This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

This lack of clarity made retirementplanning significantly more challenging. In response, Congress passed the Social Security Fairness Act at the end of 2024, repealing the WEP and GPO in full. Now that the WEP and GPO have been repealed, retirementplanning will be significantly easier going forward.

Enjoy the current installment of "Weekend Reading For Financial Planners" – this week's edition kicks off with the news that a recent report finds that the number of SEC-registered RIAs, the assets that they manage, and the number of clients they serve all increased between 2023 and 2024 and suggests the industry is robust across the size spectrum, (..)

Enjoy the current installment of "Weekend Reading For Financial Planners" - this week's edition kicks off with the news that according to a recent study by DeVoe & Company, only 42% of RIAs surveyed have written succession plans and either have begun to implement them or have already done so.

That means if your retirementplan underestimates medical costs, you risk serious shortfalls. over that period. If you planned to live on ₹1 lakh per month today, you might need ₹1.5 – ₹1.7 Prior to this, the inflation rate was 3.34% in March 2025 , 5.22% in December 2024, and 5.48% in November 2024.

Which could include measures such as additional time to comply with rules that have been adopted but not yet enforced and perhaps, more broadly, an approach from the SEC that focuses more on whether a firm has robust program controls and a strong fiduciary culture rather than seeking out specific, (sometimes minor) missteps and producing enforcement (..)

As a result, financial advisors should start honing the services Gen X members will likely benefit from the most, including retirementplanning, estate and tax planning and mortgage refinancing. advisors’ clients, up from 20% in 2021, according to a survey Cerulli conducted in 2024. trillion annually.

At the same time, CFP Board has noted that advisors pursue the certification voluntarily and that its standards, which cover the entire financial planning process (unlike SEC and FINRA regulations that largely focus on investment management), help to raise standards for the industry as a whole at a time when advisors increasingly offer comprehensive (..)

True North Expands in SF Deals & Moves: Creative Plannings Snag Hawaii RIA; $5.1B True North Expands in SF Deals & Moves: Creative Plannings Snag Hawaii RIA; $5.1B has acquired a team in Hawaii overseeing $430 million in client assets.

Between 2014 and 2024, Mason transferred client funds into his own accounts and those of the two entities without clients’ authorization, according to the SEC. Mason, who ran Rubicon Wealth Management, a registered investment advisor in Gladwyne, Pa., He pleaded guilty to all of the criminal charges.

The new law repeals both the WEP and GPO, restoring full Social Security benefits to affected individuals, retroactive to January 2024. But the challenge in making such an estimate is the fact that SSA doesn't clearly show many individuals what their full benefits would be without the reduction for WEP or GPO.

in 2024 , with revenue up by 17.6%. Enjoy the current installment of "Weekend Reading For Financial Planners" – this week's edition kicks off with the news that Charles Schwab's annual RIA benchmarking study found that median firm AUM increased 16.6% net organic growth and larger firms seeing 5.0%

Because when it comes to financial planning, you’re ready to write it downand studies show that writing down your goals makes you 42% more likely to achieve them. Heres your top 10 financial planning checklist for the new year. A little planning now avoids big headaches later. Ready to Tackle 2024? Not for you.

Mike McGlothlin , CFP, CLU, ChFC, LUTCF, NSSA, Executive Vice President, Retirement, at Ash Brokerage , is the 2024 recipient of the Kenneth Black Jr. NAIFA and FSP merged in January 2024. Leadership Award. McGlothlin manages a staff of more than 65 employees and has maintained a 90% retention rate.

Garry Esquire, CFP®, MBA Founder & CEO of Yardley Wealth Management Setting meaningful financial goals in 2025 requires more than just wishful thinking – it demands a strategic, well-planned approach. Interest rates remain a significant factor in financial planning, affecting everything from mortgage rates to investment returns.

Stocks vs bonds historical returns by calendar year (1997 – 2024) Top takeaways: Between 1997 and 2024, the S&P 500 returned 9.7% Returns shown are based on calendar year returns from 1950 to 2024. Growth of $100,000 is based on annual average total returns from 1950 to 2024. on an average annualized basis.

Strategy Contribution Limit (2024) Advantages Disadvantages Backdoor Roth IRA $7,000 ($8,000 if 50+) Circumvents income limits for Roth IRA, providing increased tax-free growth Low annual limit and pro-rata rule complications. It also requires an individuals 401(k) plan to allow after-tax contributions and in-service withdrawals.

Do you know when you want to retire? Are you saving enough for the retirement you want? Myth #2: You should plan to retire in your 60s With more people going back to school or changing careers later, holding off on retiring is becoming more common, too. for more information.

Before you can evaluate stocks or bonds to invest in, you’ll need to develop the metrics you plan to use in the analysis. Generally, investors don’t increase their risk profile as they move through retirement. Morgan Guide to the Markets, as of 1/31/2025 Assumes shares purchased 12/31/2004 and analysis ends 12/31/2024.

