This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Also in industry news this week: NASAA has proposed an amendment to its broker-dealer conduct model rule that would restrict the use of the terms “advisor” and “adviser” for broker-dealers and their registered representatives who are not also investment advisers or investment adviser representatives A recent study suggests that (..)

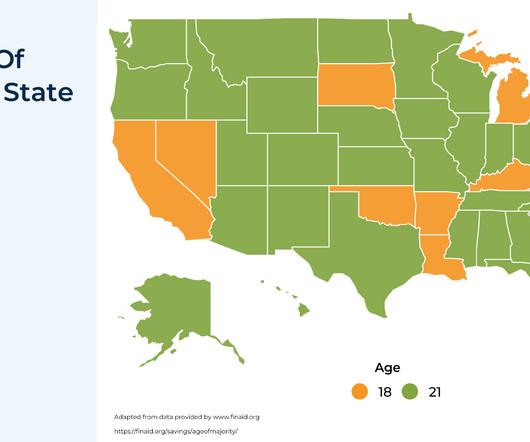

To achieve this, financial support may start at a very young age, allowing for a longer growth horizon and, in many cases, serving tax and estate planning purposes. However, once a child reaches the age of majority, they may not always be in a position to manage assets responsibly.

Related: Planning for Older Clients and Those with Disabilities Many GRATs include a so-called “swap” power in which the grantor is permitted to substitute assets of equivalent value with the GRAT. Prior case law in the Southern District of New York (Morales v. Quintiles Transnational Corp. 2d 369 (S.D. 1998) and Donoghue v.

Would you like to diversify but also defer paying big capital gains taxes? I’m Barry Ritholtz and on today’s edition of at the money we’re going to discuss how to manage concentrated equity positions with an eye towards diversification and managing big capital gains taxes. None of these solutions are optimal.

These alternative investments can offer distinct advantages in the shape of portfolio diversification and the potential for higher returns, but they can come with equally distinct tax complications that need to be carefully planned for. What are the key tax strategies for alternative investments in 2025?

As the year comes to a close, now is the time to review potential financial moves to help minimize your tax burden heading into 2025. Proactive year-end tax planning can lead to significant savings and set you up for financial success in the new year. Find your next tax advisor at Harness today. Starting at $2,500.

Donor-advised funds (DAFs) have emerged as powerful tools that deliver this exact combination, providing immediate tax advantages while offering flexibility to recommend grants to qualified organizations over time. Table of Contents What Are Donor-Advised Funds, and How Do They Work?

We also get you up to speed on the tax benefits of using a DAF. If you've heard of a DAF and are curious about incorporating it into your giving and tax planning strategy, this article is for you. Key Takeaways: Contributions to a donor-advised fund reduce your tax bill in the year your contribution is made.

Without proper planning, taxes can unexpectedly take a large bite out of the proceeds, potentially reducing financial security and the legacy. When you understand various exit strategies and their tax implications early, you position yourself to make informed decisions that maximize after-tax value while ensuring a smooth transition.

April 15 marks the IRS tax return filing deadline for 2025. Although this is the traditional tax filing deadline, given the spate of recent natural disasters (such as the California wildfires and Hurricane Milton), the IRS is granting certain filing and payment extensions beyond this date.

The post Tax Strategies for High-Income Earners 2025 appeared first on Yardley Wealth Management, LLC. Tax Strategies for High-Income Earners in 2025. In this comprehensive guide, we’ll explore proven strategies to help you minimize tax liability while staying compliant with current regulations.

Traditional Investment Strategies The Role of Income Tiers and Priority Levels Case Studies Key Considerations Conclusion Introduction Waterfall Wealth Management is a financial strategy designed for high-net-worth individuals seeking a structured, prioritized approach to wealth distribution.

As dynamic as the secondary market may be, secondaries come with complex tax implications that can significantly impact returns if not properly managed. What are the tax implications of secondary transactions? What are the tax challenges in secondary transactions? What tax strategies optimize secondary investments?

