This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Finally, it would be dangerous to extrapolate the post-1990 outperformance of US equities, as it mainly reflects rising relative valuations. He’s often referred to as Jungleman, a nod to his longtime screen name on poker sites. If anything, the current richness of US equities may point to prospective underperformance. (

I am referring to my explanation of “asset price inflation” relative to QE. I jokingly referred to this as assflation because how else can you respond to things that seem obviously wrong, except with a joke? My argument for why stocks were going up was because there was real fundamental improvement in the economy.

Markets Market valuations are a lot more attractive than they were a year ago. mantaro.money) Media Jeff Jarvis, "If network prime time has lost its value, so have networks, so has television, so has broadcast." (finance.yahoo.com) Economy Auto loan delinquencies are on the rise. blog.validea.com) Visualizing U.S.

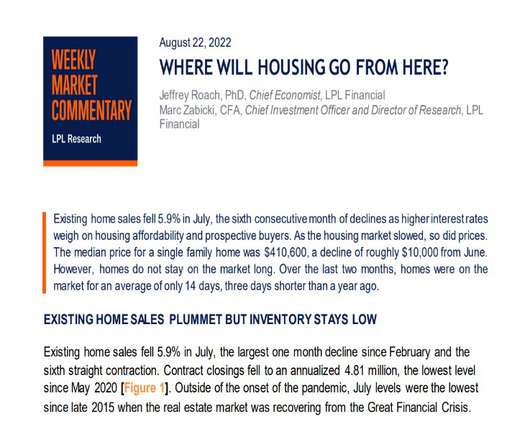

Given the lag between Federal Reserve (Fed) policy and the real economy, we have not likely seen the bottom in the housing market. Outside of the pandemic, the rate of sales were close to sales rates in 2007 and 2008, when the economy was in the depths of a housing crisis [Figure 3]. Regional differences are profound. Conclusion.

This refers to the strategy where you just move everything into T-Bills and “chill” 1 This move sounds increasingly enticing. today, but what if the economy keeps humming along, the stock market never crashes and the Fed eases rates back to 2% over the next few years? After all, 5.5% For example, rates are 5.5%

And companies can grow earnings as long as the global economy grows, which is something it has been doing much more often than not for several millennia. There have been short-term fluctuations when the economy has slowed, but the overall trend has been strong. economy can continue to grow, and the rest follows.

Perhaps the market’s biggest fear has been that the Fed may overdo its tightening to fight inflation and send the economy into a painful recession, break something, or both. He acknowledged that the economy is slowing (which is what the Fed wants) and that the full effect of the rate hikes had not yet been felt. Of course, the U.S.

at year-end can largely explain the compression in valuation, especially for higher multiple equities, primarily during the first half of the year. P/E calculations presented use FY2 earnings estimates; FY1 estimates refer to the next unreported fiscal year, and FY2 estimates refer to the fiscal year following FY1. by year-end.

It’s the same with a nation’s economy! This not only benefits the businesses themselves but also ripples through the entire economy, fostering progress and development. The primary valuation concern was that Indian stocks run ahead of fundamentals, leading to high valuations. February -1538.88 March 35098.32

One you referred to is aggressive investors and as the name would indicate, it has high 00:16:35 [Speaker Changed] Beta, 00:16:35 [Speaker Changed] A very well high beta, but very high exposure to the factors that we want, that we believe in. So you think of old economy stocks and new economy stocks is another way to think about ’em.

economy enters a recession, the causes and potential outcome will be hotly debated. The three factors for defining a recession are depth, diffusion, and duration – conveniently referred to as the “three D’s.” Depth refers to declining economic activity that is more than a relatively small change. If the U.S.

Suggesting an economy makes “no landing” makes no sense. Economic activity does not stop like an airplane eventually does, but rather the economy will settle into a steady state where growth is consistent with factors such as population and productivity. Analogies eventually break down, especially this one. Why The “Landing” Analogy?

economy contracted for the second straight quarter. With a strong, even if slowing, job market and resilient consumer spending, we believe not enough sectors of the economy are contracting to qualify as an official recession. Given the slowing economy, intense cost pressures, and a strong U.S. All index data from FactSet.

economy contracted for the second straight quarter. With a strong, even if slowing, job market and resilient consumer spending, we believe not enough sectors of the economy are contracting to qualify as an official recession. Given the slowing economy, intense cost pressures, and a strong U.S. All index data from FactSet.

