This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Because when it comes time to rebalance the portfolio to its assetallocation targets – or to reallocate the portfolio to a new strategy – any trades made to implement those changes can generate capital gains, resulting in tax consequences for the investor. Read More.

Also in industry news this week: NASAA has proposed an amendment to its broker-dealer conduct model rule that would restrict the use of the terms “advisor” and “adviser” for broker-dealers and their registered representatives who are not also investment advisers or investment adviser representatives A recent study suggests that (..)

Nonetheless, given the scale and brand awareness of the wirehouses, and as their own use of fee-based models increases (as opposed to primarily relying on commissions from selling products), competition for clients (and advisors) will likely remain stiff going forward, even amidst the favorable trends for RIAs Also in industry news this week: A recent (..)

tonyisola.com) Age is just one factor when it comes to your assetallocation. mrmoneymustache.com) Why you need to account for your Treasury income on your state taxes. (podcasts.apple.com) Investing Targeted apathy as an investment philosophy. ofdollarsanddata.com) Invest time in your life, not in managing your portfolio.

This includes a broad AssetAllocation including full Diversification of asset classes, geographies, etc. AssetAllocation. You must have a Financial Plan , so it is clear what you are investing for, and so you can see how you are progressing towards those goals. Federal Reserve. Corporate Earnings. Volatility.

A reader asks: If Bill Sweet’s favorite topic is Roth IRA’s/401K’s, I’d bet his second favorite is tax gain harvesting (in a taxable account). For 2024, individuals with taxable income below $47,025 ($94,050 for married couples) pay 0% tax for long-term capital gains (LTCG). The idea would be to r.

peterlazaroff.com) Investing There's no magic rule for assetallocation. theconversation.com) Taxes Earned income? flowfp.com) Billionaires pay their taxes differently. (podcasts.apple.com) Peter Lazaroff talks with Manisha Thakor author of “MoneyZen: The Secret to Finding Your “Enough.” Your child can open a Roth IRA.

So historically, every $1 million invested would yield annual dividend income of $19,800 on average… before tax. If you own 10,000 shares, you receive $40,000 in dividend income (before taxes) and have a portfolio currently worth $2M. Over the last 30 years, the S&P 500’s average dividend yield was 1.98%.

Tax-loss harvesting is a powerful strategy that investors can use to reduce their taxable income. As effective as tax-loss harvesting can be, there are a number of important details that investors need to be aware of in order to implement the strategy successfully while following regulations. How does tax-loss harvesting work?

Reevaluate Your AssetAllocation If watching your investment portfolio fluctuate causes anxiety, your current allocation might be too aggressive. You can reduce your stock exposure and increase investments in fixed income options, such as cash or bonds, within tax-advantaged accounts (like a 401(k), IRA, or Roth IRA).

Though in practice, while a 1% AUM fee is a common 'starting point' in the industry, the actual fee structure can vary based on the firm's approach; for example, some firms may reduce the fee for high-net-worth clients, or charge an additional fee for separate and additional services (from deeper financial planning to add-ons like tax preparation).

As the year comes to a close, now is the time to review potential financial moves to help minimize your tax burden heading into 2025. Proactive year-end tax planning can lead to significant savings and set you up for financial success in the new year. Find your next tax advisor at Harness today. Starting at $2,500.

If one stock makes up more than 10% of your overall assetallocation, it’s probably too much. Charitable Contributions: Donating appreciated stock to charity while reducing capital gains tax. This includes the stock itself, its sector, industry, and other highly correlated assets.

However, what is equally critical when it comes to creating a portfolio is assetallocation and selection. Assetallocation aims to balance risk and reward through a portfolio composition of different kinds of assets. If not allocated efficiently, you may become subject to a slew of taxes and other charges.

For those in high-tax states, dividends can be particularly tax-inefficient. The Ancient Wisdom of AssetAllocation Interestingly, Faber draws inspiration from a 2000-year-old investment principle found in the Talmud, which suggests dividing one’s portfolio into thirds: business, land, and reserves.

