This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

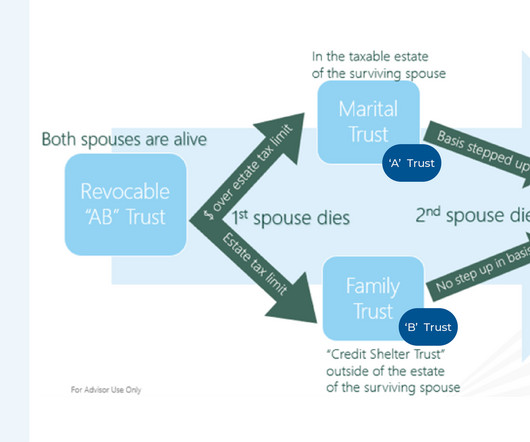

In recent years, the Internal Revenue Code (IRC) has endured some drastic changes resulting from legislative action that have altered the strategies estateplanning professionals have recommended to clients. For instance, prior to the 2017 Tax Cuts and Jobs Act (TCJA), "A/B trusts" had become ubiquitous for spousal estatetaxplanning.

Estateplanning is one of the most important steps in securing your financial legacy, but its also among the most complex. Understanding how assets will be distributed, navigating tax implications, and aligning these decisions with your personal goals can feel overwhelming.

morningstar.com) Early in retirement is the time to do some taxplanning. nextavenue.org) Estateplanning Mistakes to avoid in your estateplanning. theretirementmanifesto.com) If you have a valuable collection you need a plan for its eventual disposition.

While asset protection is a popular planning topic for High-Net-Worth (HNW) and ultra-high-net-worth clients, those who are not HNW are susceptible to the same threats to wealth. Notably, certain client assets have built-in creditor protection without the use of (often expensive) products or tools.

As the year comes to a close, now is the time to review potential financial moves to help minimize your tax burden heading into 2025. Proactive year-end taxplanning can lead to significant savings and set you up for financial success in the new year.

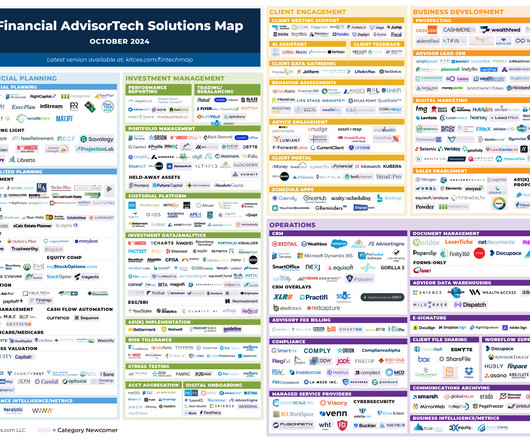

Welcome to the October 2024 issue of the Latest News in Financial #AdvisorTech – where we look at the big news, announcements, and underlying trends and developments that are emerging in the world of technology solutions for financial advisors!

million in assets to both retire and pass on a legacy interest (though many have yet to establish an estateplan), according to a recent survey. Enjoy the current installment of "Weekend Reading For Financial Planners" – this week's edition kicks off with the news that affluent Americans believe they need an average of $5.5

Benefits of Waterfall Wealth Management Managing significant assets can be complex. Key benefits include: Ensuring essential financial obligations are met first – Taxes, estateplanning, and retirement savings take precedence. Strategic long-term planning – Provides a roadmap for surplus wealth allocation.

Insurance and financial fee deductions Insurance represents a necessary expense for protecting your business assets and operations, with premiums for various types of coverage qualifying as fully deductible business expenses. To maximize tax benefits while maintaining healthy cash flow, businesses should thoroughly understand these options.

While there are certainly ways to do estateplanning without a lawyer, for most people hiring an estateplanning attorney makes the most sense. Estateplans can get complex fast, and even fairly straightforward estates can feel overwhelming if you’re not trained in the area. Do your research.