After the subprime crisis in 2008, many developed countries’ Central Banks started printing money and flooding the global economies with cheap liquidity. This resulted in inflation to the levels last seen 40 years ago in many developed economies. But first a quick recap. US Fed increased its balance sheet size from ~$4-4.5

The expectation was predicated on the view that inflation pressures would ease as global economies recalibrated to a post-pandemic environment. economy to avoid recession, and support above-average valuations. While our team underestimated inflation and the resulting hit to valuations last year, there were some wins.

economy is in or about to enter recession, so we thought a piece on what a recession might mean for the stock market would be of interest. economy is not currently in recession, odds are still perhaps a coin flip or better that one may come in the next year. While Friday’s strong jobs report provides more evidence that the U.S.

For the “no landing” crowd thinking strong consumer spending and low unemployment would keep this economy growing until the inflation fight is won, they now have to consider signs of stress in the banking system after the failure of SVB Financial (commonly known as Silicon Valley Bank). But valuations strongly favor value over growth.

While the factors above have buoyed dividend-rich stocks this year, such stocks now pose a rising risk in portfolios for several reasons: Their valuations have stretched beyond what is justified by the fundamentals in many cases. Cause for Caution: Why Dividend-Rich Stocks Pose A Greater Risk Stretched Valuations. Passive Inflows.

While the factors above have buoyed dividend-rich stocks this year, such stocks now pose a rising risk in portfolios for several reasons: Their valuations have stretched beyond what is justified by the fundamentals in many cases. Stretched Valuations. billion, nearly double the $367.3 billion in assets they held in 2011. Conclusion.

The key to getting the market back into balance is a bigger labor force, and the economy is starting to experience a larger labor force as individuals come off the sidelines and rejoin the job market. The global economy is complex, and a simplification of reality always introduces distortions, so perhaps we should zoom out a bit.

Today, we see this happening with the so-called “FANG” stocks—Facebook, Amazon, Netflix and Google (now Alphabet—for consistency we will refer to the company as Google throughout this piece). Investors also tend to naturally focus their valuation fears on big, rapidly growing stocks.

Today, we see this happening with the so-called “FANG” stocks—Facebook, Amazon, Netflix and Google (now Alphabet—for consistency we will refer to the company as Google throughout this piece). Investors also tend to naturally focus their valuation fears on big, rapidly growing stocks. False Connections.

These updates will also be available on BSE Limited’s website for public reference. Growth potential: With a solid growth history, NSE is well-positioned to capitalize on India’s expanding economy, which promises significant opportunities for further financial market expansion. The market valuation of NSE might be between ₹2.1

A global economy that was already vulnerable to inflation from supply chain disruptions, tight labor markets, excess stimulus, and loose monetary policy came under more pressure when Russian aggression in Ukraine added sharply rising commodity prices and put Europe on the brink of recession. In the midst of the storm. If the U.S. If the U.S.

Trade was important to the Roman economy and it generated vast wealth for the citizens of Rome. The economy was in shambles and trade was majorly localized and was done using barter methods. This has resulted in skyrocketing valuations of the stock markets. Nifty currently is trading at a multi-year’s high valuation.

Given the country’s weak economy, due in large part to stringent zero-COVID-19 measures that have led to strict and prolonged lockdowns, coupled with a debt-laden property market, authorities in Beijing and throughout the Chinese provinces will need to focus on reviving the country’s economic underpinning. At the same time, U.S.

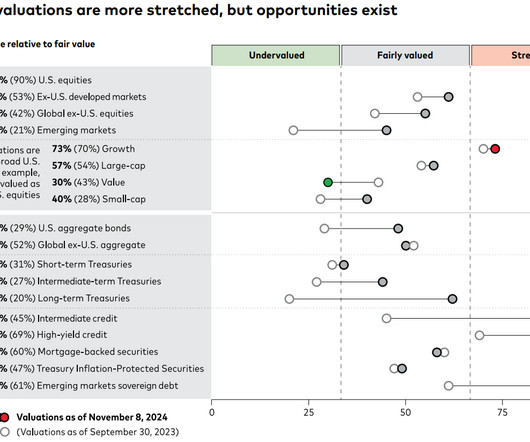

We know that equity valuations in the U.S. CURRENT VALUATION PREMIUMS, S&P 500 INDEX Metric Most Recent Long-Term Average Premium vs. Average Timeframe Trailing P/E 19.4 Please refer to the end of the article for a complete list of terms and definitions. We simply don’t know what might happen three months or six months from now.