This article will explore how to navigate complex tax situations arising from multiple income sources, examining various income types, reporting requirements, self-employment obligations, and strategic approaches to record-keeping and tax planning that can help protect your financial interests. rate is comprised of two components: 12.4%

Here’s how it breaks down for 2023-2024: If a couple’s total retirement income is between $32,000 and $44,000, up to 50% of Social Security benefits could be taxable. This is why having a smart, well-rounded retirementplan that includes income planning and tax planning is so important!

These contributions not only provide immediate tax relief but help secure longer-term financial stability during retirement. 401(k) Plans: Contribute the maximum allowable amount for 2024 : $23,000 if youre under 50, or $30,500 if youre 50 or older.

Stocks vs. Bonds: Differences in Risk and Return Make a Case for Both While there wasn’t much that went according to plan in 2020, when we zoom out, this is a picture of a diversified portfolio performing as we might expect. The Callan Periodic Table ranks calendar year returns for various asset classes.

Ericsson reports that video makes up about 60% of all smartphone traffic ; and that number was expected to jump to 74% by the end of 2024. Planning Tips for Your Ideal Audience: Share a quick retirement goal, downsizing tip, or college savings idea for your niche. You dont need to be a pro to get started.

The complex interplay between traditional tax regulations and the innovative nature of tech businesses demands smart planning from day one. Strategic tax planning serves both to keep companies on the right side of IRS regulations and to preserve necessary capital during those precarious early stages when the startup is most vulnerable.

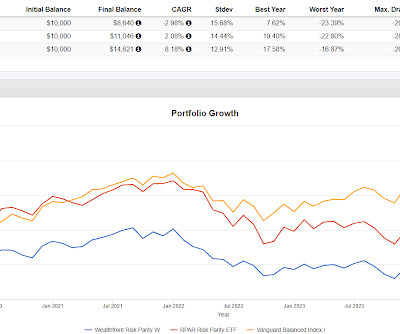

The Wealthfront Risk Parity Fund (WFRPX) is closing to new money as of 12/27/2024 and expects to be liquidated on January 3rd. And looking at the history of the few risk parity funds, it is hard to believe any of them are doing what an investor would hope they would do. billion fund charging 25 basis points.

Updated for 2024 – 2025. Although any investor with earned income can make a non-deductible contribution to an IRA (up to $7,000 in 2024-2025 if under age 50) and still take advantage of tax-deferred growth, it still may not be advisable. Investors often ask: should I be making nondeductible IRA contributions? Why non-deductible?

Eligible IRA owners age 70 ½ and older can make up to $105k in tax-free charitable donations during 2024 through qualified charitable donations (QCDs). A high deductible health plan (HDHP) must have a deductible of at least $1,650 for singles and $3,300 for family. The standard mileage rates for 2024 is $0.67

It is not intended to be a surrogate for a 60/40 portfolio, although it was close in 2024, and it clearly will not and is not intended to look like the US equity market. The idea there is I don't think it can go up another 22,000% from here and I don't think it can fall 80% unless, I say unless an 80% decline is on the way to a 99.9%

In 2024, more Americans than ever are celebrating their 65 th birthdays. 1 As they reach the traditional retirement age, many are looking at their financial future with some degree of trepidation and doubt. For many soon-to-be retirees, the primary concern is not having a source of steady income that will last throughout retirement.

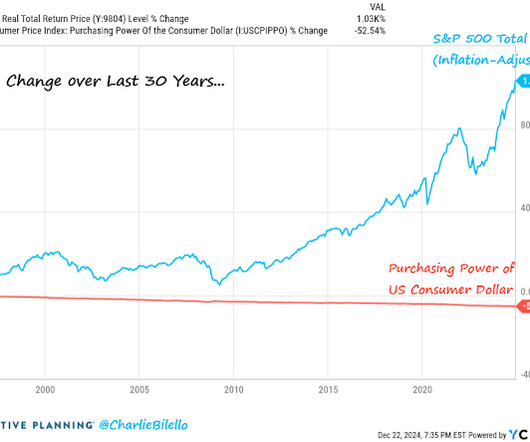

The real return is sort of consistent but was heavily skewed to 2024. A popular rule of thumb is that a real return of 2%, so inflation plus 2%, is considered attractive. Note that 2021 was a partial year.

Each week in Weekend Reading For Financial Planners, we seek to bring you synopses and commentaries on 12 articles covering news for financial advisors including topics covering technical planning, practice management, advisor marketing, career development, and more.

