This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

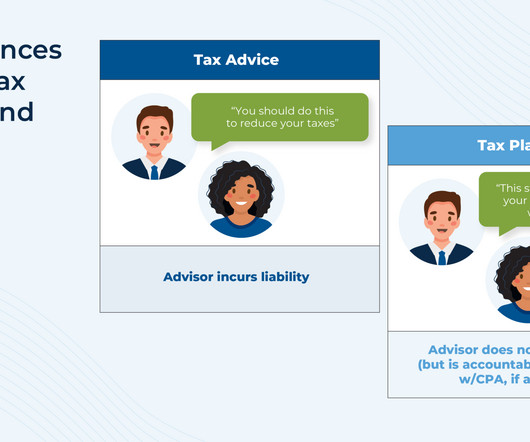

In recent years, financial advisors have increasingly embraced taxplanning as a core element of delivering value to clients. Despite this growing interest in tax conversations, most advisors are still quick to distinguish their services as "taxplanning", not "tax advice" – a distinction largely driven by liability concerns.

This month's edition kicks off with the news that digital estate planning platform Wealth.com has raised a whopping $30 million in Series A funding, following on the heels of Vanilla's follow-on $20M capital round just a few months ago – which on the one hand reflects the anticipated enthusiasm for solutions that can help advisors efficiently (..)

Seth is the founder of Heartwood Financial Planning, an advisory firm affiliated with PlanMember Securities Corporation that is based in Fresno, California, and oversees approximately $100 million in assets under management for 850 client households. Welcome everyone! Welcome to the 432nd episode of the Financial Advisor Success Podcast!

As the year comes to a close, now is the time to review potential financial moves to help minimize your tax burden heading into 2025. Proactive year-end taxplanning can lead to significant savings and set you up for financial success in the new year.

For many small tax firms, the process of collecting client taxdocuments can be a time-consuming and a prolonged process. The good news is that technology solutions, like Harness, can streamline document collection and transform the way tax professionals work.

Yet just like your vehicle, your financial plan benefits from regular maintenance and timely adjustments. At Tobias Financial Advisors, we view financial planning as an ongoing process designed to evolve with your life. It is for information and planning purposes only.

Financial planning and taxplanning go hand in hand. Including taxplanning as part of your service provides clients a comprehensive view of their finances and helps them achieve their financial goals. Start with Document Sharing The first step is to ask your clients to share their taxdocuments with you.

Estate planning is one of the most important steps in securing your financial legacy, but its also among the most complex. Understanding how assets will be distributed, navigating tax implications, and aligning these decisions with your personal goals can feel overwhelming.

Set up separate plans and goals for your business and your personal finances. It helps you plan for future expenses, allocate resources efficiently and stay on track with your financial goals. Identifying these risks early and having a plan to mitigate them can save your business from significant setbacks.

Without proper planning, taxes can unexpectedly take a large bite out of the proceeds, potentially reducing financial security and the legacy. When you understand various exit strategies and their tax implications early, you position yourself to make informed decisions that maximize after-tax value while ensuring a smooth transition.

We will cover qualification criteria, documentation requirements, and practical strategies to implement throughout the year. We will cover qualification criteria, documentation requirements, and practical strategies to implement throughout the year. Travel, meals, and supplies must directly relate to legitimate business activities.

Let us face ittech startups encounter a unique set of tax challenges that can make or break their financial future. The complex interplay between traditional tax regulations and the innovative nature of tech businesses demands smart planning from day one.

Taxplanning serves as the cornerstone of the entire acquisition deal, extending far beyond a simple checkbox. Every element, from structure to price negotiations, hinges on understanding tax implications for all parties involved. Get it right, and you will have set yourself up for a smooth transition and maximized returns.

This article explores the distinctions between K-1 and 1099 reporting, explaining their impact on taxplanning, basis calculations, filing deadlines, and strategies to optimize your after-tax returns from alternative investments.

This article will explore how to navigate complex tax situations arising from multiple income sources, examining various income types, reporting requirements, self-employment obligations, and strategic approaches to record-keeping and taxplanning that can help protect your financial interests.

For high-net-worth individuals, continuously refining your strategy over time is what keeps your plan efficient and aligned with evolving goals. At Zoe Financial, we’ve seen firsthand how proactive planning with a fiduciary advisor helps individuals protect and grow their wealth across generations.

Everyone’s tax situation is different, and as a result, there are no “one-size-fits-all" guidelines available as to what to keep, how long to keep it for, and what your tax professional actually needs to see versus what you need to keep as support documentation.

This option requires no additional documentation or complex calculations, making it an attractive choice for many taxpayers. This is particularly true for frequently audited credits, such as the Earned Income Tax Credit (EITC), which has historically been subject to fraudulent claims and requires robust supporting documentation.

Whether you are contemplating forming an LP or already operate one, gaining clarity on tax matters can optimize your financial outcomes and ensure compliance with state and federal regulations. Identifying and leveraging these opportunities is a vital part of effective taxplanning.

Incomplete taxdocumentation: Waiting for essential taxdocuments, such as W-2s, 1099s, or other forms, is a common reason to file for a tax extension. Unexpected life events: Unforeseen circumstances, including illness, bereavement, or other emergencies, can disrupt tax preparation.

Moving funds from traditional IRAs to Roth accounts triggers immediate taxation but promises tax-free withdrawals in retirement. The stakes became higher after the Tax Cuts and Jobs Act of 2017 eliminated recharacterizationthe ability to reverse conversions that did not work as planned.

