This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The 4% rule is generally the accepted standard for a safe withdrawal rate in retirement to ensure the assets last for 30 years. Bengen retired as a financial advisor in 2013 but he also considers himself a researcher. He basically ran the numbers for someone retiring in 1926 and then each each up into the 1970's.

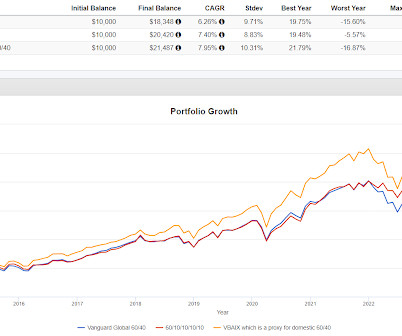

If we take out Portfolio 2 to get a longer look, we can see back to 2013 and the stats again look pretty good versus VBAIX. The volatility goes up some versus VBAIX but the gain in return seems to be worth it at least as far as the Sharpe Ratio is concerned.

Plenty of other managed futures funds came onto the scene in 2013 and 2014 but I think RYMFX is the only one to test what was a terrible time for managed futures. To my knowledge, RYMFX was the first managed futures mutual fund and it had the space to itself for several years after in launched in 2007.

The S&P 500 hit 1500 in March 2000, then again in the fall of 2007 and then the third and final time in January, 2013. Most of us of course lived through that from 2000 through to 2009. That's a long time for a broad based index to not make any progress.

EBSIX' worst 12 month stretch was a decline of 13% from June 2013 to June 2014. There is no reason anyone trying to implement some variation of this needs to put such a huge weighting into just one fund, EBSIX in this case, for the macro component. While that is not a catastrophic number, it's a visible risk that seems easy to mitigate.

When you get it wrong, it crushes your retirementplans. My own track record at making big calls is pretty damned good, but none of our clients wants me slinging around their retirement monies based on my gut instinct. But when they get market timing wrong, they lose subscribers. I sure as hell don’t want to either.

Feelings of fear, anxiety, and insecurity are common for women around the topic of retirementplanning. According to TIAA’s just-released Financial Wellness Survey, the research points out that only about a third of women (31%) are saving for retirement, compared to 44% of men. Women and money as it applies to the household.

Some recent, high-profiles examples include: In 2013, the billionaire creator of Beanie Babies pled guilty to tax evasion and faced FBAR fines of roughly $53 million. military banking facilities; certain bank-to-bank settlements; accounts owned by certain retirementplans. government is a member; accounts in overseas U.S.

Then from about 2013 to 2016, gold struggled and so too did PRPFX. The ten year numbers are awful for PRPFX because gold went down for about 4 years from 2013-2016. Both are multi-asset but PRPFX obviously allocates to precious metals and where you see the two funds diverge, those divergences coincide with big moves in gold.

When you get close to retirement, you know what will matter? What will matter is whether you have enough to retire to the lifestyle you want plus maybe having some sort of margin for error in your accumulated savings. Sure, I'm $200,000 short of my goal but you know what, I beat the market five years in a row from 2009-2013."

I used to own TIP but then figured out the interest rate problem back in what I am guessing was about 2013. I've known about this fund but didn't realize it has been around so long, back to 2013 despite only having $20 million in it. They may have inflation protection but they also assume interest rate risk. in I can't figure it out.

stock market didn’t completely recover from the 2008 financial crisis until well into 2013. Usually those goals involve a retirementplan, and you shouldn’t ever invest more than you’re prepared to lose. Forbes offers 3 pieces of advice to increase future wealth, on the assumption that the economy will take some time to rebound.

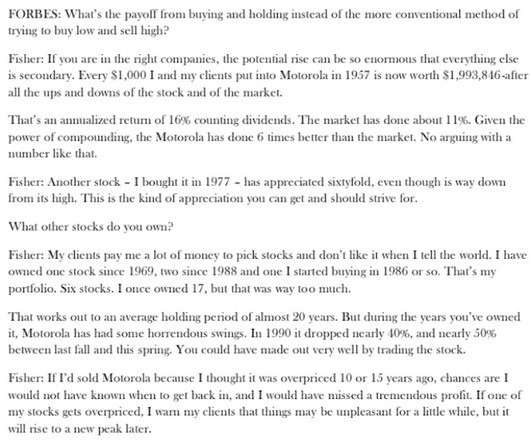

Coincidental to the Fisher quote, I bought client holding Motorola Solutions (MSI) in 2013. The Nvidia example ties right in with the Fisher quote. Let's look at a couple of stocks compared to the S&P.

Yeah, that lot that talks about terms like compounding, risk profile, returns, retirementplanning, budgeting, Investing, and whatnot! Inception Date December 02, 2013 Exit Load (0 to 90 days) 0.5% Expense ratio 0.74% Inception Date January 01, 2013 Exit Load 0.00% No. 1-yr Return 0.14% Expense Ratio 0.44 1-yr return 2.5

Some historical examples include June/July 2003, the Taper Tantrum in 2013 and of course now we can add 2022 to this list. The fund yields 9%, Portfoliovisualizer tests back to 2013. As a result of the leverage, when bad things happen in income markets and bonds go down, CEFs usually go down a lot more.