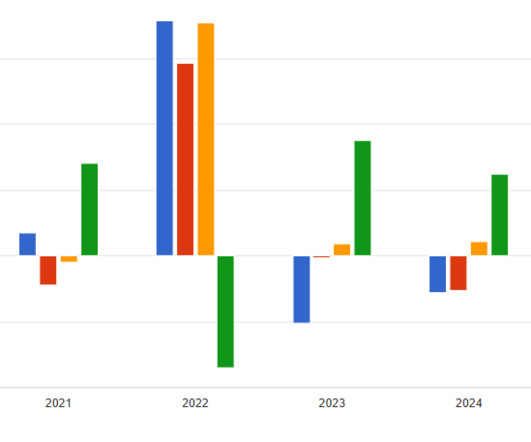

Portfolio 1 was way ahead in 2022, way behind in 2023 and 2024 but it was up nicely those years and this year it is way ahead. In the partial year of 2020, Portfolio 1 was down 83 basis points while the S&P was up 18%. In 2021 it lagged the index by 12%. It has throw in the towel at the wrong time written all over it.

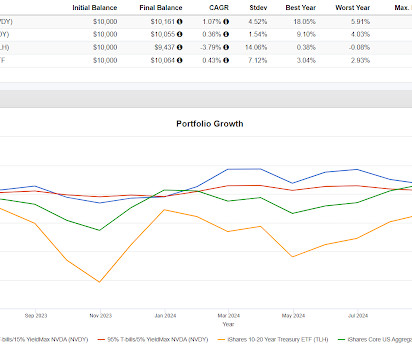

Zweig isolated a couple in particular including the YieldMax Moderna Option Income Strategy ETF (MRNY) noting that MRNY fell "80% from May 2024 to May 2025." A lot of people own them based on the AUM in the space. I'm not sure the catastrophe here was using MRNY.

The outperformance isn't solely because of 2022, VOO/BALT outperformed in partial year, 2021, 2023 and 2024. Using BALT instead of AGG has given a higher compounded return with less volatility. This year it is trailing a little bit.

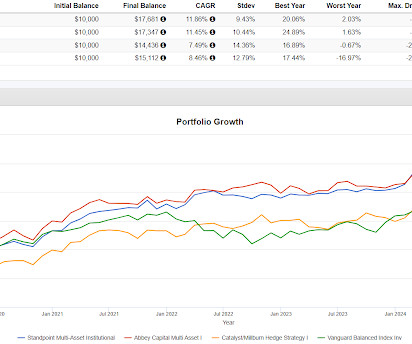

Certainly 2023 was tough for these funds but while managed futures didn't do very well in 2024, the funds generally kept up with VBAIX. And the year by year MBXIX is curious. It had a couple of terrible years this decade but was the best performer in 2022.

An IRA is one of the most powerful retirement savings tools available, and the most common options are a traditional IRA and a Roth IRA. That depends on your overall financial plan and a variety of other factors. For example, you could make IRA contributions that applied to the 2024 contribution limit until April 15 of 2025.

One of the pre-market emails that Bloomberg sends out included a passage on Monday morning noting that 96% of all ETFs are up in 2024 which is a very high percentage. Many ETFs are up a lot of course but " popular gauges tracking hedge-fund returns are scoring much smaller victories."

Several personal factors should influence the timing of your claim, including your health, marital status, financial needs, and your plans for continued work. 3 RMDs apply to accounts such as traditional IRAs, SEP IRAs, SIMPLE IRAs, and retirementplans like 401(k)s. SmartAsset.com, October 14, 2024 [link] 3.

According to the Bloomberg article , only 62% of the 1080 "newly launched quant-powered investing styles" showed a positive return going into the end of 2024. Bloomberg and Barron's each had similar articles about straying off the beaten path toward ETFs that are not the plainest of vanilla. That's pretty vague.

AMZY had a 50% "yield" in 2024 while dropping about 11% on a price basis (the return for the underlying was very good but AMZY couldn't keep up with the dividend). If it goes as plans, it would be a more tax efficient way to access the index. allocation to the YieldMax Amazon ETF (AMZY)?

Who knows how this will play out, will it be no big deal at all, like the Great Dip Of August, 2024 or something more serious but whatever it will be, it will end at some point and then markets will start to work higher.

The end of the year is an ideal time to start planning for the year ahead and make sure youre on target to achieve those goals. Good financial planning is all about asset and liability matching across time. A financial plan with an asset liability mismatch is likely to fail over time. Asset and Liability Matching.

With a cash buffer of two years or whatever, that sort of decline doesn't have to derail anyone's retirementplan. In five of the backtested years, the change was less than 1% in either direction but in 2023 and 2024 the net change was in the three's. That person would be in some trouble without a cash buffer.

Most professionals approaching retirement know they need a plan. What many underestimate (often drastically) is the size of the piece of that plan that should be devoted to healthcare. Retirement is no longer just about 401(k)s and Social Security. This article is a deep dive into healthcare costs in retirement.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content