This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

It's natural for advisors to begin discovery meetings by asking questions about a client's current financial situation – understanding cash flow, debt, investments, risktolerance, or even the burning tax concern that brought them to the advisor's door in the first place is crucial for financialplanning.

Also in industry news this week: 43% of wealth management firms are frustrated with the effectiveness of their CRM software, spurred on by challenges with integrations and workflows, according to a recent survey The Social Security Administration this week announced a 2.5%

This month's edition kicks off with the news that 'startup' custodian Altruist has completed a $169 million fundraising round as it continues to rebuild the RIA custodial tech stack layer-by-layer while positioning itself as the biggest RIA custodian built from scratch and solely for advisors – which, while making it the clear #3 custodian behind (..)

Over the years, 2 types of measurement tools have emerged as the standards for assessing risktolerance: 1) psychometric tests, which feature a series of questions (such as, "What amount of risk do you feel you have taken with past financial decisions?") Read More.

Also in industry news this week: How Goldman Sachs’ RIA custodial platform is leveraging the resources of its parent company as it seeks to build momentum amidst a highly competitive environment among custodians How NASAA has changed the substance and/or scoring of the Series 63, 65, and 66 exams From there, we have several articles on college (..)

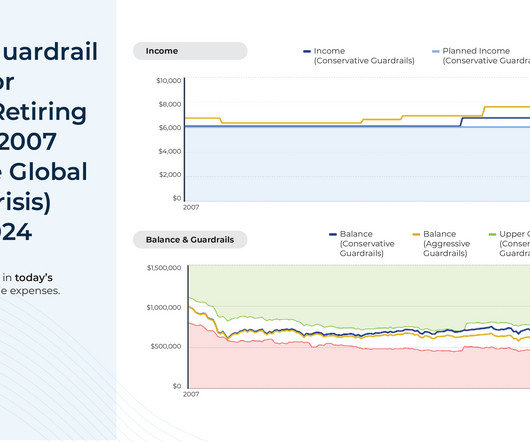

Monte Carlo simulations have become a central method of conducting financialplanning analyses for clients and are a feature of most comprehensive financialplanning software programs. the Great Depression or the Global Financial Crisis), showing clients when and to what degree spending cuts would have been necessary.

Financialplanning can take your money game up a notch by bringing clarity, strategy, and intention to your financial life. A healthy financialplan gives you the tools to take control of your finances and start living your life with passion, purpose, and freedom. So what’s the value of a financialplan?

No one cares about your financial well-being more than you, so it's important to have a financialplan for yourself. Knowing how to make a financialplan will allow you to save money, afford the things you really want, and achieve long-term goals like saving for college and retirement. What is a financialplan?

Brian Portnoy : So you’ve pointed accurately to a number of studies on this and maybe it’s 75,000 or 90,000 I’d also point out that a dollar spent in Manhattan NY versus Manhattan KS those are very different conversations. Brian Portnoy : Investing outside of a well-defined financialplan is speculation.

For more years than I’d care to name, I’ve been trying to put my finger on exactly why I have a such a huge problem with the traditional (Think: Riskalyze, now Nitrogen) risktolerance assessments in the financialplanning profession. You can actually test various bear markets and adjust accordingly.)

No one cares more about your financial well-being than you, so having a personal financialplan is important. Knowing how to make a financialplan will allow you to save money, afford the things you want, and achieve long-term goals like saving for college and retirement. Table of contents What is a financialplan?

Historically, staying the course and following a financialplan has outperformed rash investment decisions when there are times of uncertainty in the financial market. But it takes a strong plan—and no small amount of willpower—to do this.

However, it should be well understood that a client’s financial profile includes their risktolerance and their risk capacity. In this article, although we will be focusing on the latter one and why it is significant to determine your client’s risk capacity let’s first understand the difference between the two.

The number of entrepreneurs in America has exponentially increased over the past few years. That said, entrepreneurship can sometimes be cumbersome in spirit, especially in terms of financialplanning. Why is financialplanning important for entrepreneurs? What is meant by business financialplanning?

Factors to consider would include – job changes, a change in the number of dependents, or a change in the number of breadwinners. If you are unsure if your portfolio aligns with your risktolerance, time horizon and goals, reach out to us at Mainstreet and we would be happy to help!

We pulled together some information and interesting facts about some of the major indexes that can help you put the numbers you hear in context. In time, the DJIA itself would evolve, and the concept of stock indexes would grow in number, size, and importance. It’s not the number of points that matters—it’s the percentage change.

Financialplanning can take your money game up a notch by bringing clarity, strategy, and intention to your financial life. A healthy financialplan gives you the tools to take control of your finances and start living your life with passion, purpose, and freedom. So what’s the value of a financialplan?

In working with your tax professional and investment advisor, make a tax plan that incorporates your diversification goals and considers tax strategies on new exercises. Financialplanning: It’s a highly nuanced situation when a company goes public. Consider your risktolerance and overall concentration.

Recognizing the need for a financialplan is a significant first step toward the goal of achieving personal financial security. Table of Contents What is a FinancialPlan? Table of Contents What is a FinancialPlan? Why is FinancialPlanning so Important?

Of course, not all small-cap stocks grow to be the next big thing, and these companies may face a number of challenges along the way. For instance, small companies usually do not have the same financial resources as larger firms do. You can choose what to invest in, such as stocks, bonds, index funds, target-date funds, etc.

With the competition becoming fierce in the growing financial industry, you need an edge to set yourself apart from your competitors. That can be done by asking the right financialplanning questions and providing your clients with a unique and extraordinary advisor-client experience.

