This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

For many financial advisors, a core part of the retirement planning process involves simulating whether the client's assets will last through retirement. One way that advisors can help bridge this gap is by using Historical Market Visualization (HiMaV) as a more intuitive alternative for illustrating retirement income strategies.

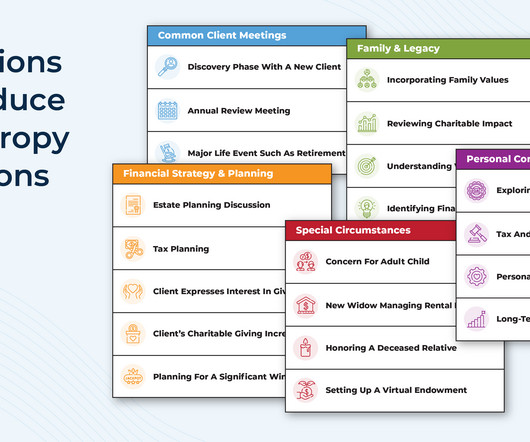

When onboarding new clients, financial advisors often use a three-meeting cadence: a Discovery Meeting to gather information, a Presentation Meeting to discuss the plan, and an Implementation Meeting to finalize it. while also setting the tone for a long-term planning relationship built on trust and deeper client engagement. Read More.

When onboarding new clients, financial advisors often use a three-meeting cadence: a Discovery Meeting to gather information, a Presentation Meeting to discuss the plan, and an Implementation Meeting to finalize it. while also setting the tone for a long-term planning relationship built on trust and deeper client engagement. Read More.

To start, Taylor refined his ideal client profile to focus on those he could best serve: diligent savers over age 50 with a retirement nest egg between $2M and $10M. These clients, typically in or near retirement, face key challenges like reducing taxes, managing investment risk, and maximizing income.

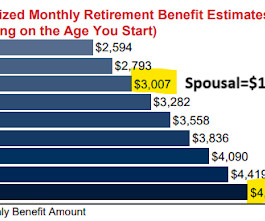

While future retirees can find nonreduced benefit estimates on their Social Security statements or online accounts, those already receiving benefits don't have access to this information – making it necessary to find a different way to predict how much their payments will increase once the law is fully implemented.

The idea of living off dividends in retirement sounds nice, but investors often don’t realize how much money they’ll need invested to generate enough income from dividends to cover lifestyle expenses. You may need more money than you think to retire on dividends. Retire on dividends?

For more information, visit: [link] See more from Jason Diamond Louis Diamond CEO, Diamond Consultants Louis has guided many of the top teams in the industry as they’ve transitioned to other employee-model firms or launched RIA firms. Jason is a graduate of Emory University in Atlanta, Ga. with a Bachelor of Business degree in finance.

Some give through established channels, such as by donating to charities or volunteer work, others may give informally to family members on a regular but less structured basis – and some simply aspire to "do more". Charitable giving is an essential aspect of many people's financial lives.

The magic of having $1 million for retirement is no longer what it once was. million as being sustainable for a 25 year retirement assuming 4%/$50,000/yr. million as being sustainable for a 25 year retirement assuming 4%/$50,000/yr. How much do you have now and how much are you likely to have when you retire?

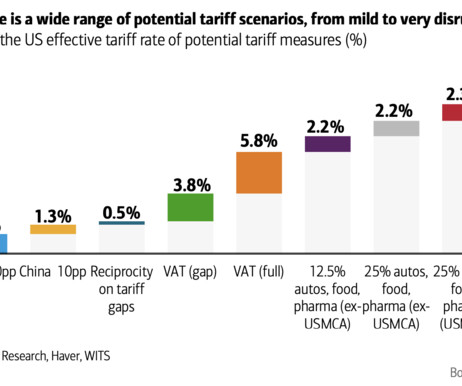

The challenge is how to frame the current economic scenario in a way that is useful and informative and not the usual run-of-the-mill noise. A quick note on tariffs : Over the past few weeks, I’ve been putting together my quarterly call for clients. We see this in the Tariffs On, Tariffs Off, Sell, Buy pattern of news-flow.