They can help you diversify your money across various asset classes and reduce your portfolio’s risk while aiming for consistent returns. A financial advisor can craft tax-efficient withdrawal strategies to minimize the tax burden on your retirement income. Taxplanning is not solely about federal taxes.

With the fee-for-service model, you can customize service offerings for clients seeking advice who don’t (yet) have traditional portfolio assets to transfer to your firm’s custodian for full-time management. This approach allows you to engage these clients by charging a fee that’s covered through their monthly cash flow.

In this comprehensive guide, we’ll explore proven strategies to help you minimize tax liability while staying compliant with current regulations. From maximizing deductions to managing capital gains, we’ll cover everything you need to know about smart taxplanning.

When there’s an opportunity to take advantage of current tax rates depending on your income level, conversions allow taxpayers to move money from before tax retirement accounts growing tax-deferred to after tax dollars growing tax free.

This tax benefit is scheduled to sunset at the end of 2026. Taxplanning for 2026 Depending on your situation, income, and goals, your planning options will vary. As with anything in taxplanning, it’s important not to let the tax-tail wag the dog.

The post Part 1: The Tools of the Tax-Planning Trade appeared first on Yardley Wealth Management, LLC. Part 1: The Tools of the Tax-Planning Trade Whether you’re saving, investing, spending, bequeathing, or receiving wealth, there’s scarcely a move you can make without considering how taxes might influence the outcome.

The post Part 1: The Tools of the Tax-Planning Trade appeared first on Yardley Wealth Management, LLC. Part 1: The Tools of the Tax-Planning Trade. Whether you’re saving, investing, spending, bequeathing, or receiving wealth, there’s scarcely a move you can make without considering how taxes might influence the outcome.

Part 3: Tax-Wise Financial Planning In our last two pieces, we covered some tools of the tax-planning trade, as well as how to deploy them for tax-efficient investing. But taxplanning isn’t just for your investments. But we can weave each event into the tax-planning fabric of your financial life.

Part 3: Tax-Wise Financial Planning. In our last two pieces, we covered some tools of the tax-planning trade, as well as how to deploy them for tax-efficient investing. . But taxplanning isn’t just for your investments. Each can translate into tax-planning challenges and opportunities: .

Only 26% of Americans have an estateplan. If you’re thinking, “But my clients are high-net-worth…many more have an estateplan.” These numbers show an opportunity for tax practices to build deeper, meaningful relationships with their clients, helping them to navigate some of life’s most challenging financial decisions.

Part 2: Tax-Wise Investment Techniques In our last piece, we introduced some of the tools of the tax-planning trade. In other words, your tax-planning techniques matter at least as much as the tools. Tax breaks come and go, and are beyond our control. It’s another to make best use of them.

Part 2: Tax-Wise Investment Techniques. In our last piece, we introduced some of the tools of the tax-planning trade. These include tax-sheltered accounts for saving toward retirement, healthcare, and education, as well as tax-efficient tools for charitable giving, emergency spending, and estateplanning. .

This flexibility allows for more sophisticated estateplanning strategies and continued tax-free growth throughout retirement. Why investors sought recharacterizations before 2018 Market volatility frequently triggered recharacterizations when converted assets suffered significant losses.

According to a Fidelity study, 45 percent of younger investors are more inclined to consolidate their assets with one advisor as opposed to spreading assets across multiple advisors. Starting Out clients are typically focused on beginning to build wealth.

Your business advisory team may consist of: a business broker or M&A advisor, accounting and tax advisors, and transaction/M&A attorney. On the personal side, your financial advisor , estateplanning attorney, and CPA/tax advisor should be involved throughout the process.

Blind Spot 3: Inadequate estateplanning In today’s age, where 60 is the new 50 and people are more active and health-conscious than ever before, it is common to think that estateplanning can wait. Life is inherently unpredictable, and unanticipated circumstances can arise at any moment.

Long-term goals typically encompass retirement planning, wealth preservation and estateplanning. Your risk tolerance will influence your investment strategy and asset allocation. They are well-versed in various aspects of financial planning, including investments, retirement planning, estateplanning and tax management.

