its recommended interest rate exposure in its tactical allocation from underweight to neutral. from its August 2020 lows and has already seen the biggest move higher in yields since 1987, when rates moved higher by 3.2%.

Her job is portfolio and product solutions and that means she could go anywhere in the world and do anything. I thought this conversation was absolutely fascinating and I think you will also, with no further ado, Goldman Sachs asset managements Elizabeth Burton. That sounds great, but I only have spots in my portfolio for a Cape Cod.

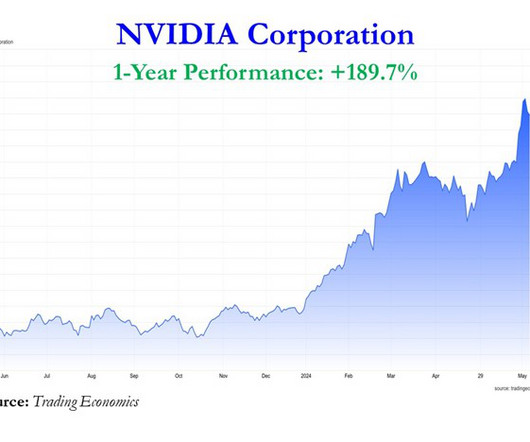

Artificial Intelligence Grabs the Spotlight Jake Bleicher, Portfolio Manager To me, the narrative of 2023 is captured by a chart showing the performance of NVIDIA, the maker of high-end computer chips that have become the bedrock of artificial intelligence (AI). in October 2022 and causing a heap of pain since the summer of 2020.

Remember that global pandemic back in 2020 called COVID-19 that killed over 350,000 people in the U.S.? What did the stock market actually do in 2020? Short-term news cycle headlines shouldn’t drive portfolio decision-making, but rather your personal objectives, goals, and risk tolerance. GDP was advancing at a reasonable +1.9%

Not understanding the role & importance of tactical assetallocation (overweight debt in euphoric times and overweight equity in a time of acute pessimism) in creating superior returns over the long term. While benchmark Sensex is down by more than 25% in the last one year, our portfolios returns are in the range of 0% to 5%.

They need some amount of time to show they can deliver on a quarterly result but I think these would be the best tool for building any sort of capitally efficient portfolio, with idea being to avoid the complexity of multi-asset funds. This is the most recent assetallocation I could find from Harvard.

At Carson Investment Research, we have moved our longer-term strategic assetallocations to their maximum equity overweight while continuing to favor U.S. That period includes two bear markets, in 2020 and again in 2022. That is why we seek to control risk in our portfolios. Here’s why. 31, 2018, through Dec.

Early today the Rational/ReSolve Adaptive AssetAllocation Fund (RDMIX) sent out it's monthly report providing an update on how things are going. RDMIX is a multi-asset and I would say multi-strategy fund that uses a lot of sophisticated strategies along with some amount of leverage. I enjoy their portfolio theory content.

In this brief paper, we will touch on what we believe are some of the most important issues and questions—including the different types of assets, return potential, fees, liquidity, diversification, volatility and transparency—that investment committees must understand as they weigh adding alternatives to their portfolios.

In this brief paper, we will touch on what we believe are some of the most important issues and questions—including the different types of assets, return potential, fees, liquidity, diversification, volatility and transparency—that investment committees must understand as they weigh adding alternatives to their portfolios.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content