This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

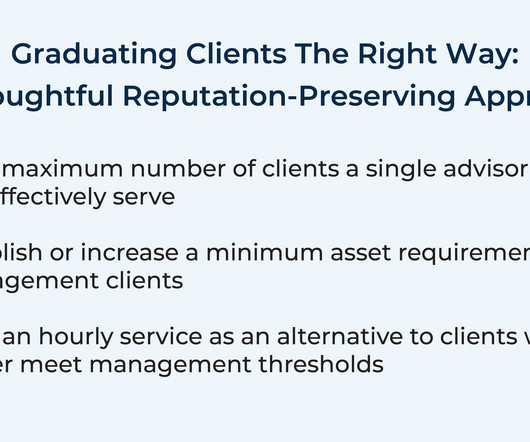

Early in a firm's life cycle, a founder might take on nearly any client (and their fees) just to generate enough revenue to 'keep the lights on'. However, as the firm grows, some of those early clients may no longer be profitable to serve – especially if they generate lower fees than newly onboarded clients.

Paul is the CEO of More Clients More Fun, a marketing company that helps financial advisors conceptualize and publish their own book in a consolidated 6-week process. Welcome everyone! Welcome to the 417th episode of the Financial Advisor Success Podcast ! My guest on today's podcast is Paul G McManus. Read More.

It's natural for advisors to begin discovery meetings by asking questions about a client's current financial situation – understanding cash flow, debt, investments, risk tolerance, or even the burning tax concern that brought them to the advisor's door in the first place is crucial for financial planning.

The necessity of fee increases entails a certain amount of pain for monthly-fee advisors since each conversation around raising fees creates the possibility of pushback from clients that could put a strain on the client-advisor relationship. Read More.

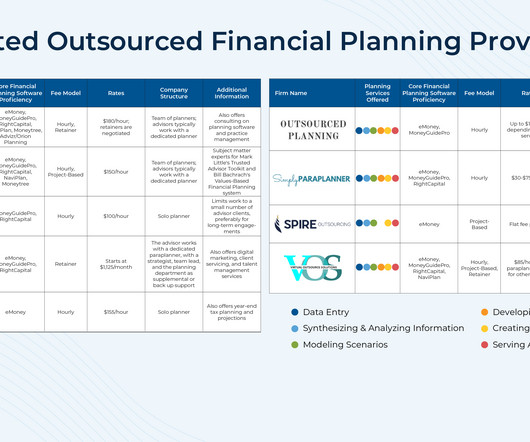

Reviewing both current marketing efforts and aspirational goals for client engagement can help advisors determine where outsourcing may add the most value. Advisors may also want to consider a contractor's communication style and marketing philosophy to assess compatibility with the firm's values.

Kevin is the CEO of Connecticut Wealth Management, an RIA based in Farmington, Connecticut, that oversees approximately $4 billion in assets under management for 1,100 client households. My guest on today's podcast is Kevin Leahy.

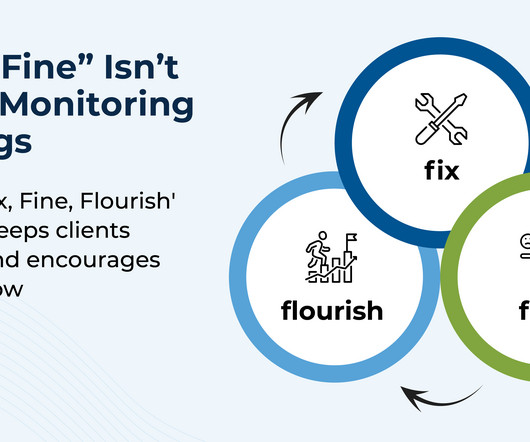

When a client first begins working with an advisor, the relationship is often marked with a flurry of onboarding tasks, immediate issues to resolve, and long-term planning goals to establish. And as clients come into monitoring meetings, they may increasingly describe their situation as "fine", with no pressing issues to address.

