This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

For most advisory firms, 2022 has been a year of relative stability, market volatility notwithstanding. Which means now it’s time once again to take at least a brief pause to get some feedback about how we’re doing.

2022 was a year that began with high hopes as households were slowly re-emerging from pandemic shutdowns, markets were reaching new highs, and most advisory firms had growing momentum. A gap our Kitces Courses aim to fill!

Whether you’re preparing to file , waiting on a refund , or have already paid your tax bill, you might notice some differences this year. First of all, many taxpayers are noticing smaller refunds or higher tax bills this year than in the previous two years. In 2022, if your AGI was over $43,000, you could take 20% of the credit.

Our newest course on Life Insurance Policies adds to our existing programs on reviewing Tax Returns and navigating Estate Documents as well, and we're committed to continue to expand our financial advicer curriculum in the years to come!

2022 marks the 50 th anniversary of the enrollment of students into the first Certified Financial Planner (CFP) course, and in the years since then, financial planning (and the process of creating a financial plan) has changed extensively.

By Mike Valenti, CPA, CFP ® , Director of Tax Planning It’s that time of year again! W-2s, 1099s and mortgage statements have been to hit your mailbox: a daily reminder that it is, once again, Tax Season. Overall, it was a relatively quiet year on the tax front. Although Congress isn’t done yet! More on that later.)

A recent announcement regarding cryptocurrency from the CFP Board provided advice on crypto-related investments stating CFPs® are neither required nor prohibited from providing advice related to cryptocurrency, but “should do so with caution.” The CFP Board stated the risks as follows in its communication.

Podcasts Christine Benz and Jeff Ptak talk taxes with Jeffrey Levine, chief planning officer for Buckingham Strategic Wealth. thereformedbroker.com) FutureProof 2022 was a resounding success. kitces.com) CFP candidates are becoming more diverse. Sign up for the next go-round.

If you were surprised at tax time this year, then you’re not alone. 2022tax refunds were about 10 percent smaller than they were last year, and for those who owed money, they tended to owe more than they expected. Taking the time now to make some strategic moves can lead to some significant savings on your taxes for the year.

Best for: All financial professionals, though most of the pro bono counseling opportunities are for CFP® professionals. E&O insurance: Yes, for CFP® pros in good standing who have completed training. Best for: Professionals with CFP®, CPA, ChFC®, CLU®, EA, CSLP®, or CDFA® credentials who want to help women.

If you’ve already filed your taxes and received your refund, you might already be thinking of ways to use that refund. Here are some tips for putting that money to the best possible use in 2022: Avoid impulse tax refund spending. If you received a tax refund, then you might already be imagining different ways to spend it.

Donating appreciated stock to charity can be a great way to give back and reduce your tax bill. Taxpayers who itemize get a tax deduction for the market value of the stock. If you want to make a gift for the 2022tax year – act now. These two steps don’t need to happen in the same tax year.

In 2022, the average American paid between about $100,000 – $200,000 for a four-year college education. This type of account allows your savings to grow tax-free and when you use the money to pay for college costs, withdrawals are tax-free too. Some states offer a tax deduction for contributions.

John Eing, MBA, CPA, CFP® “Understanding cultural values can make you a better financial planner. James Lee, CFP® “Financial planning services are wanted and needed, and I feel that my service to FPA is my way of scaling financial planning to more people throughout society.” Here are eight of their stories to enjoy.

2022 Fall and Winter Travel Prep. 2022 Holiday Spending and Inflation. Bonus: Gifts to charity are tax deductible.) . At Your Richest Life, Katie Brewer, CFP®, believes you too should have access to financial resources and fee-only financial planning. But this year, things are a little different. A looming recession?

And while ABLE accounts can be a bit more complex for Wisconsin residents, they offer significant tax benefits for individuals with disabilities and their families. The money in the account grows tax-deferred and income from the account is tax-free when used for qualified expenses. candidate for cfp® certification.

Transaction fees, management fees, and capital gains taxes can eat into your returns. For example, research from S&P Global found that over the 20-year period ending in 2022, only about 4.1% The markets are fickle, and prone to quick swings based on even seemingly minor events. of professionally managed portfolios in the U.S.

Considering Roth conversions in retirement When you convert pre-tax money from an IRA to an after-tax Roth IRA, the amount converted is included in your taxable income. But in retirement, without a paycheck, it can be a great opportunity to control your tax situation for the year and fill up the lower tax brackets.