Whether you’re building equity in a primary residence or buying a vacation home or investment property, understanding how to best prepare for, and manage, a real estate purchase is a critical piece of any personal financialplan. and FinancialPlanning for Estate Planning.

First, do you have the necessary financial acumen and knowledge to make financial decisions? Are you good with numbers, accounting, and financialplanning? If yes, then DIY financialplanning might be a good option for you. What is DIY financialplanning? Chalk out a financialplan.

Tip #3: Identify investment strategies to build long-term wealth Building long-term wealth requires identifying investment strategies that align with your goals, risktolerance, and timeline. Tip #4: Keep your emotions in check More than the numbers, building wealth is about having the right mindset.

For some, concentration risk might mean holding any amount of a single stock position in a company they work for. For others, concentration might feel suitable if they have significant other assets and/or if they have a high risktolerance or high risk capacity. Here are a number of reasons we’ve seen.

often fail to consider sequence of return, housing, longevity, health or family risks faced in retirement. Focus on Your Retirement Plan Rather Than a Magic Number. A better question than “What’s my magic number?” would be “How do I plan for retirement?“

Want some numbers to back that up? So, if you are planning your next investment move, speak to a financial advisor about the future of AI and other tech enhancements. Consider if these industries can be a good fit for your portfolio or not and understand how leveraging AI can help you enhance your financialplanning.

Your investment strategy determines the target percentages for each asset, often based on your risktolerance, investment goals, and time horizon. This may lead to a higher or lower risk profile than initially intended. With a higher income, your risktolerance can increase, and you may be more open to investing in equities.

Women’s financialplans are unique, so their investing strategies should be, too. Find out more about women and investing, and discover ideas for creating your own investment plan. Women investors are doing great financially, proving that women are equipped with the skills needed to be successful investors.

With a money market account, you can withdraw your money at any time, but there may be limits on the number of withdrawals you can make per month. On the other hand, a Money Market Fund is a type of investment fund that invests in short-term, low-risk debt securities such as treasury bills, commercial paper, and certificates of deposit.

Its essential to focus on more than just numbers when determining your transition approach. Here are five examples of analogies that can simplify complex ideas about the transition: FinancialPlanning Analogy You know how we’ve been working together to create a comprehensive financialplan for you?

It’s a number that lenders take a hard look at when you apply for a mortgage or another personal loan. Understanding your personal net worth will give you a clearer picture of where you stand financially. Are you getting closer to the number you need to retire, for example, or to pay for college for your kids?

Start planning early. It takes strategic foresight, hard numbers, and smart decisions that begin well before your final day at work. Yet far too many professionals delay the planning process. Rebalance annually: Your risktolerance at 40 isn’t the same at 55. And the best way to do that? Doing it right?

The 401(k) Plan 2. The SEP-IRA (AKA Simplified Employee Pension) Expert tip: Understand your risktolerance How to save for retirement in your 20s when you’re just starting out How much should I contribute to my 401(k) in my 20s? Generally, an investment fund with a later date can take on higher risk than one with a nearer date.

Then you can choose the options that are best for you when you create your investment portfolio and financialplan. Here’s a list of some of the types of investments you’ll encounter as you make financial choices: Individual stocks Individual stocks are shares of a company you can buy and have partial ownership.

When it comes to managing wealth and planning for a secure financial future, the services of financial professionals, such as financial advisors or wealth managers, are invaluable. Table of Contents What Services Does a Financial Advisor Provide? Are Robo-Advisors a Good Alternative?

One thing that I have craved for investors is a tool that allows you to sync all your financial accounts – your investment portfolio, checking and savings accounts, credit cards and other loan accounts – in one place, and then provides an investment-related analysis of your entire portfolio. What are the cons of Personal Capital?

Financial advisors can offer insights into a diverse range of investment instruments, including stocks, bonds, real estate, and precious metals like gold, and align the recommendations with your risktolerance and long-term goals. These professionals also go beyond the numbers and charts and educate you about investing.

Pros and Cons of Tender Offers for Startup Employees Personal FinancialPlanning Considerations Frequently Asked Questions What is a Tender Offer? A tender offer is a liquidity event in which a company, investor, or group of investors propose to buy a fixed number of shares from existing shareholders at a set price.

The downside to highly liquid investments 12 Highly liquid vs short term highly liquid investments Expert tip: Know your risktolerance When does it make sense to pursue a liquid investment? The asset must maintain a large number of readily-available, interested buyers. They have their place in any financialplanning process.

This is because you have been failing to plan your funds because of less time, following the old ways, peer pressure, less understanding of the financial markets, and so on. A financial advisor is a certified financial planner who is licensed and regulated to take mandate decisions on multiple aspects of financialplanning.

Deciding what to do with a cash windfall always comes down to your personal goals and financial situation. And ultimately, how to invest a windfall will depend on a number of factors, including your risktolerance, time horizon, and spending plans. One-time cash needs Lay out any one-time potential cash needs.

Deciding what to do with a cash windfall always comes down to your personal goals and financial situation. And ultimately, how to invest a windfall will depend on a number of factors, including your risktolerance, time horizon, and spending plans. One-time cash needs Lay out any one-time potential cash needs.

Knowing the types of financial advisors and their compensation models can empower you to select a professional whose approach aligns seamlessly with your financial goals, risktolerance, and overall budget. Below are the different types of financial advisors you can choose from based on their fee model: 1.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content