This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

To find out more, I speak with Jeremy Schwartz, Global Chief Investment Officer of WisdomTree, leading the firm’s investment strategy team in the construction of equity Indexes, quantitative active strategies and multi-asset Model Portfolios. Dividends come from earnings, and so those are sort of anchors to valuation.

The previous high mark over this period, around the height of the dot-com era in early 2000, appears small in comparison. This means that the expansion of valuation multiples, like price-to-earnings (P/E), has played a big role.2 Data for Panel A and Panel B from 1/1/2000 12/31/2024. Pay attention to valuations.

While both track major indexes and serve as core holdings in countless portfolios, the similarities stop there. In this post, we break down the most important differences between SPY and QQQ across key dimensions: performance, volatility, valuation, sector exposure, factor makeup, and fees. When it comes to large-cap U.S. innovation.

Equity markets corrected by more than 50% in 2000-01 and more than 60% in 2007-08 which lasted for 1.5-3 Looking closely at your portfolio allocation should be done at all times and not just when the market corrects. For the sustainable long-term progress of financial markets, corrections are healthy and useful.

Equity markets corrected by more than 50% in 2000-01 and more than 60% in 2007-08 which lasted for 1.5-3 Looking closely at your portfolio allocation should be done at all times and not just when the market corrects. For the sustainable long-term progress of financial markets, corrections are healthy and useful.

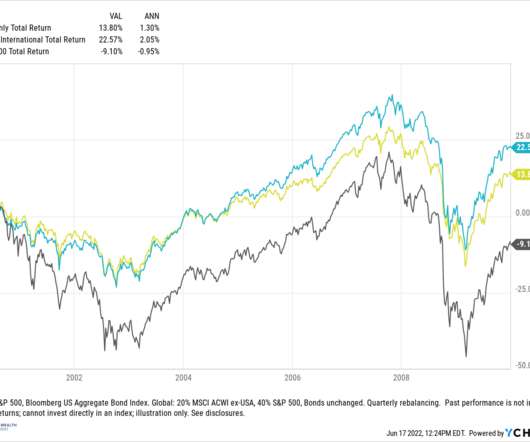

Coming into 2022, the 60/40 stock/bond portfolio had been a stalwart strategy for your balanced investor. Even with bear markets like 2000-2002 and 2008-2009, the portfolio had strong returns for a very long period. at the start of the year) things are looking brighter for this simple portfolio. Source: [link].

stocks that started in the early 2000s. Between 2000 – 2009, the cumulative total return for the S&P 500 was negative 9.1% equity may be able to help reduce risk in a portfolio. By way of example, consider this hypothetical 60/40 portfolio of stocks to bonds. Valuations. These bouts can be significant.

How did that background help when it comes to modeling portfolios or applying those methods of statistical analysis to investing? First of all, my, some of my co-portfolio managers will bristle if you refer to us as a factor based firm. That sort of data analytics wasn’t really well understood back then. It’s our size.

. ~~~ About Jeremy Schwartz: Jeremy Schwartz is Global Chief Investment Officer of WisdomTree, leading the firm’s investment strategy team in the construction of equity Indexes, quantitative active strategies, and multi-asset Model Portfolios. But when you buy a broad market portfolio, You’re getting that diversification.

A client said – I understand market valuations are expensive but it doesn’t seem that it will correct much. The fundamental driver of market peaks and exorbitant valuations is the perception that there is nothing to worry about – there is no investment risk. There is nothing to worry about.

S&P returns (including dividends) since 2019, graph by the excellent portfolio visualizer website. For example, if the house brings in $2000 per month ($24,000 each year) and the sale price is $240,000, the next investor is buying a business with a price-to-earnings ratio of 10, because 240k/24k=10.

We do discretionary macro trading, which is typically a portfolio manager — and we have some number of portfolio managers, 15 or 18 different portfolio managers that independently manage a book of, you know, risk assets. And last market question, so we’ve seen equity valuations come down. RITHOLTZ: Wow.

The Russell 2000 has declined 32% from its November 2021 high through June 2022—worse than the S&P 500’s 24% drop. And the Russell 2000 is now up 14.3% That’s led some strategists to advise investors to overweight their portfolios with small-caps, the article reports.

All of their portfolio managers not only are substantial investors in each of their funds, but they do a disclosure year that shows each manager by name and how much money they have invested in their own fund. So we really think that it creates alignment to have our portfolio managers meaningfully owning shares of the funds that they manage.