2020 or 2021 income applies, but 2022 income does not. Your loans must have been disbursed as of June 30, 2022. Do I have to pay taxes on the canceled debt? You do not have to pay federal taxes on the canceled debt. You do not have to pay federal taxes on the canceled debt.

For example, what’s the best time of year to take required minimum distributions, how to reinvest it, or if you can avoid paying tax on RMDs. All else equal, (though it rarely is), it’s often best to stay invested as long as possible to prolong tax-deferred growth. How to take RMDs and avoid any taxes (legally of course).

I have been sharing my pronouns professionally for some time now on social media, during video meetings, and in discussions,” Laura LaTourette, CFP®, said in an editorial for Financial Planning magazine. For advisor and LGBTQ+ ally Woody Derricks, CFP®, ADPA®, this is a commonsense approach. “It’s

Acts, what that means to you and your Tax Planning in Retirement. Hosted by: Cynthia Flannigan , CFP®. CPA/PFS, CFP, EA, USTCP, AEP. also known as Securing a Strong Retirement Act of 2022 (HR2954), builds on the SECURE Act and its significant changes to retirement. The latest on the RISE & SHINE/SECURE 2.0

Tax time is here again, and if you’re not one of the 25 million Americans who have already filed , then you’re probably going through the process of gathering what you need and preparing to file. The Child Tax Credit and Potential Changes The 2023 child tax credit is capped at a refundable amount of $1,600 – for now.

Act, signed into law December 29, 2022, is designed to help strengthen the retirement system and Americans’ preparedness for retirement. We’ll be taking an in-depth look at recent tax law updates for 2023, focusing on SECURE 2.0 Register now for the 2023 Tax Legislation Insights, Secure 2.0 The SECURE 2.0

Congress is once again poised to make sweeping changes to the retirement and tax rules in the last two weeks of the year. There are many components of the 2022 Act that will impact employers that aren’t outlined below. IRAs: the $1,000 catch-up limit will be indexed by inflation for tax years starting in 2024.

1 year total return 11/2021 – 10/2022. These charts also highlight the downside of tax loss harvesting. Harvesting losses only for tax purposes can have broader implications due to the wash sale rules. Article written by Darrow Advisor Kristin McKenna, CFP® and originally appeared on Forbes. Silver lining!

In a 2022 advisor technology study, 56 percent said they chose each tool on an individual basis, with an average of five tech vendors per practice. In a 2022 advisor technology study, 56 percent said they chose each tool on an individual basis, with an average of five tech vendors per practice. Sources: 1. The Cerulli Report.

Health insurance is often the focus of open enrollment, but don’t forget about the other important benefits offered, like: Health Savings Account (HSA) – HSAs are savings accounts funded with pre-tax contributions. They also have tax-free earnings and tax-free withdrawals for qualified medical expenses.

Although 2023 closed with a festive explosion, 2022 ended with a bearish growl. Effectively, 2023 was a reverse mirror image of 2022. In 2022, the stock market fell -19% (S&P) due to a spike in inflation. For the year just ended, much of the year felt like a party, but 2022 felt more like a funeral.

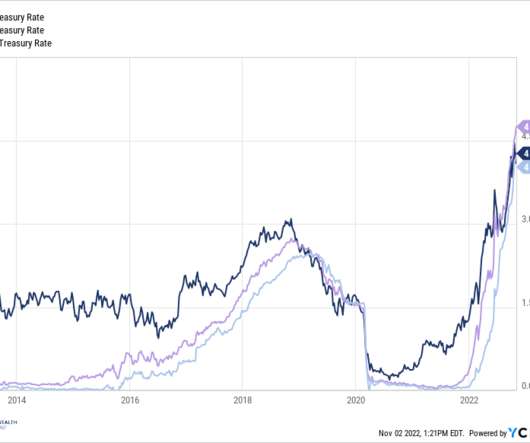

As of 9/30/2022, the 1-year Treasury was yielding 4.05% versus 4.22% on the 2-year Treasury. As an added bonus, Treasuries are exempt from state tax. Core inflation was 6.32% year-over-year as of September 30th, 2022. Article written by Darrow Advisor Kristin McKenna, CFP® and originally appeared on Forbes. Treasuries.

This is an increase from the $20,500 you could contribute in 2022. This is an increase from the $6,500 catch-up contribution for 2022. This is an increase from the 2022 limit of $61,000 ($67,500 including catch-up contributions). You also may be able to make after-tax contributions into your 401k as well to get up to the limit.