We know that equity valuations in the U.S. CURRENT VALUATION PREMIUMS, S&P 500 INDEX. In the years after the 2008-09 financial crisis, securities tended to trade in lockstep with each other as the market focused most of its attention on the big-picture health of the economy. Most Recent. Long-Term Average. Premium vs. Average.

The “Magnificent 7” has become a popular term on Wall Street, referring to seven large technology companies that have dominated stock market returns in recent years: Apple, Microsoft, Alphabet, Amazon, Nvidia, Meta Platforms, and Tesla. Strong return on equity (ROE): The company’s average ROE of 18.5%

With a series of important economic indicators suggesting the economy is declining and inflation is finally decelerating, albeit very slowly, markets are beginning to factor in that the Fed may soon transition to a less aggressive stance in early 2023. The Economy Slows But Inflation Follows Too Slowly. economy grew at a 2.6%

economy in mid-March, 62% of S&P 500 companies beat estimates, and aggregate earnings were within one percentage point of expectations. economy, as measured by gross domestic product, so the ISM index tends to have some predictive power when it comes to earnings. The S&P 500 is more manufacturing-heavy than the U.S.

As the economy is likely downshifting, investors should take heed that the Federal Reserve’s (Fed) current stance is eerily similar to early 2007. During that time, the Fed held a tightening bias since they believed the housing market was stabilizing, the economy would continue to expand, and inflation risks remained.

Topic 1: Economy Bull case: Consumer is resilient, the labor market is strong, wages are rising, and inflation is coming down steadily. Background: The global economy will likely slow from the upper-2% range in 2022 down to slightly above zero in 2023 ( Figure 1 ). Call us cautious bulls. Our take: The U.S.

But the drop in valuations experienced at year’s end, alongside higher bond yields, offer a foundation for better long-term return expectations across most asset classes. This is also a fitting moment to review the intersection of risk and valuation. Entering 2019, we face rising economic, political and market risks. In non-U.S.

The “Magnificent 7” refers to a group of seven elite large-cap technology companies that have delivered outstanding long-term returns and growth. As the top companies in the world’s largest economy, they are seen as the leaders of the digital economy and the faces of American innovation and global success.

ILMANEN: It’s always good to think of starting yields and valuation sort of two sides of the same coin. But in conclusions, I did put there that it just seems that stars are aligning for some fast pain and it wasn’t just high valuations but there was a catalyst. Explain that. Bonds are the most expensive. RITHOLTZ: Right.

However, as Fed rate hikes flow into the real economy, the risk of a recession increases, which should help bring down yields. This is referred to as an inverted yield curve, which has been a pretty reliable predictor of economic recessions. It is also a major component used to calculate the price-to-earnings valuation ratio.

If an economy needs to see inflation easing, it makes little sense to stimulate the economy through tax cuts while tightening monetary policy by raising interest rates. Powell has repeated, in what has become his mantra, that without price stability we cannot have a strong economy or a strong labor market.

The numerous challenges last quarter included a slowing economy, intensifying inflation pressures, ongoing global supply chain disruptions, and a surging U.S. References to markets, asset classes, and sectors are generally regarding the corresponding market index. Investing involves risks including possible loss of principal.

economy remains on solid footing, and expectations the Fed is close to completing its rate hiking campaign, bankers are hopeful they can begin taking a growing pipeline of companies public. economy and corporate America have has been impressive. It is also a major component used to calculate the price-to-earnings valuation ratio.

This is referred to as financial statement analysis: a comprehensive review of key financial documents to assess a company’s effectiveness. And because the financial sector is so important to the functioning of the economy, it’s safe to say that there will always be a demand for financial professionals.

economy grew at a solid 3.2% and European economies, currency effects, and some mitigation of profit margin pressures from cost controls and lower inflation. economy may “muddle through” and skirt recession. References to markets, asset classes, and sectors are generally regarding the corresponding market index.

Forward-looking sales estimates paint a more subdued picture, which makes sense given the macro headwinds facing the economy and the consumer. Retailer valuations have also taken a hit, as the forward (next 12 months) P/E multiple has contracted ~20% year to date, from ~27x to ~22x currently. over the last 20 years, pre-2020.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content