The six-person team, led by managing partner, wealth advisor, Ty Vogele, and wealth advisors David Guenthner, CEPA ® and Ryan Wittman, AIF ® , manages over $400 million in assets. Now, we have the resources and support to deepen client relationships and explore innovative financial planning solutions.

Gift Tax Exemptions Each year, you can give up to $17,000 to any number of people tax-free. This means that if you have two children, you can give each of them $17,000 without a tax penalty in 2023. [1] 1] This can be something you do as part of your estateplan.

Arun Thukral, New CFP Framework is different from other financial courses as it focuses on the practical aspects of financial planning. CFP course covers topics such as investment planning, retirement planning, estateplanning, and taxplanning.

Middle-income individuals often gravitate more towards safer investment options and prefer predictability over the volatility associated with riskier assets. Deductions for mortgage interest, property taxes, and depreciation can significantly mitigate their tax liabilities and enhance the appeal of real estate as an investment avenue.

Taxes should always be a component of any investment decision — but not the main driver. Individuals who inherit a concentrated stock position should speak with their estateplanning attorney to confirm whether they’ll receive a step-up in basis. If so, there might not be any material tax impact from selling shares.

Long-term goals typically encompass retirement planning, wealth preservation and estateplanning. Your risk tolerance will influence your investment strategy and asset allocation. They are well-versed in various aspects of financial planning, including investments, retirement planning, estateplanning and tax management.

The CFP Program Structure Comprehensive Curriculum Design The CFP program offers a unique 4-in-1 certification structure that covers all essential areas of financial planning: Investment Planning: Understanding market dynamics, portfolio management, and asset allocation strategies Retirement and TaxPlanning: Mastering retirement solutions and tax-efficient (..)

This tax benefit is scheduled to sunset at the end of 2026. Taxplanning for 2026 Depending on your situation, income, and goals, your planning options will vary. As with anything in taxplanning, it’s important not to let the tax-tail wag the dog.

Employed by law firms, corporate legal departments, or running their own practices, tax attorneys can be looked to for legal tax issues and disputes, along with comprehensive taxplanning and preparation.

High-Net-Worth Individuals (HNWIs) have a net worth of $1 million or more in liquid assets. In general terms, a high-net-worth individual is someone with substantial wealth and a mix of liquid assets, such as cash, stocks, and bonds, as well as non-liquid assets, such as real estate and privately-held businesses.

It details your current money situation and financial system, including investing, saving, retirement, and estateplanning. So, what is a financial plan, in simple terms? Insurance is essentially your backup plan, protecting your assets in the event a life circumstance occurs that requires a large amount of money to resolve.

It demonstrates to employers, peers, and clients alike that the holder possesses a comprehensive understanding of financial planning concepts, including retirement, taxplanning, investment management and estateplanning. From a client’s perspective, working with a CFP® offers a sense of security and trust.

The wealth manager offers advisory services or multiple products, including mortgages, retirement plans, stock options, taxplanning, bonds and real estate investment. He is an advisor who charges a certain percentage of clients’ total assets. . Planning services . Taxplanning services .

If the services you currently provide focus on investment management and basic financial planning, advice related to estateplanning and settlement, wealth transfer, and taxplanning are good value-added services to investigate. And then determine that insurance will be reviewed in the odd years.

In this comprehensive guide, we will explore the intricacies of NUA, its benefits and considerations, and provide practical insights to help you make informed decisions regarding your retirement assets. NUA is a tax strategy that applies to individuals who hold employer stock within their employer-sponsored retirement plans, such as a 401(k).

Several of the wealth managers had specialists in-house such as: Chief Philanthropic Advisor, Head of TaxPlanning, Family Legal Counselor, Trust Officer If you can’t hire these specialists, work out an arrangement with a close third-party with this expertise. Wear a suit and present yourself conservatively.

Financial planning is about understanding and utilizing your assets in a manner that helps you and your family work towards achieving your goals and meeting your needs. While it may seem like a luxury that is only available to the wealthy, anyone is capable of building an effective financial plan and putting it into action.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content