And also, you know, there are really nice tax planning mechanisms that people can use to help them achieve, achieve those things as well. Yeah, get, get some advice on the tax aspect of this. A tax deduction on that contribution. It’s a way to reduce the tax burden associated with, um, that IRA. It’s lumpier.

Also in industry news this week: A recent survey indicates that younger "DIY" investors are more likely to be interested in working with a human advisor than their older counterparts, suggesting an opportunity for advisors to tap into this demographic (perhaps by setting minimum planning fees that ensure these clients can be served profitably today (..)

While a Roth conversion may never make sense for some individuals, for others, early retirement years may be the best time to convert pre-tax accounts to tax-free Roth. Your current and projected future tax rate is often a main component of the decision, but there are other considerations and benefits as well.

While the appeal of real estate may be evident, complex federal, state, and local tax regulations can present a major challenge to the profitability of your property investments. Table of Contents Understanding real estate taxes What are the most tax-efficient ownership structures? Net Investment Income Tax (NIIT): A 3.8%

Using Health Savings Accounts (HSAs) to manage healthcare costs in retirement A health savings account (HSA) is one of the most tax-efficient tools available for covering qualified medical expenses, both before and during retirement. Tax-free growth on interest and investment returns within the account.

The firm manages numerous ETFs, including those that focus on shareholder yield and is approaching 3 billion in client assets. So investors that focus only on dividends historically now miss over half of the picture on how companies distribute their cash. Let’s bring in Meb Faber founder and CIO of Cambria.

Asset management Connecting investors to what matters most, so they can achieve their goals and make confident decisions. These tax-advantaged funds provide capital to small and midsized U.S. To qualify as a BDC, at least 70% of a fund’s assets must be invested in U.S.-based Neither SEI nor its affiliates provide tax advice.

Full transcript below. ~~~ About this week’s guest: Matt Hougan, Chief Investment Officer at Bitwise Asset Management discusses the best ways to responsibly manage crypto assets. His firm runs over $10 billion in client crypto assets. And so our distribution team sits under that. You can see it before your eyes.

Below are some of the mistakes you should avoid making to secure your wealth: Mistake #1: Not diversifying your investments Investing too much of your money into one sector, one type of asset, or one region can expose your wealth to unnecessary risk. A good estate plan ensures your assets go where you want them to. The good news?

If one stock makes up more than 10% of your overall asset allocation, it’s probably too much. When considering the distribution of excess lifetime returns of individual stocks vs the Russell 3000, the median stock underperformance was almost -10%.(J.P. What is a concentrated stock position?

This can come from dividends, interest, rental income, and distributions from brokerage or retirement accounts. A helpful approach is to categorize expenses into: Fixed expenses: Mortgage, rent, property taxes, insurance, and loan repayments. Earn Earnings go beyond just a paycheck. Invest Investing can help savings grow over time.

Positioning Philanthropy as a Cornerstone of Legacy There are many reasons for giving during your lifetime, including supporting causes you care about, making a positive impact on the world, and accessing certain tax advantages. There are overall limits on charitable donation tax deductions, however.

When considering the various business structures available, understanding the tax implications is crucial for making informed decisions. A Limited Partnership (LP) offers a unique blend of operational flexibility and liability protection, but its tax treatment can be complex. Table of Contents What Is a Limited Partnership (LP)?

The post Tax-Free Transfers from Your IRA to Charity: A Smart Financial Strategy appeared first on Yardley Wealth Management, LLC. Tax-Free Transfers from Your IRA to Charity: A Smart Financial Strategy At Yardley Wealth Management, we understand that many clients want to make a difference while also securing their financial future.

Getting Started: What First-Time Planners Should Know Even for seasoned investors, key decisions around taxes, estate structure, and long-term income planning can carry significant implications. She wants to minimize taxes while aligning her legacy with charitable values.