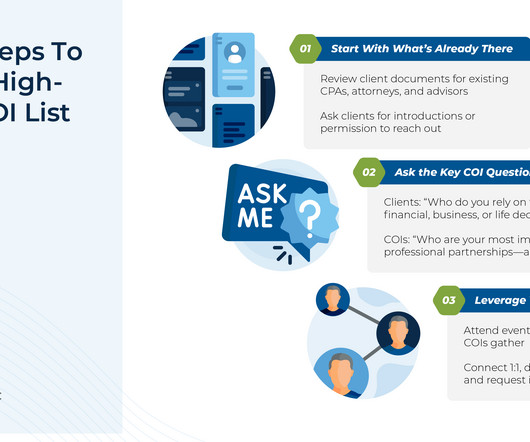

When cultivated with care, these relationships can become valuable sources of client referrals and collaborative insight – especially because COIs and advisors often work with similar client profiles. Centers Of Influence (COIs) play a vital role in the growth and service capabilities of a financial advisory firm. Read More.

The typical prospecting process involves multiple meetings, and a fairly common response for advisors to hear after giving their 'pitch' is that the client needs some extra time to think about it. I can only onboard 3 clients in a given quarter. Read More.

FINNY AI, an AI-powered prospecting tool, has raised $4.2 FINNY AI, an AI-powered prospecting tool, has raised $4.2 FINNY AI, an AI-powered prospecting tool, has raised $4.2

Vanessa is the CEO of Expressive Wealth, an RIA based in Chicago, Illinois, that oversees $135 million in assets under management for approximately 70 client households, including 10 ‘core' ultra-high-net-worth families.

Gideon is the CEO of Drucker Wealth, a hybrid advisory firm based in New York City, that oversees approximately $1 billion in assets under management for 800 client households.

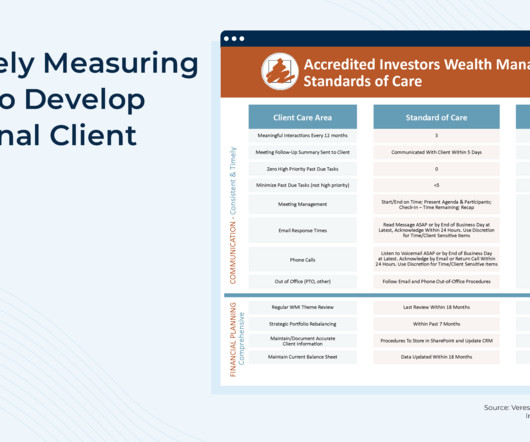

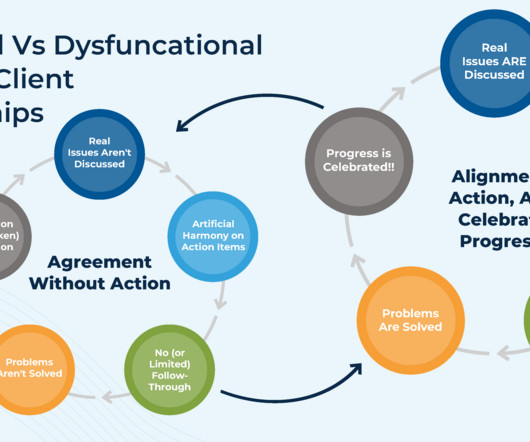

Most financial advisors strive to provide excellent client care and prioritize a systematic process to maintain regular communication with their clients both on a scheduled (e.g., Suddenly, the question of, "What does it mean to provide the best care for clients at this firm as a team?" becomes a crucial one to solve.

