This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Also fire related, Walker Fire will be upgrading one of our water tenders (2000 gallon water truck) in the next year or so and I'd be able to take that out if we needed. Anyone relying on their portfolio to make their retirementplan work probably needs a "normal" allocation to equities.

As a Retirement Income Certified Professional and a Life and Annuities Certified Professional, John advises clients on retirementplanning, investment planning, and risk management. His primary focus is to help people align their financial decisions with their values and truths to live enriching lives.

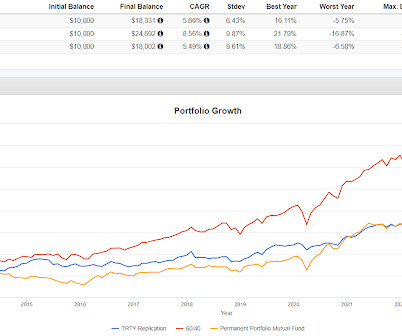

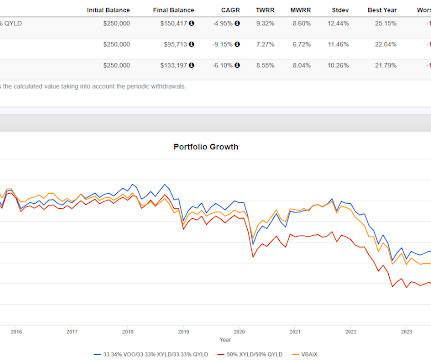

From 2000 to 2019, Swensen outperformed 14 times. And plugging into Testfol.io which goes back further and comparing it to VBAIX. Swensen did better over the course of the backtest with a little more volatility and bigger drawdowns. From 2020 on, VBAIX outperformed four times.

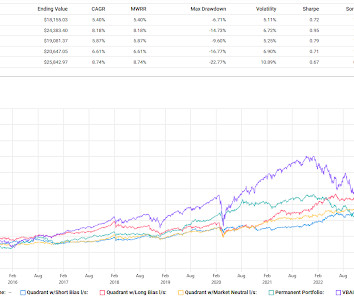

We had a lost decade from 2000-2009 but there were several years that stocks went up kind of lot. In 2022, that blend was down 89 basis points so some drag (PRPFX did worse than BLNDX that year) but not problematic. Portfolio 3 is sort of close to what we blog about regularly.

If you're 85 and very fit but out of money, whether you outperformed from 1990 to 2000 means nothing. If you're 50 and only have 1/3 of what you should have by now, you're not going to outperform your way up to where you should be. A very volatile portfolio increases the likelihood of panicking or making some other behavioral mistake.

10,000 invested on November 30, 2000 would have grown to $50,820 according to testfol.io. Having an allocation to something that moves like that makes sense in the context of constructing a diversified portfolio but going heavy into that sort of volatility is a panic sale waiting to happen. Going back 24 years, VBAIX compounded at 6.99%.

Most of us of course lived through that from 2000 through to 2009. The S&P 500 hit 1500 in March 2000, then again in the fall of 2007 and then the third and final time in January, 2013. That's a long time for a broad based index to not make any progress.

If you put 3% into Ariba Networks into a diversified portfolio in 2000 or bought a house you could comfortably afford in 2007 then you had a setback but weren't blown up. I posted the above joke on Bluesky a few days ago. This person will get blown up if anything bad ever happens, absolutely destroyed.

Sidebar, if you were in markets in the late 90's into the early 2000's, that last line might remind you of Alberto Vilar saying that Yahoo was going to be the next Yahoo.

PKW has been about 2000 basis points better than SYLD. Shareholder yield and buybacks tracked very closely to each other which makes sense until very recently. Early on SYLD lagged MCW badly but PKW was pretty close until it wasn't. There should be times where it is the best too but value investors have been waiting a long time.

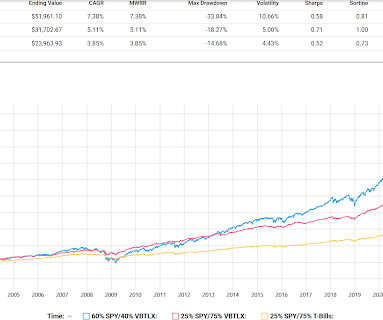

From March, 2000-March, 2003 the S&P 500 negatively compounded at 13.95%. The driver of this result of course is that 2 and 3 avoid the volatility of bonds with duration that funds like AGG and VBAIX will take on. Knowing what to avoid can be more important than knowing what to include.

The second backtest also cuts out the lost decade of the 2000's. Actually, the lost decade up until the end of 2007 was pretty good for this concept using 25% into ULPIX instead of SSO. So the problem was the Financial Crisis, this idea unravels holding through the financial crisis.