Clients participating in this year’s tech-stock rally could benefit from a portfolio review and diversification check, as this appreciation may have thrown many allocations off balance. Investors may find opportunities at more reasonable valuations when comparing different asset classes across the market.

If you’re at all interested in focused portfolios, the concept of quality as a sub-sector under value and just how you build a portfolio and a track record, that’s tough to beat. Dick Mayo was a traditional, I’d say portfolio, strong portfolio manager focused on US stocks. In 2000, right.

In an interview with Bloomberg, Villalon said that the models used by AQR indicate that equities in emerging markets have the cheapest relative valuations since the year 2000, and will beat U.S. AQR takes “a valuations-based perspective,” Villalon says, so while the firm can’t predict “if the U.S. equities for the next 10 years.

The budget gap for nonprofits has widened because of a slump in their three sources of funds—donations, grants and portfolio returns. Yet the hardest funding challenge for many nonprofits is achieving sufficient portfolio returns. Consider changes to portfolio construction. Charitable giving to foundations in 2015 shrank 3.8%

returns over the past 12 months—the second best in the history of the Russell 2000 ® Index—and on the heels of one of the worst quarters since inception in 1984 (-30.6% The strong price appreciation has resulted in a commensurate rise in valuations and a tsunami of new deal issuance in these areas. GICS Sectors. The Smallest Lead.

returns over the past 12 months—the second best in the history of the Russell 2000 ® Index—and on the heels of one of the worst quarters since inception in 1984 (-30.6% The strong price appreciation has resulted in a commensurate rise in valuations and a tsunami of new deal issuance in these areas. Small Caps: The Big Picture.

The index’s loss of 6.24% in 2018 was paltry compared to its 38% loss in 2008 and three consecutive double-digit down years of 2000-2002. This helps to illustrate the fact that market corrections are common over most periods of time and should be viewed as the market resetting stock valuations back to a more fundamental level.

Less than two years later, Palo Alto Networks purchased the company for $200 million—a more than 25-fold surge in valuation. In November 2015, Square, a San Francisco-based creator of mobile payment technology, went public at $9 per share and immediately rocketed 45% to a valuation of more than $4 billion. Not necessarily.

I had an amazing 99 in early 2000, and I had left a hedge fund, so I was probably one of the few people to leave a hedge fund and go to a larger institution in the middle of the tech bubble. The best example I always love to give is that Amazon’s last private round was at a $60 million post money valuation. It was April of 99.

This range is determined by a number of factors, including but not limited to the business cycle, valuations, interest rates, inflation, and the collective mood of millions of investors. Yesterday, Research Affiliates put out a piece saying the chance of a 60/40 portfolio returning 5% a year for the next ten years is zero.

In Engines That Move Markets, a 2002 book about the cycles of technology investing, Alasdair Nairn defines “bubbles” as periods when investors appear to suspend rational valuation, much as they had during the dotcom craze shortly before the book was published. Unsurprisingly, as volume has increased, so have valuations. Possible Signs.

1999, 2000, the internet was blowing up. And I said, Paul, I don’t know anything about managing a public portfolio, but the deal we made with each other. The SNL crisis Tiger Chase had started, you know, in the wake of the internet melding down in 2000. I I was speaking at the Javits Center, 2000 people in the audience.

Though not “working” she was making more off the family portfolio than my Dad was earning off his business. As I said there: This brings me to my conclusion: stock splits are a momentum effect, but it is larger when companies are still have a cheap valuation. I had a CTA in my portfolio. My Mom later paid me back for that.)

Market conditions may indeed be changing, and in ways that warrant a reassessment of portfolio positioning. Even as the “E” (earnings) component of the P/E ratio has increased in 2018 thanks to the strong economy and tax cuts, the “P” (price) component has moved up more, and valuations have risen perceptibly.

Market conditions may indeed be changing, and in ways that warrant a reassessment of portfolio positioning. Even as the “E” (earnings) component of the P/E ratio has increased in 2018 thanks to the strong economy and tax cuts, the “P” (price) component has moved up more, and valuations have risen perceptibly.

Instead, they’ve turned to indexing their portfolios to the S&P 500 ® Index or some other relevant benchmark, thereby accepting “average” performance rather than trying for something better. Portfolios with greater active share could be said to reflect more independent thinking on the part of the managers.