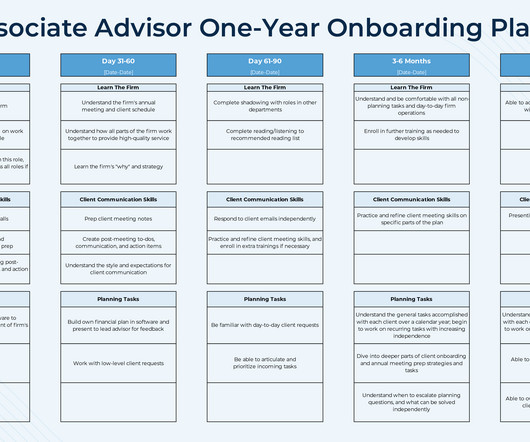

We have provided an onboarding plan template for advisors to download, which breaks up the skills list into two primary categories: 1) clientcommunication skills (e.g., meetings, email communication, and phone calls), and 2) technical skills (e.g., building an initial financial plan). Read More.

In the early days of financial planning, serving clients often meant developing transactional relationships focused on facilitating trades and selling insurance. Over time, advisors shifted toward more analytical approaches, such as investment management and retirement planning.

Stacey is the chief operating officer of Morton Wealth, an RIA based in Calabasas, California, that oversees approximately $3 billion in assets under management for 1,300 client households.

I help clients in retirement by doing X, Y, and Z."). For these clients, connection and understanding are often more important than problem-solving, and advisors who focus too quickly on identifying potential future issues risk alienating these prospects. However, not all prospects have immediate financial concerns.

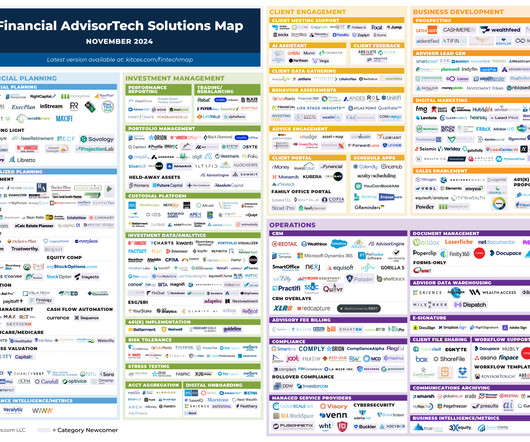

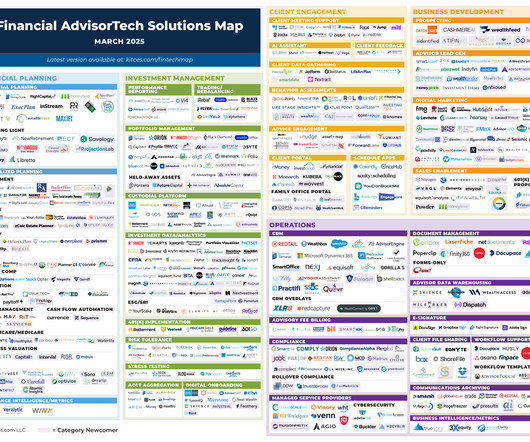

And while Black Diamond has cut a deal with Morningstar to be the 'default' option for Office advisors to move to, a host of other portfolio management platforms are offering their own incentives as well, leaving Morningstar Office advisors with an opportunity to evaluate a large and crowded landscape of options to find the platform that will work (..)

In the modern era of financial advice, the advicer/client relationship is tightly centered on trust. Then, because the client isn't "bought in" to the recommendations, they simply don't act on what the advisor recommends.

But some advisors who choose to take more time off from their schedules might be concerned that prospects and clients will consider them to be less committed to serving their planning needs than other advisors. Notably, the choice of work schedule can affect the type of client with whom an advisor might want to work.

Establishing successful client relationships as a financial advisor relies on good communication skills not just to present information persuasively and with confidence, but also to establish client rapport that allows meaningful and engaging relationships to be built.

Eric is the Chief Financial Advisor and Co-Owner of Econologics Financial Advisors, an independent RIA based in Largo, Florida, that generates more than $4M of revenue while working with nearly 300 client households.