At 50, having $200,000 in retirement savings is far from rich but it is not nothing, that would be a useful piece of money and it wouldn't have taken a crazy high income starting in 2000 to have that much now. According to Copilot, $240/mo at an annualized 6% would be $200,000 today.

If this couple planned it out well, maybe their $2000/mo mortgage gets paid off right as they are retiring. Hopefully they're saving a little bit, call it 10% or $10,000 and their net is $75,000 (a little more than that for the tax not owed on their 401k contributions).

Get out a spreadsheet, list your fixed expenses, list out what you typically spend on discretionary stuff, add it all up and pad it by $1000 or maybe $2000 depending on how lucky you are/are not with one-off expenses like vet bills, new tires and all the rest of things like that. That's the number you need to cover.

Rams) won in 2000 and the market dropped. Related Posts: Five Things to do During a Stock Market Correction Is a $100,000 Per Year Retirement Doable? Some notable misses for the indicator include: St. Louis (an old NFL team that was formerly and is now again the L.A. Photo credit: Flickr.

These are target date funds with a range of target retirement date options and levels of risk. The Microsoft 401(k) retirementplan offers many excellent choices among actively managed and index funds. The Plan is subject to change by Microsoft. Please see your latest Plan document for the most up-to-date information.

Brian shares what he tells clients about investing and retirementplanning. For instance, Tom Brady, the greatest of all time, was 199 th pick when he was drafted in 2000. Similarly, investors who want to plan their own retirement might pick stocks based on emotions that they later regret.

Financial advisors spend the majority of our careers understanding the financial aspects of retirement; has the client saved enough to sustain through the remainder of their lives, is there a risk that they may “overspend” their plan, and what unforeseen risks may come their way as they navigate the next 20-40 years of their lives.

Somewhere around 1999 and 2000, television started to change. Before Netflix and streaming services pumped out shows as 8-hour binges, the following shows of the early 2000s began to set the groundwork for popular shows like Game of Thrones and Stranger Things. They turned television into a medium for long-form, poetic storytelling.

If we're thinking about risk planning for the next ten years, I might wonder about a lost decade for US equities like we had from 2000-2010 and whether that might mean foreign equities rotate back into favor like they were back in 2000-2010. It's good to start thinking about these things ahead of time.

Articles Analysts have the second highest set of future earnings expectations for growth stocks since 2000. By Patrick O'Shaughnessy Expecting companies to sponsor retirementplans is like demanding that a dog dance; it may comply, but neither well nor happily.

When you turn age 72, you’re required to begin receiving distributions from the plan. This is always true when neither you nor your spouse are covered by an employer-sponsored retirementplan. The numbers are different if you’re not covered by an employer-sponsored retirementplan, but your spouse is.

We've looked at these a couple of times over the years, back in the 2000's I accessed the space through a closed end fund that had a high yield, higher than what the space typically offers, thanks to the leverage inherent in the closed end universe.

That period ending in May 2000 was relatively bad for PRPFX. I'd argue it all worked out in the end but imagine how you might handle being that far behind in early 2000. That would not have been easy of course there was no way to know how well gold was about to do to help PRPFX catch up over the next few years.

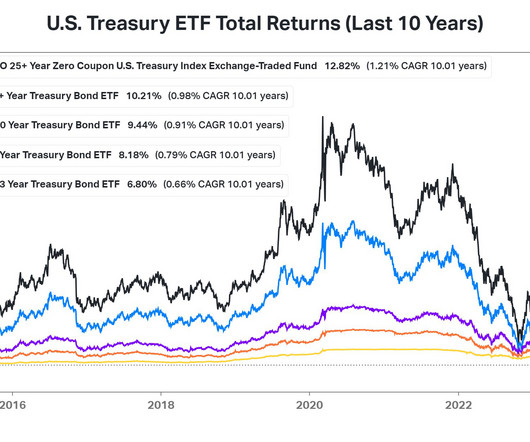

Unlike the decade long round trip to nowhere for equities in the 2000's, bond ETFs don't necessarily need to go back to where they were. I've seen a couple of references to a big, really big, round trip in price for fixed income ETFs. That image is from Stocktwits. Notice the CAGRs.

There are less than 2000 people in India who have qualified CFP. RetirementPlanning Course – Retirementplanning is gaining huge popularity among Indians. High disposable incomes and high-spending lifestyles have been encouraging Indians to plan for their retirement to ensure they continue to live their dreams.

Additionally, the study found that from 2000 to 2023, benefits under Social Security COLA increased by 78% or 3.4% In 2023 terms, the retiree would only be able to purchase $64 of goods and services that would have bought $100 worth in 2000. annually, while overall goods and services purchased by retirees rose 141.4%

Additionally, the study found that from 2000 to 2023, benefits under Social Security COLA increased by 78% or 3.4% In 2023 terms, the retiree would only be able to purchase $64 of goods and services that would have bought $100 worth in 2000. annually, while overall goods and services purchased by retirees rose 141.4%

There was an odd and I believe inaccurate emphasis on workplace retirementplans pivoting from defined benefit plans (pensions) to defined contribution plans (401k) starting around the turn of the century. People entering the workforce in 2000 were not the 401k guinea pigs. That is Rooster. Rooster loves duck toys.