The Tax Cuts and Jobs Act (TCJA)the 2017 tax code overhaul designed to boost economic growthis set to expire on December 31, 2025. Unless Congress intervenes, the TCJAs sunset will usher in a swathe of tax increases in 2026, with analysts estimating that over $4 trillion worth of tax hikes could take effect.

If you have commingled deductible and non-deducted IRA contributions in your outside IRA accounts, having an active 401(k) plan can help you to “separate” the deductible IRA assets from the non-deducted. Depending upon the state you live in, IRA assets may be available to your creditors in the event of a bankruptcy.

For example, “The Complete Tax Optimization Guide for Healthcare Professionals” speaks directly to physicians and dentists who face unique tax challenges. If you work with business owners, highlight how you helped a client reduce their tax burden by 30% while increasing their retirement contributions.

Private equity and alternative investments create unique tax reporting complexities that demand attention. This article explores the distinctions between K-1 and 1099 reporting, explaining their impact on tax planning, basis calculations, filing deadlines, and strategies to optimize your after-tax returns from alternative investments.

Roth IRA conversions present a significant challenge for retirement planners: pay taxes now or later? Moving funds from traditional IRAs to Roth accounts triggers immediate taxation but promises tax-free withdrawals in retirement. The absence of required minimum distributions during the owner’s lifetime.

Understanding how assets will be distributed, navigating tax implications, and aligning these decisions with your personal goals can feel overwhelming. Estate planning is one of the most important steps in securing your financial legacy, but its also among the most complex.

Start saving early by contributing to tax-advantaged accounts like 529 Plans or Coverdell Education Savings Accounts (ESAs). These accounts come with tax benefits that can alleviate future financial pressures when it’s time for your child to attend college.

But if you make $350K a year and you were approved for two mortgages (or bought the houses with cash) then you might feel cash flow poor, but you are very likely asset rich. That leaves them asset rich and/or experience rich and cash poor. Tax deferred plans (IRA and 401K): $1,021,147. And that’s possible here.

An endowment is a portfolio of assets that is invested to provide support for a cause. Donations to endowment funds are tax-deductible, giving them a place in your overall financial management and tax plan. An endowment offers benefits that can extend beyond tax deductions and financial efficiency.

With careful planning, you may be able to reduce your tax bill or optimize the impact of your estate. Youll want to consider your income, net worth, types and liquidity of assets, your future needs and familys needs, and any other plans you want to fund like a business venture or advanced degree.

We've talked about these as sort of being depleting assets. To buy the JP Morgan YieldMax (JPMO), you'd need some basis to believe the common won't crater but the YieldMax as an asset likely to deplete at some rate of speed won't implode on a total return basis if the stock meanders or even struggles.

The first example to look at they call Leverage In The Strategic Asset Allocation via this table in the paper. The distribution of results are pretty even. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. These are easy to model.

Barron's wrote about the difficulty of spending down accumulated assets in retirement. Generically, dividends are not tax efficient. They are taxed at ordinary income. SCHD has historically paid "qualified" dividends which are taxed more favorably as capital gains but this is something to continuously track.

Because many taxpayers earn too much to make pre-tax IRA contributions as they have a 401(k) at work. Although any investor with earned income can make a non-deductible contribution to an IRA (up to $7,000 in 2024-2025 if under age 50) and still take advantage of tax-deferred growth, it still may not be advisable. Yes and no.

Do you know how you will take money from your 401(k) or IRA, how you will take Social Security, how to be tax-smart with your income planning? Your advisor can help you decide which solution provides the most protection for you based on your income and assets. Its also how you plan your retirement income.

Thats because wealth at the upper end tends to be built not just through income, but through equity ownership, business interests, long-term investing, and real estate gains, assets that benefit from compounding, appreciation, and favorable tax treatment over time. Whats on the Average American Balance Sheet?

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content