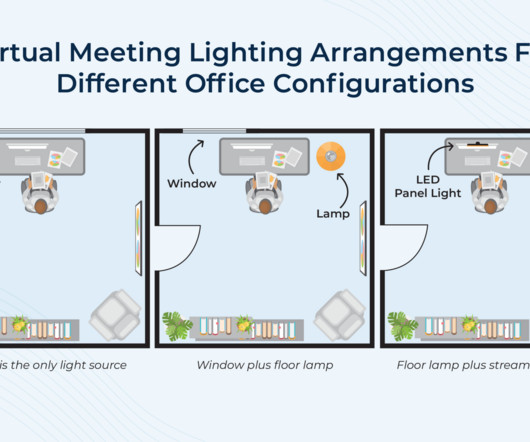

Traditionally, financial planning meetings have been held face-to-face in an advisor's office, and over the years, a body of research has emerged showing that how the advisor's office is laid out can have a significant impact on how clients perceive the advisor, their mood during the meeting, and even their resulting financial planning decisions.

When a firm becomes large enough, though, the firm owner may be compelled to consider stepping away from their long-standing work as a client-facing financial advisor into a more pronounced business leadership role to manage the growing business.

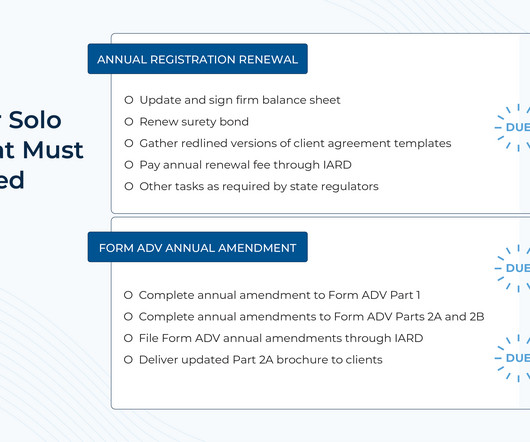

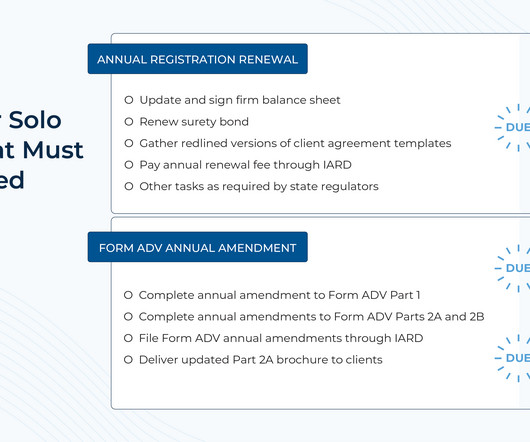

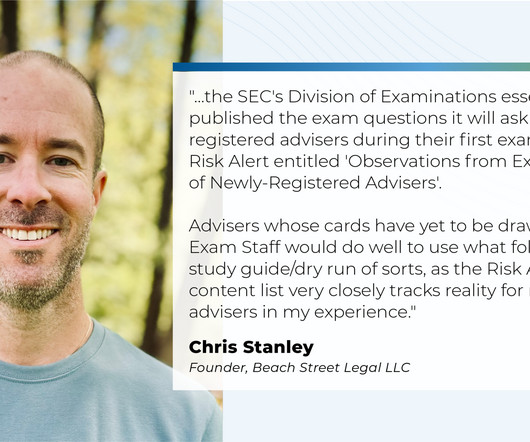

The 1st category of tasks that advisory firms must handle involves renewing their registration with the applicable state(s) in which they do business each year, which typically involves submitting select documents (e.g., Read More.