During the Taper Tantrum in 2013, both low volatility funds underperformed but that was also a very short term event. YTD they are both holding up much better than the S&P 500. During the 2020 Pandemic Crash, SPLV did a little worse than the S&P 500 and USMV did only slightly better but neither offered protection.

Some recent, high-profiles examples include: In 2013, the billionaire creator of Beanie Babies pled guilty to tax evasion and faced FBAR fines of roughly $53 million. military banking facilities; certain bank-to-bank settlements; accounts owned by certain retirementplans. government is a member; accounts in overseas U.S.

Given that MCN went up during the Taper Tantrum of 2013, I lean toward thinking it was equity beta. I wouldn't be dissuaded if it was a matter of equity beta but probably would not want to take on interest rate risk with this product.

AGI includes all taxable income, including wages, bonuses, taxable interest, dividends, capital gains, retirement distributions, annuities, rents and royalties. This is a significant increase over the rate for long-term gains rate of 15% for the highest bracket prior to 2013.

It's not as old as DVY, XYLD only goes back to 2013. It has plenty of income of course, no equity upside to speak of which doesn't have to be bad but it does capture a lot the downside. In the 2018 crash it went down 14%, in the 2020 Pandemic Crash it went down 32% and in 2022 it went down 12%.

In 2013, she applied it to the small number of privately held companies with a market value over $1 billion to denote their rarity. Uber, arguably the best known, first became a unicorn in mid-2013, about the time Ms. Most have achieved their unicorn status rather recently, and in fact nearly all did so in just the past five years.

For instance, events like a market downturn in June 2013 allowed some services to capture losses promptly, providing tax savings for clients. If you are retired, you must make sure that your financial advisor possesses a strong understanding of Social Security taxes. Need a financial advisor?

I did in 2013 the largest banking transaction that the market had seen since the financial crisis, it was a $2.4 It has to be such a different set, the retirementplanning is different, the safety net is different. I had the chance to be part of some very interesting transactions in the banking space. billion deal.

Opening a Roth IRA can be a smart move if you want to invest for retirement and save money on taxes later in life. When you’re ready to take distributions from your Roth IRA in retirement (or after age 59 ½), you won’t pay income taxes on your distributions, either. Retirement Account Conversions Allowed.

Because retirement accounts are tax-sheltered, it makes little sense to include municipal bonds in those accounts.). It has provided a return of 1.67% in the 12 months ending May 31, and an average of 12.33% per year since the fund began in October 2013. In general, growth stocks work best for retirementplans.

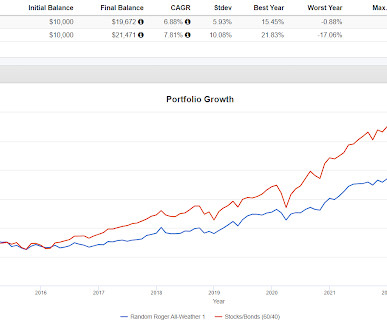

In 2013, both of them missed out on a very good year and then they've each taken turns completely missing out in other years. If you compare both to 60/40 starting in 2009, stripping out the great year of 2008, 60/40 compounded at 9.54, All-weather at 6.08% and PP at 5.96%.

LGBTQ+ adults were not legally permitted to marry their romantic partners nationwide, nor receive the 1,100+ legal benefits and protections that come along with marriage, until the United States Supreme Court’s Windsor and Obergefell decisions in 2013 and 2015, respectively 3.

So built in a retirement offering an insurance offering, expanded their mutual fund offering, expanded their ETF offering. We were fortunate enough to launch in 2013, which was a great, you know, start of a new bull market and a great decade ahead of it. It was great. Great job to have 00:06:17 [Speaker Changed] Choice is good.

As we know, the detrimental impact of reduced annual earnings compounds over time, which negatively impacts LGBTQ+ individuals financial futures and planning. Retirementplanning. Another way to help with retirementplanning is making sure your clients have a life insurance plan. Planning for Children.

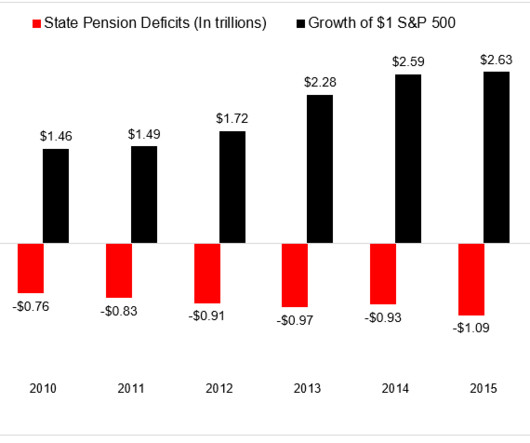

From February 2013 to November 2016, there were 3.6 The median retirement account balance of people ages 56 to 61 is just $25,000. People aren't saving enough in their defined contribution plans (401(K), IRA), and defined benefit plans (pensions) are in serious danger. That is no longer the case."

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content