This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In recent years, financial advisors have increasingly embraced tax planning as a core element of delivering value to clients. But as the profession has evolved toward more holistic planning, tax considerations have likewise expanded into more areas of advice, including Roth conversions, charitable strategies, and small business structuring.

Tax deductions can save you thousands annually by reducing your taxable income through legitimate business expenses. Understanding these deductions is more critical than ever as tax laws evolve, presenting new opportunities for savings. Understanding this distinction is crucial for maximizing your tax benefits effectively.

These alternative investments can offer distinct advantages in the shape of portfolio diversification and the potential for higher returns, but they can come with equally distinct tax complications that need to be carefully planned for. What are the key tax strategies for alternative investments in 2025?

Seth is the founder of Heartwood Financial Planning, an advisory firm affiliated with PlanMember Securities Corporation that is based in Fresno, California, and oversees approximately $100 million in assets under management for 850 client households.

Without proper planning, taxes can unexpectedly take a large bite out of the proceeds, potentially reducing financial security and the legacy. When you understand various exit strategies and their tax implications early, you position yourself to make informed decisions that maximize after-tax value while ensuring a smooth transition.

As the year comes to a close, now is the time to review potential financial moves to help minimize your tax burden heading into 2025. Proactive year-end tax planning can lead to significant savings and set you up for financial success in the new year. Find your next tax advisor at Harness today. Starting at $2,500.

Freelancers and contractors may enjoy greater flexibility and independence than full-time employees, however, this autonomy brings increased tax responsibility. Unlike W-2 employees, freelancers and independent contractors are responsible for managing their own tax obligations, which can be a complex process.

Tax season can feel overwhelming, whether you’re filing for the first time or you’ve been doing it for years. Should you tackle your taxes on your own, or is it time to bring in a professional? Lets explore the pros and cons of DIY tax preparation and when seeking expert help might be the right move.

As dynamic as the secondary market may be, secondaries come with complex tax implications that can significantly impact returns if not properly managed. What are the tax implications of secondary transactions? What are the tax challenges in secondary transactions? What tax strategies optimize secondary investments?

Tax planning serves as the cornerstone of the entire acquisition deal, extending far beyond a simple checkbox. Every element, from structure to price negotiations, hinges on understanding tax implications for all parties involved. Get it right, and you will have set yourself up for a smooth transition and maximized returns.

April 15 marks the IRS tax return filing deadline for 2025. Although this is the traditional tax filing deadline, given the spate of recent natural disasters (such as the California wildfires and Hurricane Milton), the IRS is granting certain filing and payment extensions beyond this date.

In this article, well examine the nature of IRS audits, the common audit red flags that result in IRS scrutiny, and how professional tax advisors can help reduce the risk of you being audited. An IRS audit is a formal review of your financial records to verify their accuracy and compliance with tax laws.

Document Management: Microsoft SharePoint SharePoint is the reason we’re in the whole Microsoft ecosystem. Copilot can very easily look across all of our Teams meetings, all of our SharePoint documents, our emails, etc. But again, we’ll continue to support both because of that client experience transition challenge.

And also, you know, there are really nice tax planning mechanisms that people can use to help them achieve, achieve those things as well. It shouldn’t be just something you think about when you’re at your estate attorney and you’re signing a document and that’s the last you see of it. Exactly that.

However, as appealing as these forms of compensation may be, they can result in sizable and unexpected tax bills. Along with the 83(b) election, there is a less well-known provisionthe 83(i) election that offers other tax advantages to certain types of employees. Table of Contents What is an 83(i) election?

Here are a few things to consider: Your income Family size and additional income Existing insurance coverage Net worth Current portfolio and retirement assets Did you just start a family, buy your first or second home, or start your own business? One of the most common reasons people put off creating one is a perceived lack of assets.

Understanding how assets will be distributed, navigating tax implications, and aligning these decisions with your personal goals can feel overwhelming. The software connects with Orion, our portfolio managing software, ensuring that investment assets are automatically included, providing an accurate snapshot of the entire estate.

When considering the various business structures available, understanding the tax implications is crucial for making informed decisions. A Limited Partnership (LP) offers a unique blend of operational flexibility and liability protection, but its tax treatment can be complex. Table of Contents What Is a Limited Partnership (LP)?

The rise of remote work and digital nomadism has made FEIE a common tax minimization strategy for Americans living abroad. What is the Foreign Tax Credit (FTC)? Financial and lifestyle considerations of living abroad The importance of professional tax advice for expats FAQs about the FEIE What is the Foreign Earned Income Exclusion?

Getting Started: What First-Time Planners Should Know Even for seasoned investors, key decisions around taxes, estate structure, and long-term income planning can carry significant implications. She wants to minimize taxes while aligning her legacy with charitable values.

Roth IRA conversions present a significant challenge for retirement planners: pay taxes now or later? Moving funds from traditional IRAs to Roth accounts triggers immediate taxation but promises tax-free withdrawals in retirement. One of the Roth IRA’s most compelling features?

Positioning Philanthropy as a Cornerstone of Legacy There are many reasons for giving during your lifetime, including supporting causes you care about, making a positive impact on the world, and accessing certain tax advantages. There are overall limits on charitable donation tax deductions, however.

Do you know how you will take money from your 401(k) or IRA, how you will take Social Security, how to be tax-smart with your income planning? Your advisor can help you decide which solution provides the most protection for you based on your income and assets. Its also how you plan your retirement income.

Private equity and alternative investments create unique tax reporting complexities that demand attention. This article explores the distinctions between K-1 and 1099 reporting, explaining their impact on tax planning, basis calculations, filing deadlines, and strategies to optimize your after-tax returns from alternative investments.