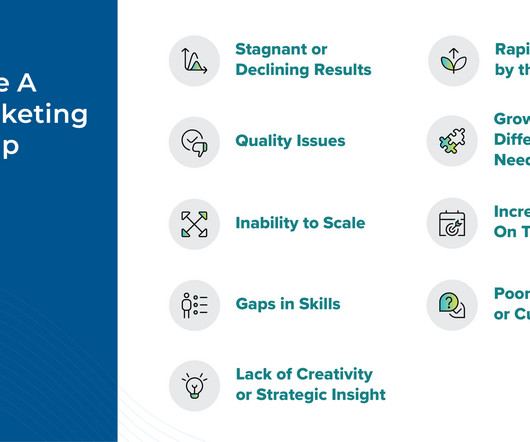

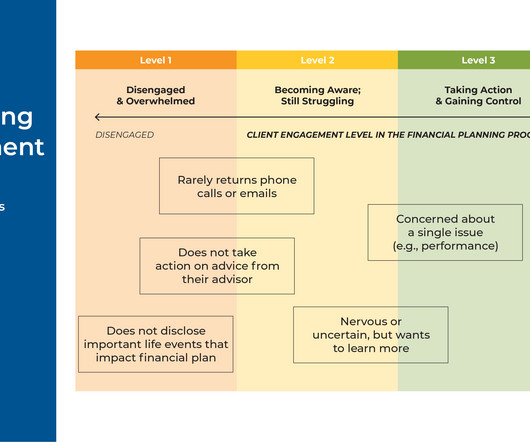

After advisors do all of the work of bringing on a new client (Marketing! And while all may appear well on the surface – the client rarely contacts the advisor with problems but they show up for every annual meeting – they may actually be feeling quite disengaged with the financial planning services being provided.

Eric is the Managing Partner of Prospero Wealth, an RIA based in Seattle, Washington, that oversees $52 million in assets under management for 80 client households.

Measuring a client's tolerance for risk is an essential (and required!) step when onboarding a new client, as making any sort of recommendation is impossible without first understanding how comfortable clients may be when their portfolios inevitably experience volatility. And while few (if any!)

The 1st category of tasks that advisory firms must handle involves renewing their registration with the applicable state(s) in which they do business each year, which typically involves submitting select documents (e.g., Read More.

Measuring a client's risk tolerance is both an art and a science. Beyond assessing how a client feels in the moment, advisors must evaluate a client's long-term behavioral tendencies, actual risk capacity, and financial goals – all of which require considerable time and skill.

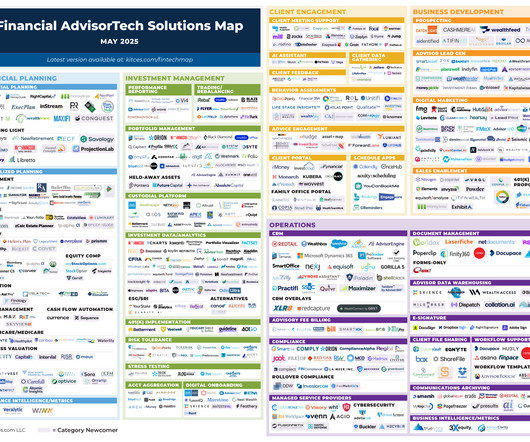

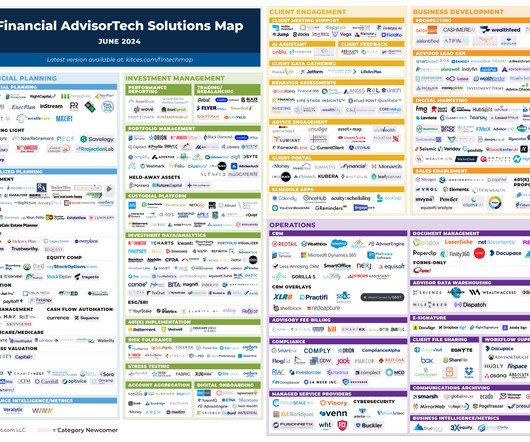

This month's edition kicks off with the news that 'startup' custodian Altruist has completed a $169 million fundraising round as it continues to rebuild the RIA custodial tech stack layer-by-layer while positioning itself as the biggest RIA custodian built from scratch and solely for advisors – which, while making it the clear #3 custodian behind (..)