Because of these differences, stocks and bonds accomplish different things in an assetallocation. Taxes, fees, expenses, trading costs, etc. As economic conditions and income needs change, so too will your assetallocation. When you own a stock, you’re buying a piece of equity ownership in the company.

riabiz.com) Retirement Why retirees should include Social Security into their assetallocation. morningstar.com) Delaying taxes in retirement isn't always the best strategy. thinkadvisor.com) How Notice 2022-53 has affected the tax code. (riabiz.com) CI Financial ($CIXX) is planning to spin-off its U.S.

As the tax year draws to a close, many high-income investors will look to reposition their portfolios to intentionally generate losses as a way to offset gains — an investment strategy known as tax loss harvesting. A net neutral tax position. What Is Tax Loss Harvesting? How Tax Loss Harvesting Works.

Key benefits include: Ensuring essential financial obligations are met first – Taxes, estate planning, and retirement savings take precedence. Strategic long-term planning – Provides a roadmap for surplus wealth allocation. Wealth preservation – Protects assets while allowing for strategic investments and philanthropy.

CIO Perspectives Webinar, 2022 AssetAllocation Outlook mhannan Fri, 03/18/2022 - 06:42 Markets have been unsteady at the start of 2022, driven by geopolitical tensions, inflation, and concerns about equity valuations. Brown Advisory does not render legal or tax advice. The war in Ukraine is causing even more uncertainty.

CIO Perspectives Webinar, 2022 AssetAllocation Outlook. CIO Perspectives Webinar, 2022 AssetAllocation Outlook . The themes and topics discussed include: The performance of various markets and asset classes over recent years and since the onset of the Ukraine conflict. Fri, 03/18/2022 - 06:42. Watch the Video.

🔊 Play Audio Have you heard of the Income Tax Saving Festival in India? Well, usually it starts in the last quarter of the financial year (Jan-Mar) when many employees scurry to provide investment proof to save tax outgo. If not already, why not from today?

A portfolio review can help you: Assess your investment objectives and confirm they align with your financial plan Evaluate your time horizon and risk tolerance Ensure proper diversification and assetallocation Review tax management strategies, including capital gains and the Net Investment Income Tax (NIIT) Monitor performance beyond just returns, (..)

One of the pre-market Bloomberg emails gave a positive mention to the Cambria Global AssetAllocation ETF (GAA) because it is up in what of course has been a tough tape for equities this year. It is an interesting assetallocation that targets 40% in equities, 40% in fixed income and 20% in alternatives.

What to Do Instead: Stick to fundamentals: Learn about assetallocation, risk management, and diversification before investing. But many jump into stocks, crypto, or NFTs without understanding risk, diversification, or assetallocation.

If your employer offers a Roth 401(k) option, evaluate whether splitting your contributions between traditional and Roth accounts might benefit your long-term tax strategy. Tax Efficiency: A Often Overlooked Opportunity One area where I see clients consistently leaving money on the table is tax planning.

Review risk tolerance and current assetallocation strategy It’s important to ensure your clients’ portfolios align with their risk tolerance because taking too much risk can negatively impact their ability to navigate market fluctuations. You can help them start the year right by conducting a retirement checkup.

Advisors are being asked to provide their clients with a full suite of solutions, ranging from estate and tax planning to portfolio management, and everything in between. Clients are increasingly eager to gain access to fully customizable solutions that meet their individual needs.

This is a little bit of a follow up to yesterday where I mentioned the Global AssetAllocation as mentioned in a paper by Meb Faber. Today, Meb Tweeted out a reference to the Atlas Lifted report from Robeco which references a similar idea, the Global Market Portfolio which is allocated as follows.