State and local taxes Secondary funds and their investors may face various state and local taxes, including income tax, franchise tax, and property tax. These taxes can vary significantly depending on the location of the fund, its investors, and its investments. FIRPTA planning using a U.S.

Document Request Follow-up “Hi [Client Name], just checking in on those documents we discussed. Event Invitation Follow-up “Hi [Client Name], thanks for your interest in our retirement planning workshop. Text me with any questions – I typically respond within 30 minutes during business hours.”

These contributions not only provide immediate tax relief but help secure longer-term financial stability during retirement. 401(k) Plans: Contribute the maximum allowable amount for 2024 : $23,000 if youre under 50, or $30,500 if youre 50 or older. Timing RMDs : Begin taking RMDs by April 1 of the year after you turn 73.

This is the time to do comprehensive financial planning: retirement planning, investment planning, taxplanning and estate planning. Discuss more advanced estate planning, charitable planning and special family issues. This is the new normal, where she is now loving life and moving forward.

No one cares more about your financial well-being than you, so having a personal financial plan is important. Knowing how to make a financial plan will allow you to save money, afford the things you want, and achieve long-term goals like saving for college and retirement. Table of contents What is a financial plan?

You may be eager to file your taxes to get your return as soon as possible, but filing before you have all your documents can actually cause delays in getting your return. It’s best to be patient and ensure that you have all the documents that you need for submitting your taxes. [1] Make sure you sign your documents!

They receive copies of W-2s from employers, 1099s from clients, and other income-reporting documents. To avoid scrutiny, maintain detailed logs of business-related expenses , making sure that all deductions are directly related to business activities and are supported by proper documentation, such as receipts and itineraries.

Depending on a firms tech strategy, she wrote, advisors may have to log in to the CRM, custodian, portfolio accounting, planning software, taxplanning software, estate planning software, social security maximizer software, etc.,

By Mike Valenti, CPA, CFP®, Director,TaxPlanning LLCs can provide legal protections and a level of anonymity, either or both of which can be beneficial for business owners, investors, and others with valid intentions. From the business : Legal business name and all DBA names Physical address (not a P.O.

Taxes owed on pre-tax contributions converted to a Roth 401(k) can also move individuals into a higher tax bracket for the year Mega Backdoor IRA Up to $46,000 Higher contribution limit, with no Required Minimum Distribution. It also requires an individuals 401(k) plan to allow after-tax contributions and in-service withdrawals.

MainStreet Financial Planning , Inc. We want to make it unequivocally clear that MainStreet Financial Planning, Inc is not associated with this debt consolidation agency in any way. Please also note that the name of our financial planning firm is spelled differently. MainStreet Financial Planning, Inc.

This contract serves as documentation for the IRS, substantiating your self-employment. A good rule of thumb is to set aside at least 30% of every payment you receive to cover your estimated tax obligationshowever, this percentage may need to be adjusted based on your individual tax bracket.

Plan for Current Business Needs. First, let’s talk about the importance of a business plan. It takes vision, work, and a good plan. For entrepreneurs, we call this map a business plan. Some essentials of a business plan include: Researching competing products. Creating a marketing plan. TaxPlanning.

2017 Year-End Planning Letter. presidential election, we have grappled with the lack of clarity regarding the details of new tax legislation. The outcome of the tax reform debate is likely to impact how we advise clients on taxplanning, estate planning and a host of other topics. Mon, 12/04/2017 - 13:10.

Most recently, Intel announced layoffs impacting 15% of the workforce with a plan to cut $10 billion in total costs. So, if you separate from the company near the end of the year, earning a full year of salary plus severance payouts, you could be pushed into a higher tax bracket. Taxplanning for a transition out of Intel is critical.

However, the tax treatment of a C Corp is distinct and can be complex, requiring careful consideration and planning. This article provides a comprehensive overview of C Corp taxes, exploring what defines this business structure, its tax filing requirements, key deductions and credits, and both state and federal tax considerations.

Financial paraplanners can be recent college graduates with no work experience, or may also be career changers with an extensive background in other areas that can add more value to an RIA owner, such as tax professionals. He cold called over 500 financial planning companies over a year or so to get to a full book of clients.

Traditional tax firms tend to have rigid business models that make it difficult for clients looking for one-off expert consultations or even ongoing planning services. Ongoing tax guidance from an accountant throughout the year, including expert insight into the industry and state-specific tax optimizations that affect you.

Enter reporting company information Legal Name: Enter the full legal name of the reporting company exactly as it appears on official documents. EIN/Tax ID: Enter the company’s EIN or other applicable tax identification number. Pay close attention to names, dates, addresses, and identification document details.

Step 1 – Gather Your Documents The first step in filing your Vermont taxes is to collect all relevant financial documents. This includes W-2 forms from employers, 1099 forms for other income, records of deductions and credits, and any prior year tax returns. Both are valuable tools in effective taxplanning.

Most importantly, tax practices are built on strong client relationships and specialized knowledge. Succession planning for tax practices, therefore, is as delicate a process as it is important. Table of Contents Why is succession planning so vital for tax advisory practices?

By exploring these nuances, you can better appreciate the tax advantages and responsibilities that come with running a Co-op. Understanding Co-op Taxes Key Tax Deductions and Credits Taxplanning tips for a Co-op Final Thoughts on Understanding Co-op Taxes Partner with Harness for Expert Tax Support What Is a Cooperative (Co-op)?

Whether you are contemplating forming an LP or already operate one, gaining clarity on tax matters can optimize your financial outcomes and ensure compliance with state and federal regulations. Identifying and leveraging these opportunities is a vital part of effective taxplanning.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content