’ So they read it and they document it, they model it into the financial planning software, how it’s going to work when shares are coming in over time. And then pivoting over into, ‘Who does your taxes? To them it’s, ‘We need to understand all this.’ What’s their relationship with money?

Tax season is approaching, which means many people will be exploring the use of tax software to prepare and submit their tax returns themselves. While tax software certainly offers benefits, particularly when it comes to cost, the decision to use it isn’t nearly as straightforward as it may seem.

By Brady Marlow, CFP, AEP, CAP, CPWA, CExP , Director, Carson Private Client Wealth Strategy The emotional and psychological benefits of charitable giving are well documented. With careful planning, you may be able to reduce your tax bill or optimize the impact of your estate. This is, of course, a very individual decision.

Advisors who learn how to incorporate these and other emerging asset classes into Life-Centered Financial Plans will be offering a valuable service that sets them apart — especially in the eyes of high-net-worth individuals. But, to a growing segment of clients and prospects, these investments are almost as important as their 401(k)s.

Because many taxpayers earn too much to make pre-tax IRA contributions as they have a 401(k) at work. Although any investor with earned income can make a non-deductible contribution to an IRA (up to $7,000 in 2024-2025 if under age 50) and still take advantage of tax-deferred growth, it still may not be advisable. Yes and no.

The simplest form of estate equalization would be dividing all your assets equally by the number of children you have. You would divide all assets equally among beneficiaries, giving each person an equal percentage of each asset. Each of the two children in the prior example might receive different types of assets.

One of the most important aspects of developing a thorough estate plan is tax planning, as this has the potential to diminish the impact of your gifts and your loved ones’ inheritances. Let’s take a look at the tax impact and other considerations of each. million before triggering federal estate taxes).

And the third thing is documenting war crimes. And that’s actually something that Bridgeway Foundation knows a lot about, 00:13:33 [Speaker Changed] Documenting war crimes, 00:13:35 [Speaker Changed] Documenting. What do you do with all of that information once you’ve documented a war crime in Ukraine?

We start with several articles on retirement planning: Why considering a client's retirement time horizon and spending flexibility could lead to more accurate (and often higher) safe withdrawal rates than the simpler "4% rule" Four unique risks retirees face when drawing down their assets, from sequence of returns risk to tax risk, and how financial (..)

Charley Ellis : The research explosion happened in the seventies and then into the eighties, but the documents that you were looking at or thinking about, were all looking backwards, Give you the plain vanilla facts of what’s happened in the last five years in a standardized format with no analytical or insight available.

However, unlike stocks and bonds, alternative investments, or alts as theyre commonly known, have unique tax treatments and complex reporting requirements that investors should carefully consider before investing. Well also go into some potential strategies to optimize tax efficiency. How Are Alternative Investments Taxed?

If you have no estate documents, known as dying intestate , and no beneficiaries are listed, then distribution will follow your states intestate succession laws. If you had estate documents created, you want to make sure these designations match with the estate distribution flow in them, especially if trusts were created.

Asset and Liability Matching. Good financial planning is all about asset and liability matching across time. That means you need to make sure you understand how your income and assets relate to your expenses and liabilities. A financial plan with an asset liability mismatch is likely to fail over time.

Asset management Connecting investors to what matters most, so they can achieve their goals and make confident decisions. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting, and investment advice from an investment professional. Information in the U.S.

A living trust doesn’t help with asset protection purposes or remove the home from your taxable estate. Leaving a home to a spouse (if not owned jointly during life) or children in a willcauses those assets to pass through probate. Again, revocable living trusts avoid probate, but they don’t protect assets from creditors.

In my practice representing high-net-worth clients in estate and trust disputes, I often see how expectations, emotional baggage and vague documents can turn estate plans into battlegrounds. Related: Tax Court Rules $2 Million Bequest to Spouse Isn’t QTIP To prevent this, advise your clients to discuss their estate plans early and openly.

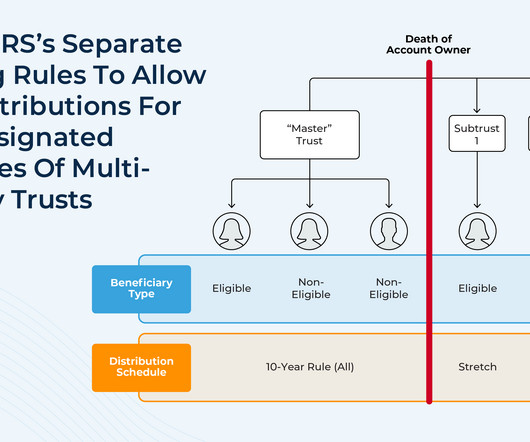

They might want to have more control over how the account assets are distributed to their beneficiaries. Notably, the IRS regulations only allow this 'separate accounting' treatment when the trust document includes a provision to divide the trust into separate subtrusts before the account owner's death. Read More.

The documents youll need at a minimum may include a will, durable power of attorney, and a health care power of attorney. Taxable investment accounts may be another option and provide additional tax diversity in your saving strategy. Early withdrawals can result in taxes, penalties, and lost growth potential.

At Rs 19,878 crore, net interest income climbed by 27%, and asset quality is significantly increasing. The company’s Profit After Tax (PAT) reached Rs 10,353 crore in FY25, growing by 33% from Rs 7,759 crore in FY24. Read all the related documents carefully before investing. Investments in securities are subject to market risks.

Start with important documents There are 3 main documents your clients will want to have in the event of their passing, or if something renders them unable to care for their farm, including: Will Durable power of attorney Medical advance directive These documents can be essential for clients with no farm family successors.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content