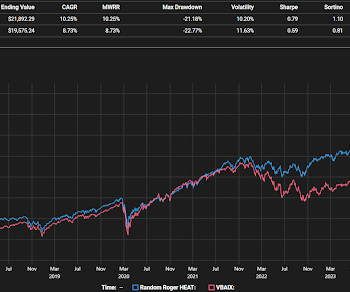

Other than having the proper assetallocation and addressing sequence of return risk when relevant, I would not want to get too aggressive, like selling 95% of my stocks, trying to fight that inertia. What if it jumped 10%, he got back in and then it fell 30% and then traded sideways? The chart is the S&P 500 going back 40 years.

Your assetallocation is the percentage of your portfolio that you distribute between different asset classes, like stocks and bonds. To rebalance your portfolio, you’ll buy and sell certain investments to realign to your accounts with your desired assetallocation. Then work down, perhaps going to U.S.

A financial advisor can help navigate the complexities of wealth management, from tax considerations to estate planning and retirement strategies. Their role extends beyond investment managementthey can help with: Retirement Planning : Structuring your assets to support your desired lifestyle. Ready to Grow Your Wealth?

The more someone trades, the more they are fighting that natural inertia other than proper assetallocation targets and mitigating sequence of return risk when relevant. They are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation.

Consequently, the portfolio allocation should reflect these probabilities depending on the risk profiles. Therefore, we maintain our underweight position to equity (check the Model Portfolio Current assetallocation below). One can consider debt portfolios with floating rate instruments for long-term allocation.

Tariffs are, essentially, taxes imposed on imported goods. Diversifying portfolios across asset classes, sectors, and geographies to reduce concentrated risks. Emphasizing low-fee, tax-efficient strategies to maximize your returns regardless of market conditions. And should we be concerned?

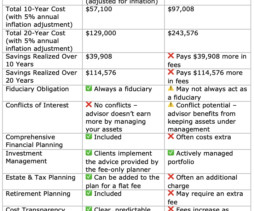

Unlike AUM advisors, they dont have an incentive to keep assets under management, so their recommendations are truly objective. Comprehensive Financial Planning is Included Many AUM advisors charge extra for estate planning, tax strategies, and retirement planning. Are There Any Benefits to AUM-Based Advisors?

The process of diversifying among asset classes is known as assetallocation, and the exact composition should be based on your financial goals and risk profile. You can also further diversify within an asset class. You should be re-evaluating your assetallocation at regular intervals to keep your portfolio on track.

The Roth Man himself, Bill Sweet, joined me on the show this week to discuss questions about taxes in marriage, retirement withdrawal strategies, the tax implications of selling farmland and how to manage tax rates in early retirement.

Rebalancing a 401(k) refers to adjusting the assetallocation of your investment portfolio back to its original target percentages. Your investment strategy determines the target percentages for each asset, often based on your risk tolerance, investment goals, and time horizon. Click to compare vetted advisors now.

Today, we’re excited to announce we’re releasing updated assetallocations for all of our Automated […] The post Wealthfront’s Portfolios Are Now Even More Tax-Optimized appeared first on Wealthfront Blog. As part of that commitment, we are always looking for opportunities to help you earn more and keep more.

Take advantage of tax-advantaged retirement accounts such as 401(k)s, IRAs, and Roth IRAs to maximize your contributions and benefit from tax-deferred or tax-free growth. Rebalancing involves selling appreciated assets and buying underperforming ones to keep your portfolio aligned with your goals.

Of course, one of the most important aspects of retirement planning is managing retirement taxes. Taxes can significantly impact the amount of money you’ll have for retirement. As such, you must be aware of any tax implications arising from your investments during your working years.

Of course, one of the most important aspects of retirement planning is managing retirement taxes. Taxes can significantly impact the amount of money you’ll have for retirement. As such, you must be aware of any tax implications arising from your investments during your working years.

The assetallocation was 10% to hedges, 30% to T-bills for asymmetry but that seems more like optionality to me, 9% to edges which included one broad stock picking ETF, a derivative income fund and a short volatility product. None of them were hideously wrong out of the blocks but it's too soon to declare victory with them.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content