What would that do to people's retirementplans? If 2000 was fool me once and 2008 was fool me twice, what would 2019 be? The United States has experienced just six distinct bear markets since The Great Depression: 1929, 1937, 1969, 1973, 2000, and 2008. What would happen if stocks crash?

Yes, there is absolutely the possibility that the period that someone needs to do this looks like the 2000's or maybe David Kostin of Goldman Sachs will turn out to be right about 3% annualized growth over the next 10 years. But what retirementplan doesn't need some level of resilience in the face of some sort of adverse market sequence?

In the 80's and 90's domestic outperformed, for most of the 2000's foreign outperformed and we are now in a 12 or 13 year run of domestic outperforming. In the 2000's I was much heavier in foreign than I have been for the last 10 or 12 years.

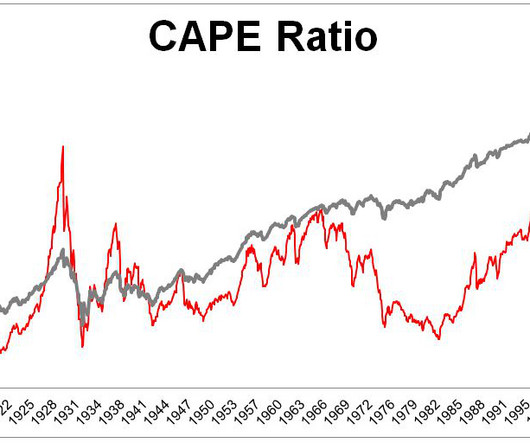

while the average CAPE since the year 2000 has been over 25." With millions of Americans shoveling money into their retirementplans every month, there is a much greater demand for stocks than their was in the first half of the twentieth century. The average CAPE for the decade immediately following WWII was 12.4,

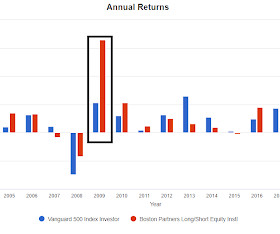

In 2000, BPLSX outperformed by 69%, in 2001 it outperformed by 37%, 22% in 2002 and 46% in 2009. That is not a bad result but might be less than you'd think when looking at the CAGR numbers. I outlined the four years that account for just about all of the long term outperformance.

Willie Delwichie Tweeted out that all of the S&P 500's gains since 2000 have come when the VIX was above 28.5 Factors are things like momentum, low volatility, buy backs, even value and of course earlier this year funds started trading that track the night anomaly where buying at the close and selling at the open outperforms buy and hold.

From the high in 2000 it took until 2019 to double. Or you could look at the 2007 high which was within a few points of the 2000 high and say it took 12 years to double. From the high in 1968, it took 18 years to double which is a very long time of course.

Retirementplanning focuses on the steps you need to take to achieve your desired retired life, such as saving and investing wisely, creating a budget, and considering your healthcare needs. However, it is also essential to be aware of the potential pitfalls and things to avoid during the retirementplanning process.

This happens every so often, probably does not indicate a healthy market but as we saw in 2020, it can resolve by the rest of the market catching up, it doesn't have to result in a 2000-era bubble popping. I have no idea if the rest of the market will catch up or if this one will end very badly, we have no control over that.

Examples of this type of expense include $450 for tax prep, $500 for firewood, $2000 for homeowners insurance and so on. This list starts the year at about $9000 including $2000 for property tax. There a column off to the right of the various monthlies where I track things that are not monthly but maybe annual or twice per year.

A little exposure to something like TLH, that's merely unfortunate kind of like the person who put a little into Cisco Systems (CSCO) above $70 back in 2000 and still holds it today at $43. Small allocations don't become impediments to portfolio growth, simply they are laggards.

These strategies may include the conversion of an IRA or qualified retirementplan to a Roth IRA , because the tax consequences of such a conversion are based on asset values at the time of conversion, and any future growth in value will avoid income taxation, both within the plan and at the time of distribution to the plan beneficiary.

These strategies may include the conversion of an IRA or qualified retirementplan to a Roth IRA , because the tax consequences of such a conversion are based on asset values at the time of conversion, and any future growth in value will avoid income taxation, both within the plan and at the time of distribution to the plan beneficiary.

Back on October 20th, Willie Delwiche Tweeted about research he did showing that since 2000, all the net gains for the S&P 500 came with the VIX above 28.5. We'll see whether "sophisticated" leads to better nominal returns or better risk adjusted returns but these resonate.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content