For most financial advisors today, a website is a critical tool that allows them to market their services and communicate their fees to potential clients. This can help prospects decide whether the working relationship would be a good fit for them and give them greater confidence in the value of hiring the advisor.

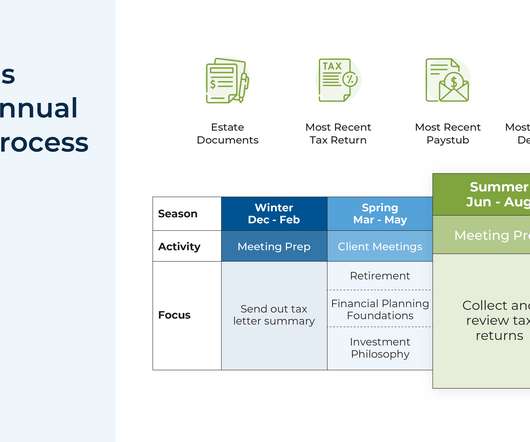

A common service model for many financial advisory firms is to schedule annual client meetings throughout the year where the advisor meets with each client in the month they started working with the firm, and conducts a comprehensive review of all planning topics for the client.

Read the analysis about these announcements in this month's column, and a discussion of more trends in advisor technology, including: Brand design consultancy firm Intention.ly

However, when these aspirations are delayed or blocked by senior advisory firm partners who choose to delay their retirement plans, it can leave younger advisors frustrated and in a place of uncertainty about their futures with their firm.

For many financial advisors, setting asset minimums helps ensure that their firm can generate enough revenue to maintain business costs and compensate the advisor appropriately. A simple way for advisors to educate prospects about asset minimums is to include the information on their firm’s website.

Stacey is the President of Envision Financial Planning, an independent RIA based in Memphis, Tennessee, that oversees nearly $200 million in assets under management for 206 client households.

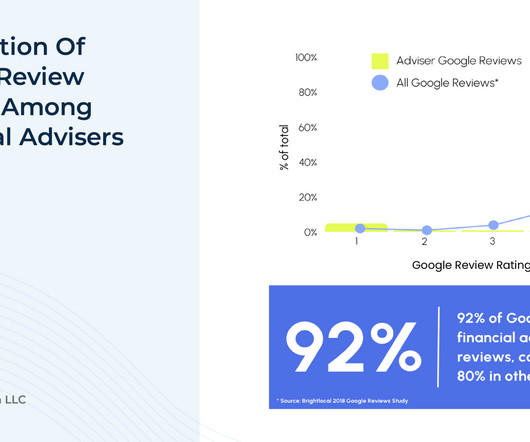

Nonetheless, fewer than 10% of SEC-registered investment advisers report using them, even though the SEC’s updated investment adviser marketing rule allows financial advisors to proactively encourage testimonials (from clients), use endorsements (from non-clients), and highlight their own ratings on various third-party review sites.

However, at a certain point, initial business growth goals will have been met, leaving the business owner at a crossroads of deciding where to take the business next – should they maintain the firm’s current size or continue the growth trajectory and adapt to the firm’s growing needs to bring on more clients?

Regardless of the size of a financial advisory firm, clients are a constant necessity to sustain a profitable business. As a starting point, there are unconventional marketing principles that can help advisors who do not want to engage in traditional marketing campaigns to effectively attract and acquire clients.

Which means the firm will need to provide records of holdings and transactions for each of its clients (which may require some training and practice for employees to be able to quickly pull the needed data from the firm's custodian), as well as archived clientcommunications and any advertisements produced by the firm.

When a financial advisory firm owner first starts their business, much of their time is spent on finding clients that they can serve. But as they (hopefully) onboard more clients and get busier with servicing those clients, they will also find that they eventually start to run short on time.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content