The post Investing for Retirement: Strategies for Long-Term Success appeared first on Yardley Wealth Management, LLC. Investing for Retirement: Strategies for Long-Term Success Introduction Investing for retirement is a journey that demands careful planning, patience, and discipline. What lifestyle do you envision?

As a freelancer, you juggle not only your craft but also your finances, taxes, and retirement planning. Plan for retirement 5. Plan for retirement Without a traditional employer-sponsored 401(k), freelancers need to take control of their retirement savings. That’s where financial planning for freelancers comes in.

Whether planning for retirement, investing in volatile markets, or managing tax implications, clients are often presented with intricate information that can leave them overwhelmed, confused, and anxious, undermining their ability to make informed decisions.

In this episode, we talk in-depth about how Seth built and provides his input deliverable (which calculates the appropriate amount of tax-exempt housing allowance pastors can take based on their individual circumstances, and even prepares a request and subsequent resolution that the Church's Board can then use) to demonstrate his expertise to prospective (..)

Do you know when you want to retire? Are you saving enough for the retirement you want? Myth #2: You should plan to retire in your 60s With more people going back to school or changing careers later, holding off on retiring is becoming more common, too. for more information. And then, there are the un-retirees.

Over time, advisors shifted toward more analytical approaches, such as investment management and retirement planning. In the early days of financial planning, serving clients often meant developing transactional relationships focused on facilitating trades and selling insurance. The process begins by helping clients define their core values.

Retirement planning is deeply personal, and for single individuals, it comes with both unique opportunities and important considerations. Whether by choice or circumstance, retiring solo means you’re in full control of your financial decisions, but you also face distinct planning challenges that require thoughtful strategy.

Healthcare costs are rising at a pace that demands attention, particularly for individuals nearing retirement. Without proper planning, healthcare expenses can quickly consume a significant portion of retirement savings. They can build a more resilient financial strategy for retirement. increase from the previous year.

Last observed in 2019, the campaign was paused during the pandemic and has been revived to help Americans make informed decisions about their retirement income.

There is so much information out there and so many varying and often conflicting perspectives that an advisor might rightfully feel paralyzed by indecision, uncertainty, and data overload. Its critical to be armed with accurate and timely information. Firm retire-in-place programs are the only way to retire.

It's not like this is a bad problem but there can be expensive mistakes made in this sort of scenario I want to believe that it is not realistic that if someone has a set of maybe five or six assumptions that go into their retirement plan, that not all of them would have a worst case outcome. Everything going wrong would be really bad luck.

Why Referrals Matter More Than Ever in the Digital Age In today’s online world, people receive a lot of information. Making Data-Driven Decisions to Improve Your Program Use the information you gather to make smart decisions about your referral program. These clients will likely keep using your services for a long time.

Life transitions such as marriage, divorce, the birth of a child or grandchild, career changes, retirement, an inheritance, or the purchase or sale of a home can all influence your broader financial picture. It is for information and planning purposes only. This is a publication of Tobias Financial Advisors.

This could include saving for a down payment on a home, contributing to retirement accounts, or growing an investment portfolio. These principles can inform your financial priorities and decisions. If security is your priority, focus on building an emergency fund or increasing your retirement contributions.

AI-powered search engines, including Googles AI Overviews and tools like ChatGPT, now generate responses by pulling information from multiple sources. AI prioritizes information from reputable sources secure media mentions in trusted finance publications and news sites. How Can Financial Advisors Adapt to AI-Powered Search Engines?

While an investor’s timeline affects their risk tolerance and allocation decisions between stocks and bonds, it’s important to remember how long a retirement time horizon can truly be. Retirement planning, like any type of robust financial planning, should include stress testing your investment strategy and financial plan.

The answer largely depends on your financial situation, but understanding the value these professionals bring can help you make an informed decision. Retirement Planning Retirement planning is one area where talking to a financial planner proves particularly worthwhile.

