This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

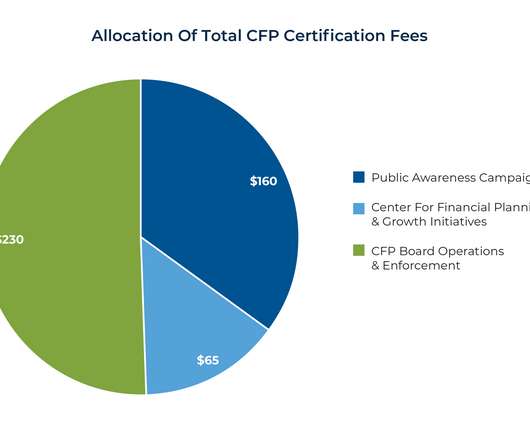

Amid estimates that nearly 40% of all financial advisors are likely to retire in the next 10 years, the need for a new generation of advisor talent is clear.

Also in industry news this week: Top Democratic Senators are urging the Treasury Department to crack down on a range of estate planning strategies for high-net-worth individuals, including GRATs and IDGTs Amid fallout from recent bank failures, both Republicans and Democrats are considering whether current FDIC insurance limits should be increased (..)

In the mid-20th century, the first phone call for a person who needed guidance on saving or planning for retirement was likely to be to a stockbroker or a mutual fund or insurance salesperson.

Let’s be honest, retirement isn’t what it used to be. The traditional blueprint of working until 65, collecting a pension, and retiring feels outdated, especially for mid-level professionals who’ve started thinking early about what their ideal retirement should look like. What’s the earliest you can retire?

And for those looking to become such professionals, the question naturally arises: Is pursuing the Certified Financial Planner (CFP) certification worth it in India? What is the CFP Certification? The Certified Financial Planner (CFP) certification is widely regarded as the gold standard in personal financial planning.

Key Takeaways: The last two years have been marked by the highest inflation rates in decades; your clients saving for retirement can use this to their advantage through short-term investments, tax deferral, and insurance products offering better benefits. For many people, this might mean retirement. 5%, never even topping 1%.

By Bryson Milley, CFP, CIM One of the questions I’m most asked by retiring clients is, “How do I manage my investments once I’m retired?” A retirement investment portfolio is like owning an apartment building. And when you retire, you stop construction and begin filling the building with tenants. Managing the building.

Early retirement has become a popular financial goal. Even if you never retire early, just knowing that you can is liberating! Can You Really Retire at 50? Can You Really Retire at 50? Table of Contents Can You Really Retire at 50? FAQs on Retiring Early at 50 It’s a big bold claim – retire at 50?

And this is precisely what the CFP® certification is built to instil. The CFP® program isn’t just about mastering technical modules on investment planning, taxation, retirement, or insurance. It means asking better questions, filtering out noise, and grounding every action in logic, not emotion. It builds a mindset.

So much of our world is filled with abbreviations surrounding insurance and investment products, processes, education and accomplishments. . Translating from the secret language of financial planning, the sentence would read “Tammy specializes in insurance. Professional Certifications for Financial Advisors.

This certification is recognized globally and showcases a deep, systematic understanding of personal financial management, including investment planning, risk management, tax planning, and retirement planning. Individuals who earn this certification are thoroughly prepared to offer expert financial advice.

At the heart of this profession lies the financial planner certification, a credential that not only signifies expertise but also opens doors to significant career opportunities. This certification is recognized globally and is considered a benchmark for competence and professionalism in financial planning.

Keep the following documents for one to three years: Paystubs Bank records Insurance policies Investment statements Mortgage statements Receipts for charitable contributors All business-related documents. Some documentation has no expiration date, such as birth certificates and social security cards. for insurance purposes.

Their wisdom extends to suggesting tax-efficient avenues for pivotal life moments, be it education or the golden years of retirement. While many financial advisors find their niche in investment firms, banks, and insurance sanctuaries, some trailblazers opt for independence, establishing their advisory havens. Where Do They Shine?

Where CFP® Really Comes In This is where the Certified Financial Planner (CFP®) certification makes a real difference. It’s not just a certification. Are you trained to discuss term insurance but hesitant to ask about family dynamics? • Its a whole new way of thinking. Are you available online but emotionally disconnected?

Fee-only firms are unique as they do not receive commissions from selling financial products, such as insurance policies or investment products. The ability to advise on standard financial planning matters such as retirement planning should be table stakes (if not, red flag). Do you have a unique situation?

Which decade should you really start to plan for retirement? This might mean going back to school to earn a master’s degree or a professional certification. Proper insurance coverage: One of the biggest risks for many people in their 30s is they’re still acting as if they’re invincible. Build your positive financial behaviors.

You can request a social security number along with your baby’s birth certificate. Update your life and disability insurance. Now more than ever you want to have appropriate life and disability insurance coverage, so if something unexpected happens your family will be OK. Start saving for college now.

Certificates of Deposit . Certificates of Deposit. Index funds have become popular among the FIRE (financial independence, retire early) crowd, and for a good reason. This strategy works best when you already have a solid plan for your retirement and your other financial ducks are in a row. Certificates of Deposit.

You are building your emergency fund, saving for a car or home down payment, or getting ready to retire and want to know where to park your short-term cash. You can visit bankrate.com to see the current yields for many FDIC-insured high yield savings accounts. Current rates are 3.75%-4.30%.

The Actual Expense Method opens up possibilities for larger deductions, particularly for newer or luxury vehicles, by allowing you to deduct the business percentage of real costs, including fuel, maintenance, insurance, and depreciation. To maximize these benefits, it is essential to understand what qualifies as deductible travel.