To implement these strategies successfully, we must first understand the difference between claiming the standard tax deduction and itemizing deductions. In this blog post, we will explore three charitable giving strategies intended for a tax deduction, minimizing record keeping, and increasing donations to charity.

It’s hard to believe for many, but after a strong performance in October and November, stock market losses during 2022 have registered in at a mere -4.8%, as measured by the Dow Jones Industrial Average. The latest growth forecast for the fourth quarter of 2022 is expected to accelerate to +4.3%, which was also revised higher , recently.

Here are 36 financial advisor influencers who will likely have a big impact on the industry in 2022. Steve Sanduski Steve Sanduski is a CFP® professional and personal coach to financial professionals. Jim Blankenship Jim Blankenship is a CFP® professional who specializes in Social Security, income tax, and personal finance.

Implementing these strategies can help reduce tax bills, save more, and achieve financial goals sooner. The deadline for tax filing is around the corner. Besides meeting all the requirements for this date, have you considered the impact of implementing long-term tax strategies on your wealth?

CFP ® , Director of Consumer Investment Research. LLM, CFP ® , ChFC ® , CLU ® , RICP ® ,? An individual who learns to manage $4,000 a month after taxes will be equipped to manage $14,000 or even $40,000 a month as their earnings increase over time. Craig Lemoine, Ph.D., and Jamie Hopkins,?Esq., Careers, work and responsibility.

Ryan Yamada, CFP ® , Senior Wealth Planner. But wait … it’s 2022. This blog is for general information only and is not intended to provide specific legal, tax, or other professional advice. For a comprehensive review of your personal situation, always consult with a tax or legal advisor. In most years. The market is down.

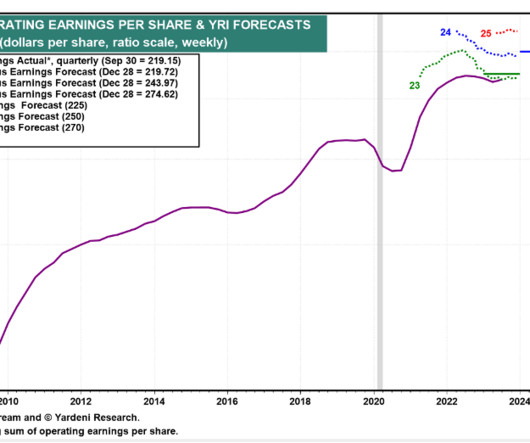

Source: Ed Yardeni (Yardeni Takes) Santa did not show up for a rally last December in 2022. for the Christmas month last year and finished 2022 down -19%. Slome, CFA, CFP® Plan. The S&P 500 index fell -5.9% www.Sidoxia.com Wade W. Subscribe Here to view all monthly articles.

At the 2022 Financial Planning Association National Conference, I and fellow researchers Dr. Sonya Lutter and Dr. Megan McCoy presented research-based evidence that people who have experienced financial stress and hardship in the past are often more resilient in the face of future financial shocks. link] 3 Lazarus, Richard S.,

Maybe ChatGPT will do my taxes next year? 2023 Stock Performance Explained – Index Up but Most Stocks Down Although 2022 was a rough year for the stock market (i.e., S&P 500 down -19%), stock prices have rebounded by +20% from the October 2022 lows, and +9% this year. Slome, CFA, CFP® Plan. Microsoft Corp.,

Scott Budd, CFP ®. Because the coverage is free for people who paid taxes during their working careers. The average monthly premium in 2022 is $170.10. July 29, 2022, [link]. Senior Wealth Planner . Choosing the right Medicare plan is one of the most important decisions seniors are faced with.

In fact, the Federal Reserve has raised the upper limit federal funds rate by 5% since the beginning of 2022. Since the beginning of 2022, cash has outperformed the S&P 500 by about 14% on a cumulative total return basis. Article written by Darrow Wealth Management President Kristin McKenna, CFP® and originally appeared on Forbes.

The CFP Board advocates for a seven-step, cyclical financial planning process which means you’ll continue to revisit the plan to ensure it stays focused and up to date on the changes a client experiences throughout their lifetime. It is not meant to be, and should not be taken as financial, legal, tax or other professional advice.

was signed into law December 29th, 2022, bringing more major changes to tax law. Amount rolled over is tax-free (not included in beneficiary’s income) and penalty-free. Currently, pre-tax or Roth contributions are allowed. Before the passing of the Act, employer funding could only be pre-tax. The Secure Act 2.0

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content