For instance, I will contribute an additional $10,000 to my retirement fund this year or I will pay off my $15,000 credit card balance by December 2025. Allocate funds for savings, retirement, and an emergency fund while leaving room for meaningful indulgences. Outcome: What Results Will You Achieve? Ready to Grow Your Wealth?

Backdoor strategies are retirement contribution methods that allow individuals to bypass income limits and contribute to tax-advantaged retirement accounts. Roth IRAs are also not subject to Required Minimum Distributions (RMDs), allowing more flexibility in retirement planning.

The 4% rule is generally the accepted standard for a safe withdrawal rate in retirement to ensure the assets last for 30 years. Bengen retired as a financial advisor in 2013 but he also considers himself a researcher. He basically ran the numbers for someone retiring in 1926 and then each each up into the 1970's.

Financial literacy isn’t just about knowing technical jargon—it’s about applying principles that support informed financial decision-making. This can come from dividends, interest, rental income, and distributions from brokerage or retirement accounts. What is Financial Literacy? Deferred gratification often plays a role in saving.

This information can help you improve your campaigns and boost your ROI. Running focused social media campaigns that highlight their services and share their skills in areas like tax planning or retirement planning. Using strong cybersecurity is important to protect sensitive information from breaches and unauthorized access.

Retirement Planning: Looking Beyond the Basics For 2025, it’s essential to think beyond the standard “maximize your 401(k)” advice. While that remains important, consider diversifying your retirement strategy. This can significantly impact your retirement savings trajectory.

They often use the internet to find information and make choices. This includes budgeting, investing, retirement planning, and understanding key financial concepts in wealth management. Email Marketing Build relationships and share valuable information through targeted email campaigns. Use a friendly tone to keep them engaged.

Fully Utilize Tax-Advantaged Retirement and Savings Accounts There are multiple steps you can take using retirement accounts to reduce your taxable income. Contribute to Tax-Advantaged Retirement Accounts Do your best to fully contribute to one or multiple tax-advantaged retirement accounts, such as 401(k), 403(b), or IRAs.

Advisors can customize the application to convey pretty much any type of data or information clients or prospects might want. We have a serious communication problem in the industry, and it can be really hard to get hold of clients,” he said, noting that with his technology, advisors can see their clients go to the app every day.

In this episode, we talk in-depth about Michelle's 5-part planning process, which starts with a "Get to Know You" meeting with prospects that includes some Life Planning exercises to both help Michelle understand what the client's real issues are and help the client understand Michelle's planning approach and whether a planning relationship would be (..)

Articles that inform and educate your readers. Infographics that present information in a visual way. E-books that provide in-depth information on a subject. E-books that provide in-depth information on a subject. Articles: Discuss topics such as investing, retirement planning, and related subjects.

Leave Space for Responses A common mistake is overloading posts with too much information. Instead of listing ten tips for retirement planning, share your top three and ask, What would you add to this list? For instance, many people feel overwhelmed by retirement planning. Whats your biggest question about retirement?

Let’s be honest, retirement isn’t what it used to be. The traditional blueprint of working until 65, collecting a pension, and retiring feels outdated, especially for mid-level professionals who’ve started thinking early about what their ideal retirement should look like. What’s the earliest you can retire?

Click here and contact us for more information. A: Key tax deductions include maximizing retirement contributions, utilizing HSA accounts, strategic charitable giving through donor-advised funds, and property-related deductions like mortgage interest and property taxes. Tax Strategies for High-Income Earners in 2025.

The calculation becomes increasingly complex for higher-income taxpayers , as it introduces factors such as W-2 wages paid to employees, the unadjusted basis of qualified property, and retirement plan contributions. Connect with our expert advisors today for guidance on life events, equity compensation, or retirement planning.

This content is intended for informational purposes only and does not constitute legal, investment, or financial advice. The views and opinions expressed in this article are those of the author and do not necessarily reflect the official policy or position of Moran Wealth Management.

The key to success lies in grasping what your target audience truly needs and delivering that information in formats they prefer to consume. A timely video explaining how recent Federal Reserve decisions might impact retirement planning can position you as the go-to advisor for your niche.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content