Even though the federal government has rescued SVB and guaranteed all deposits over the FDIC insurance limit of $250,000 per account, that doesn’t mean they will be doing it again for other banks. Let’s review and recap how Federal Deposit Insurance Corporation (FDIC) insurance works and what other alternatives are available.

This group of categories includes: Retirement account contributions e.g. 401k/403b/IRA Non-retirement investing (e.g. Before you pay any bills or do any shopping, a portion of your earnings should be diverted into your retirement account, if possible, for your future self and your emergency savings accounts for a rainy day.

Laying the foundation with a basic emergency fund, securing adequate life and health insurance, beginning investments for her child’s education, and planning early for retirement are essential steps toward building long-term financial security.

The financial planning and insurance industry offers a dynamic career path with immense growth potential. In this blog, we will explore the benefits of pursuing short-term courses in the insurance planning industry and how they can help you unlock your dream job with guaranteed placements.

Studies by the American College of Financial Services show that 90% of special needs family members and caregivers admit that caring for their loved ones is more important to them than planning for their own retirement. The eligibility criteria require you to have an approved Disability Tax Credit Certificate by the government.

The CFP® Fast Track course offers a quick, efficient pathway to certification, allowing you to accelerate your career in the financial planning industry. Unlike the regular pathway that requires passing multiple exams over a year, the fast track allows eligible candidates to take just one exam and complete the certification in 3-4 months.

The course covers an introduction to personal finance, credit cards, life insurance, health insurance, investment instruments, loans, income tax and planning, budgeting and building a strong portfolio. From the above concepts you will learn how to approach financials and plan for your retirement goals with good risk management.

The CFP certification stands as the gold standard in financial planning, offering professionals a comprehensive pathway to excellence in this dynamic field. The CFP certification prepares professionals for these challenges through rigorous training and practical application.

High-Yield Certificates of Deposit. High-yield savings accounts come with FDIC insurance , meaning your deposits are federally protected in amounts up to $250,000 per depositor per account. High-Yield Certificates of Deposit. No minimum deposit required * No maintenance fees * 24/7 access to your funds * FDIC insured.

This article will discuss the basics of financial planning , the education and certifications required to become a financial planner, and how to develop your financial planning skills and network. Education and Certifications for Becoming a Financial Planner Are you interested in becoming a financial planner?

It wasn’t too long ago when investments would mean going to the bank and following the advice of the bankers or calling in neighborhood uncle to buy term-deposit certificates or insurance. You’d perhaps need to undergo special certifications as you enter the industry but MBA (Finance) remains a good starting point.

Certificates of Deposit (CDs) . The best high-yield savings accounts are FDIC-insured, so you are protected up to $250,000 per depositor per account. Opening a brokerage account lets you invest for the future outside of a retirement account, allowing you to access your money by selling shares at any time without waiting until age 59 ½.

out of 5 stars in the App Store Best for No Fees CIT Bank Our Partner Open an Account Annual Percentage Yield (APY) 1.90% Minimum Account Balance $100 Monthly Fees None FDIC Insured? Like other savings accounts that made our ranking, CIT Bank is also FDIC insured. Yes Yes Yes Yes Yes Yes Mobile App Rating 3.4 Yes Mobile App Rating 3.4

Some common career paths for investment advisors include working as wealth manager, family office, portfolio manager (PMS), Retirement Planner, Estate Planner. Investment advisors can also specialize in specific areas such as retirement planning, tax planning, or portfolio management. Excellent communication and interpersonal skills.

Curriculum and Faculty: The Pillars of Excellence The financial planning curriculum focuses on investment strategy, taxation, retirement planning, insurance, portfolio management and estate planning, and. The Importance of Financial Advisory Certifications In the field of finance, certifications like CFP® hold a lot of significance.

Boost your retirement savings Now that you have excess money in the bank, it may be a smart time to increase your retirement savings. One in four Americans don’t have any retirement savings whatsoever, explains Yahoo Money. How many IRAs can you have in your retirement strategy? Click to grab your copy!

The simplest definition of the role of a financial advisor would of that of a person who helps individuals, families, and organizations make decisions related to their investments, taxes, insurance planning, retirement planning, estate planning, and money management. Insurance Companies. Banks & NBFCs. Brokerage Firms.

Financial institutions based in GIFT City can treat their operations, investments, and deposits as offshore, enabling Indian banks, NBFCs, insurance providers, and capital market entities to offer global financial products in foreign currencies.

Understand the Role of a Financial Advisor A financial advisor is an expert who provides guidance and recommendations on diverse financial matters, including tax strategies, investments, insurance, and retirement planning. To excel as a financial advisor, you need to possess a specific set of skills and qualities.

It can enable physicians to set realistic and achievable financial goals, such as purchasing a home, preparing for retirement, or saving for a child’s higher education. Financial advisors can also help physicians cater to significant life goals like saving for retirement.

Credentials matter in any profession and when it comes to personal finance, there’s no certification more highly coveted than Certified Financial Planner. Earning the CFP designation requires a rigorous course of study covering investment planning, income taxation, retirement planning and risk management.

Insurance Advisor. An insurance advisor’s primary job is to help customers find the best insurance products for their short- and long-term needs. This covers all areas of insurance – from life and home/auto coverage to financial planning services. Average salary: $89,295 per year. Hedge Fund Manager.

A Roth IRA is a type of investment account that lets you invest after-tax dollars for retirement. From there, your money can grow tax-free, and you can withdraw your funds without having to pay income taxes once you reach retirement age. High-yield savings accounts or certificates of deposit (CDs) offered by banks and credit unions.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content