Instead, they’ve turned to indexing their portfolios to the S&P 500 ® Index or some other relevant benchmark, thereby accepting “average” performance rather than trying for something better. Portfolios with greater active share could be said to reflect more independent thinking on the part of the managers. Manager Characteristics.

It examines how transitory inflation may actually be, and how we have been positioning portfolios. The discussion dissects technology sector valuations, what rising rates could mean for markets and the most important investment trends in the decade ahead. Mon, 11/22/2021 - 11:44. Learn more >.

Amid all the noise surrounding geopolitical issues, global valuations, and FII selloff, the Nifty bulls might be feeling a bit clueless about their next moves. Here, we’ve got some pretty interesting data that shows the average per-month returns from 2000 to 2022, covering the last 23 years. Source: niftyindices.com and PrimeInvestor.in

In the short run, there can be distortions in public market valuations as we saw in 2001 and we saw prior to that in 2007, and prior to that in 2000, in ‘99. Valuations go up and you saw it, of course, in the late ‘90s, in the tech sector. BARATTA: Yeah. In the long run. You saw it in the financial services sector.

While new highs were set before bear markets in 1987, 2000, 2007, and 2020 in recent memory, the market has also made spectacular gains following new highs. A diversified portfolio does not assure a profit or protect against loss in a declining market. They are perfectly normal. In general, these records have not been warning signs.

Defining Free Cash Flow Yield Free cash flow yield is a valuation metric that compares a company’s free cash flow per share to its market price per share. A higher FCF yield generally indicates that a company is generating more cash relative to its valuation, potentially making it a more attractive investment.

As we discuss in this article, we believe that credit naturally plays a complementary role with equities in portfolios, and that this pairing can be particularly fruitful during cyclical downturns. In some situations, we may be looking to bolster portfolio stability to counteract potential macro or sector-specific headwinds.

As we discuss in this article, we believe that credit naturally plays a complementary role with equities in portfolios, and that this pairing can be particularly fruitful during cyclical downturns. Over the past several decades we have seen three major periods marked by market downturns and default cycles—1989-90, 2000-02, and 2007-08.

He has put together an amazing track record at Greenlight in the middle 2000 and tens. Then we stayed open until about 2000. And then in 2000, I don’t know, we were maybe around six or 700 million at that point. I’m the portfolio manager and I’m actually the only portfolio manager.

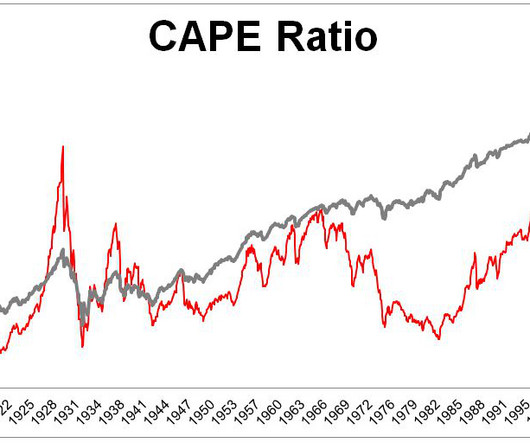

This visual tells a lot of stories, but for the purposes of this exercise, I want to focus on the two previous valuation spikes in red, which were followed by two stock market crashes in gray. If 2000 was fool me once and 2008 was fool me twice, what would 2019 be? The chart below shows the CAPE ratio and the S&P 500 (log).

Valuations of the U.S. It is rarely wise to make impulsive or reactionary investment decisions; we believe that every action in a portfolio should fit into a disciplined program with clear long-term objectives in mind. Today, we hear the word “unprecedented” far too often, referencing everything from stock valuations, to the U.S.

Valuations of the U.S. It is rarely wise to make impulsive or reactionary investment decisions; we believe that every action in a portfolio should fit into a disciplined program with clear long-term objectives in mind. Today, we hear the word “unprecedented” far too often, referencing everything from stock valuations, to the U.S.

These planning opportunities are driven primarily by four factors: Materially lower market values for publicly traded securities, and a likely downturn in valuations of real estate and other illiquid assets. to a grantor trust) similarly remain attractive because of low interest rates and potentially low valuations.

These planning opportunities are driven primarily by four factors: Materially lower market values for publicly traded securities, and a likely downturn in valuations of real estate and other illiquid assets. to a grantor trust) similarly remain attractive because of low interest rates and potentially low valuations. Outright Gifting.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content